(Tuesday Market Open) China said today it’s cutting its pandemic quarantine time for foreign travelers in half and U.S. trade deficit figures fell for the second month in a row, giving a potential boost to already-negative GDP forecasts for the second quarter. Both set the stage for a healthier market open for a busy news week to come.

Potential Market Movers

Equity futures were up this morning after China’s announcement that it will cut institutional and home quarantine time in half for foreign visitors. Meanwhile, the U.S. trade deficit fell 2.2% in May to $104.3 billion, a second straight drop that could lift second-quarter gross domestic product (GDP) and possibly brighten some of the recession talk that’s out there.

Equity futures were modestly higher before the open. S&P 500 futures were up 0.40% after completing their best trading session since 2020 on Friday. Dow Jones futures were up 0.52%, and Nasdaq futures rose 0.31% before the bell. Investors traded through a choppy Monday session following a bear bounce Friday that gave the S&P 500 their best close since 2020.

Wall Street is still set to wrap up the worst first half year for stocks in decades.

China’s national health organization said early Tuesday it would loosen its strict quarantine requirements for international travelers. The nation is refocusing its zero-COVID policies to rebuild its economy.

At home, the better trade deficit report was followed by April results from the S&P CoreLogic Case-Shiller National Home Price Index showing that major metropolitan area home prices rose 20.4% in April, though down for the first time in months compared with an increase 20.6% in March. It looks like a continued squeeze for prospective homeowners as mortgage rates are at a 13-year high.

Conference Board consumer confidence data will be out later in the day.

Premarket, energy and travel stocks were on the rise. Las Vegas Sands LVS was up 8.02% before the bell as was Occidental Petroleum (OXY), up 4.14.%

Reviewing the Market Minutes

Yesterday’s investors took a breather from Friday’s news-making rally to wait out what could be a pivotal week for economic data and the Federal Reserve’s future direction on rates. May durable goods orders and pending home sales, both up an identical, above-expectations 0.07% for the month, couldn’t keep enthusiastic buyers in the game.

Today’s data includes the Conference Board’s June Consumer Confidence Index and the Case-Schiller U.S. Home Price Index results. Tomorrow, Federal Reserve Chairman Jerome Powell is expected to participate in a panel discussion at the European Central Bank (ECB) annual conference in Portugal.

On Thursday comes the May PCE inflation report—known to be the Fed’s favorite inflation barometer—followed by Friday’s much-awaited announcement of the ISM manufacturing index for June, a key indicator of where corporate purchasing manufacturers think the economy is headed.

With all this news ahead, the S&P 500 (SPX) finished down 0.30% during Monday’s session, followed by the Dow Jones Industrial Average ($DJI), off 0.20%, and the Nasdaq Composite ($COMP), down 0.72% by the close. However, the Cboe Market Volatility Index (VIX) finished at just under 27, a full point lower on the day.

After an early run, investors couldn’t sustain last Friday’s rally, which saw the biggest one-day percentage gain in the S&P 500 since 2020. That came after another key consumer barometer, the University of Michigan’s consumer sentiment survey, revised its June measurement of consumer inflation expectations downward to 3.1% from the previous 3.3%. The move was a significant indication that consumers could be a little less worried about longer-term inflation than previously thought.

This week’s data will help set the stage for the start of Q2 earnings reports in July, closing the worst first half for the S&P 500 since 1970. Another potential scene setter: Monday’s bank dividend announcements following last week’s news that the nation’s 34 largest banks passed the Fed’s annual stress test. After the close, JPMorgan Chase JPM said it kept its dividend unchanged, while Bank of America BAC raised its payout 5% and Morgan Stanley MS increased its dividend 11%.

In other market action, energy stocks led all sectors in yesterday’s trading as oil jumped despite the G7 nations’ pledge to cap the price of Russian oil as part of the West’s efforts to support the Ukrainian government. China and India are among the nations expected to stay steady customers for Russian oil. WTI crude oil finished the day at $109.81 per barrel, up 2.19%. Top energy gainers included Valero Energy VLO, up 8%, Devon Energy DVN, up 7.48%, and Hess Corp. HES, up 5.18% by the close.

Other stocks making news during and after Monday’s session:

- Nike NKE beat sales and earnings expectations in its latest quarter but didn’t share a forecast for the year ahead in its announcement after the close. The company’s shares fell 2.13% in Monday’s trading.

- Robinhood HOOD gained 14% in Monday’s trading after Bloomberg News reported cryptocurrency exchange FTX was considering purchasing the trading platform. Last week, FTX offered to provide bailout funds to fintechs BlockFi and Voyager Digital. Yesterday, Voyager Digital announced it defaulted on a $670 million loan to Three Arrows Capital.

- Spirit Airlines SAVE slid 8.12% by Monday’s close after Frontier Group Holdings ULCC raised its bid for Spirit in its acquisition battle with JetBlue JBLU. Frontier stock fell 11.2%, while JetBlue advanced 1.62%.As mentioned above, JetBlue raised its offer again early Tuesday.

- Walgreens Boots Alliance (WBA) gained 1.30% after news reports surfaced Monday that Reliance Industries is in talks to raise $8 billion for a planned leveraged buyout of the global drug store chain. Walgreens will report earnings on Thursday.

On Thursday, the last trading day of the month, U.S. equities may get a boost from end-of-quarter rebalancing. J.P. Morgan’s chief global markets strategist Marko Kolanovic said last Friday that U.S. equities could see a 7% move upward by the end of this week.

It may not be enough to get the S&P 500 out of bear territory—but it could help.

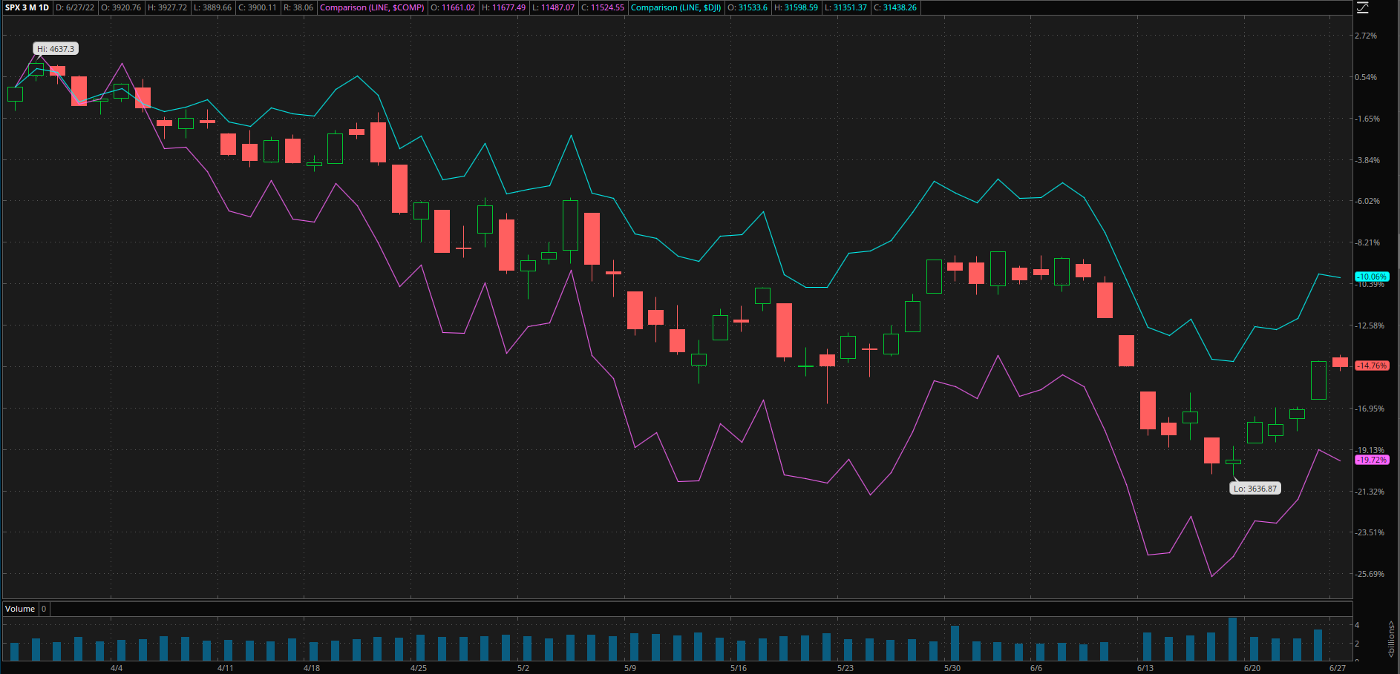

CHART OF THE DAY: LOCKSTEP. In Monday’s trading, the S&P 500 (SPX—candlesticks), Nasdaq Composite ($COMP—pink), and Dow Jones Industrial Average ($DJI) trailed downward by the close. With a heavy economic news week still ahead, this formation will be worth watching. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

10-Year Close-Up: Certainly, there’s more to watch this week than a flood of economic reports. The 10-year Treasury yield (TNX) closed unchanged Monday at a yield of 3.202%. That has some wondering whether bonds will do their part to get equities moving again. Yesterday, Barron’s said a drop below the 3% yield level could drive the stock market higher, or at least keep it from heading lower.

Bankers Home and Abroad: There’s a good chance Fed Chair Powell won’t be the only central bank official making news abroad this week. During today’s session at the European Central Bank (ECB) forum, ECB President Christine Lagarde downplayed global recession risks and pledged to “move faster” on rates if needed to fight inflation. Besides Powell, Bank of England (BoE) Governor Andrew Bailey and Cleveland Fed President Loretta Mester are also expected to speak at the conference. Back in the states, San Francisco Fed President Mary Daly and St. Louis Fed President James Bullard are expected to make appearances this week.

Real Supply Chain Relief? Shifting COVID-19 shutdowns and quarantines in China continue to affect businesses around the world. That’s why today’s new from the health commission about loosening quarantine restrictions impacted global markets. Inside China, the nation’s rebar futures rose in response, indicating signs of returning construction activity. There are other signs of recovery too—the nation released better industrial profits report this week and reports have surfaced that the government might renew its stimulus package to stabilize the country’s economy.

Notable Calendar Items

June 29: Gross domestic product (GDP) and earnings from Paychex PAYX, General Mills GIS

June 30: Initial Jobless Claims, PCE inflation, Chicago PMI, and earnings from Walgreens Boots WBA, Micron MU, and Constellation Brands STZ

July 1: ISM Manufacturing PMI

July 4: Markets closed for Independence Day

July 5: Factory Orders

July 6: JOLTS job openings report, ISM services index and S&P U.S. services PMI

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.