(Tuesday Market Open) Stock index futures attempted a recovery after Monday’s fierce selling as investors await a potentially higher-than-projected rate hike tomorrow from the Federal Reserve. Wholesale price data released ahead of the open was in line with estimates but still indicate that inflation and recession fears are weighing heavily on the U.S. economy.

Potential Market Movers

A day before the Federal Reserve’s June rate announcement, the May Producer Price Index (PPI) came in around expectations at 10.8% year-over-year and up 0.8% for the month, doubling April’s pace. Without food, energy and trade, core PPI rose 0.5% for the month, slightly below estimates but still up 0.4% from April.

It’s the last major piece of government data Fed officials will receive on their way into Federal Open Market Committee (FOMC) discussions today and tomorrow. According to the CME FedWatch tool, there’s now a 91% probability of at least a 75-basis-point rate hike announcement tomorrow afternoon, up from recent Fed projections of serial monthly 50-basis-point hikes going into the fall.

Near the open, U.S. stock futures were making fractional gains. S&P 500 futures remained in bear territory around the 3,770 level with an early gain of +0.45% after the index’s nearly 4% drop on Monday. Dow Jones Industrial Average futures were up +0.34% and Nasdaq futures moved +0.74% higher. The 10-year Treasury yield (TNX) moved slightly lower to 3.345% before the open while the 2-year Treasury yield rose slightly to 3.324%. Both yields had inverted briefly before Monday’s open.

After releasing earnings last night, shares of Oracle ORCL rose 12% premarket after reporting a major increase in demand for its infrastructure cloud business. It will be worth watching to see if other technology stocks are buoyed by the news in today’s trading. Inflation continues as a global concern as European stocks turned lower for the sixth day. Germany’s inflation rate reached the highest level since reunification at 7.9% in May, pointing to the continuing Russia-Ukraine war and rising food and energy prices.

European markets were lower before the U.S. market open, with the DAX down -0.03%, CAC down 0.4%, and the FTSE off -0.11%.

Reviewing The Market Minutes

After digesting Friday’s dismal inflation report and considering more economic headwinds ahead, investors sold out of all major indexes and sectors by the close, leaving the S&P 500 (SPX) down nearly 4% and officially in bear territory.

From tech to cryptocurrency, investors leapt to safety ahead of tomorrow’s Producer Price Index (PPI) report, Wednesday’s Federal Reserve rate announcement, and Friday’s triple witching hour. The S&P 500 fell 3.87% to finish at 3,748.81, the Nasdaq Composite ($COMP) lost 4.68%, and the Dow Jones Industrial Average ($DJI) slid 876 points for a loss of 2.79% on the day.

Good news was tough to find. To start the week, gasoline prices finally hit an all-time nationwide average high of $5 per gallon while 30-year mortgage rates approached 6%, nearly double year-ago levels. On Friday, the government reported higher-than-expected Consumer Price Index (CPI) data that revealed inflation had jumped a full percent since the end of April, speeding past analysts’ 0.7% forecasted increase and dwarfing April’s 0.3% gain.

To indicate how little investors were willing to risk in this environment, the price of bitcoin plunged below $23,000 on Monday, trading nearly 70% below its November highs at one point in the session.

Yields captured the market’s attention as the 10-year Treasury yield (TNX) briefly inverted with the 2-year Treasury before Monday’s open. Seen by many as a recession indicator, it was the second inversion since April. The 10-year rose to 3.387%, while the 2-year finished at 3.383% after the close.

Wednesday’s Federal Open Market Committee rate announcement—and Chairman Jerome Powell’s comments immediately afterward—will likely define this week’s economic news, but they’ll be far from the only events investors will want to watch. Overnight, industrial production and retail sales figures were expected from China, and Germany will be offering its own inflation forecast as a barometer of the European Union’s economic health.

While analysts are speculating that the Fed may increase its expected rate hikes above the 50-basis-point level in the coming months, it’s unclear whether the central bank plans to become more hawkish beyond its previous public statements.

After the close, Oracle (ORCL) rose nearly 9% in extended trading after a better-than-expected earnings report.

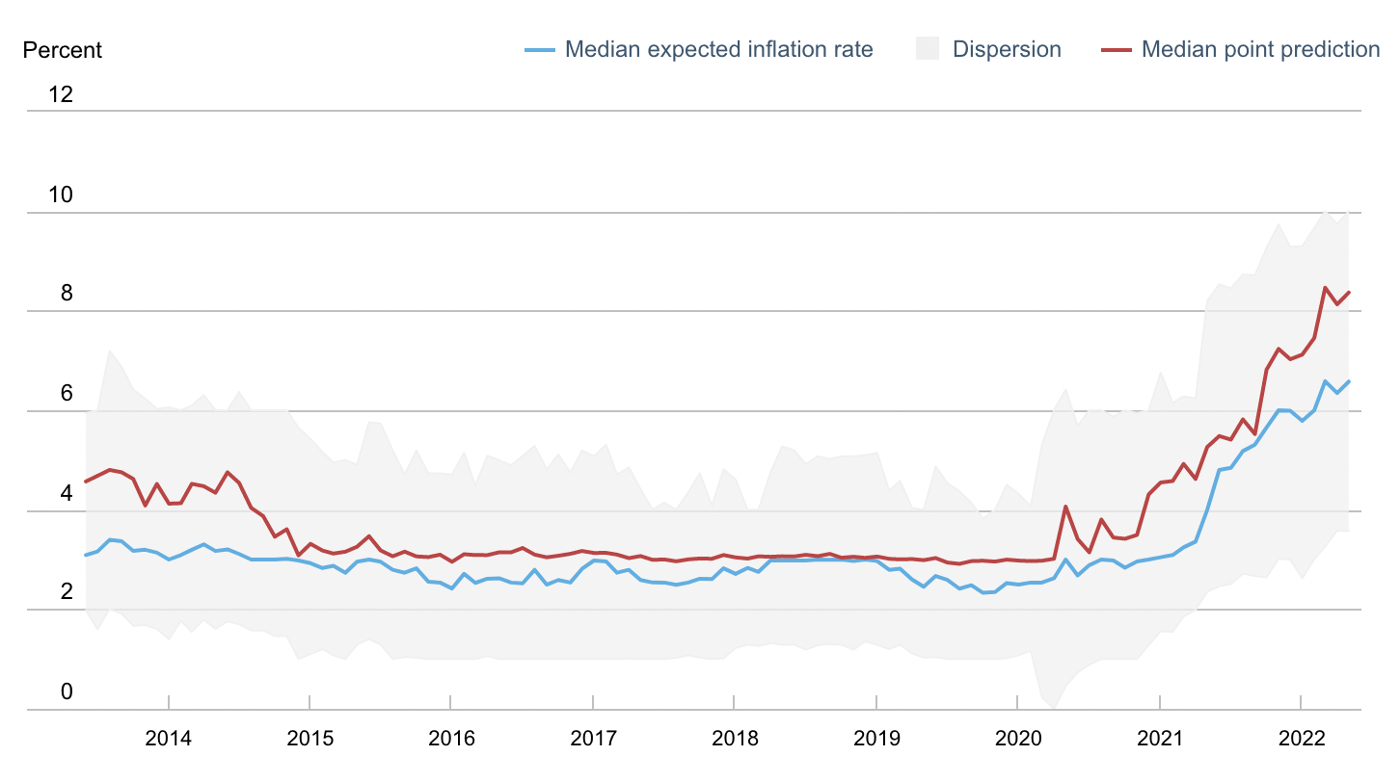

CHART OF THE DAY: NOT-SO-GREAT EXPECTATIONS. Consumer expectations for inflation and spending in the coming year hit record levels in May, reflecting prices that galloped at their highest level in 40 years. New York Federal Reserve data showed consumers expect prices to increase 6.6% (blue), up 0.3% in April and tied with March for the highest rate on record back in June 2013. Chart source: New York Fed Survey of Consumer Expectations.

Three Things to Watch

Job Security: Respondents told a New York Fed survey they expect U.S. unemployment rate will be higher one year from now. That number rose from 36.3% in April to 38.6% percent in May, the highest rate since February 2021. Some 11.1% of respondents said they feared losing their job, up slightly (0.03%) from April but still below the report’s 2021 average of 12.5%.

‘Great Resignation’ Still Alive? For now, some employees seem to think they’ve still got options. Some 20.3% of those surveyed in May said they were voluntarily planning to leave their jobs 12 months from now, compared to 19% who gave the same response in April. That’s the highest reading since September 2020.

Notable Calendar Items

June 15: Retail sales, FOMC interest rate decision

June 16: Building permits, Housing starts, Philadelphia Fed Manufacturing Index, and earnings from Adobe (ADBE), Kroger (KR)

June 20: Markets closed for Juneteenth

June 21: Existing home sales

June 22: Earnings from KB Home (KBH) and H.B. Fuller (FUL)

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Pixabay

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.