(Tuesday Market Open) A big slide in the U.S. dollar appears to be pushing stocks higher Tuesday as a slew of earnings arrived before the opening bell.

Potential Market Movers

The U.S. Dollar Index ($DXY) was down 0.75% before the market opened, continuing its three-day slide. As of early Tuesday, the dollar index was off about 2% from its recent high. The dollar may trade lower as the eurozone reported year-over-year inflation growth of 8.6%. The print came in on target with analysts’ forecasts. The European Central Bank (ECB) is expected to address rising inflation numbers by increasing its key interest rate 25 basis points at their meeting on Thursday. It would be the ECB’s first rate hike in more than a decade.

Europe has seen slight economic improvement as they’ve adjusted Q1 gross domestic product (GDP) up from 0.3% to 0.6%. Strength in the economy could provide the ECB more room to address inflation with continued rate hikes, which in turn could strengthen the euro against the U.S. dollar.

Equity index futures are higher as the dollar is lower, but we saw a similar setup before yesterday’s open only to see stocks sell off later in the afternoon. However, there was a red flag ahead of yesterday’s open as the Cboe Market Volatility Index (VIX) was higher. This morning, the VIX was below 25 in premarket action, which suggests investors are feeling a little more confident.

After a few days dominated by earnings reports from financials and banks, a more diverse group has reported earnings this morning. But concerns over the stronger dollar continues to be a theme.

- Johnson & Johnson JNJ reported better-than-expected earnings and revenue but trimmed its fiscal-year earnings due to currency headwinds. JNJ was up 0.6% in premarket trading.

- Lockheed Martin LMT reported worse-than-expected earnings and revenue prompting a 3.8% drop in ahead of the opening bell. The defense contractor lowered its forward earnings guidance due to low sales and production slowdowns.

- Haliburton HAL shot up about 3% in premarket action after reporting it beat on top- and bottom-line numbers.

- Hasbro (HAS) was able to beat on earnings estimates despite missing on revenues. After falling 1.2% in premarket trading, HAS cut the losses and was up 0.73% before the opening bell.

After Monday’s market close, IBM IBM reported better-than-expected earnings and revenues but fell 4.26% in extended hours trading. The technology giant said that currency headwinds reduced revenues by $900 million for Q2, $200 million more than the company had anticipated.

After today’s close, Netflix NFLX will report. Despite falling 72% since November, Netflix remains one of the largest companies in the market.

Warren Buffett’s Berkshire Hathaway (NYSE: BRK/A) continues to add to its position in Occidental Petroleum OXY and now holds 19.4% of the company. According to an SEC filing, Berkshire purchased more than $100 million in OXY stock last Thursday and Friday.

After reaching its 20-month low, NCR NCR has rallied more than 9% after The Wall Street Journal reported that private-equity firm Veritas Capital was looking to buy the software company and take it private.

Finally, the housing market continues to show weakness as June building permits fell another 0.6% despite coming in higher than forecasts. Housing starts also fell 2% in June as well. On Monday, the NAHB Housing Market Index came in much lower-than-expected reflecting a major slowdown in home building.

Reviewing the Market Minutes

Stocks tried to move higher on Monday, hoping to add to Friday’s gains, but a lack of buying conviction caused the gains to evaporate. The Dow Jones Industrials ($DJI), S&P 500® index (SPX), and the Nasdaq ($COMP) ended the day 0.69%, 0.84%, and 0.81% lower.

Stocks really seemed to lose steam after a Bloomberg article suggested that Apple (NASDAQ: AAPL) plans to slow hiring and ease spending in some of its divisions in anticipation of an economic downturn.

The volume behind Friday’s rally was light and the inability to maintain Monday’s rally suggests that investors just weren’t interested in buying. On the bright side, they don’t appear to be interested in selling either.

Earnings reports thus far haven’t provided the catalyst to move them extensively either way.

According to FactSet, Q2 earnings season for the S&P 500 has been weaker than normal with the number of earnings surprises and the margin of positive earnings surprises smaller than previous periods. However, it’s still early with only 7% of the S&P 500 reporting by Friday.

Bank stocks had attempted to build on Friday’s rally with a sparkling earnings report from Goldman Sachs (GS) early yesterday. The PHLX KBW Bank Index (BKX) rallied 2.7% up to its late-June highs after GS reported, but apparently ran into a group of sellers and gave up its gains to close just 0.11% higher for the day. Earnings reports and guidance from banks have been mixed, and Bank of America’s (BAC) miss Monday morning depressed the group. However, after surrendering their earlier gains, GS still closed 2.51% higher and BAC eked out a gain of 0.03%.

Of the 11 sectors in the S&P 500, eight of them closed in the red. Energy was the top performer after a rebound in oil prices. WTI crude oil futures settled 5.2% higher on the day at $102.09 per barrel.

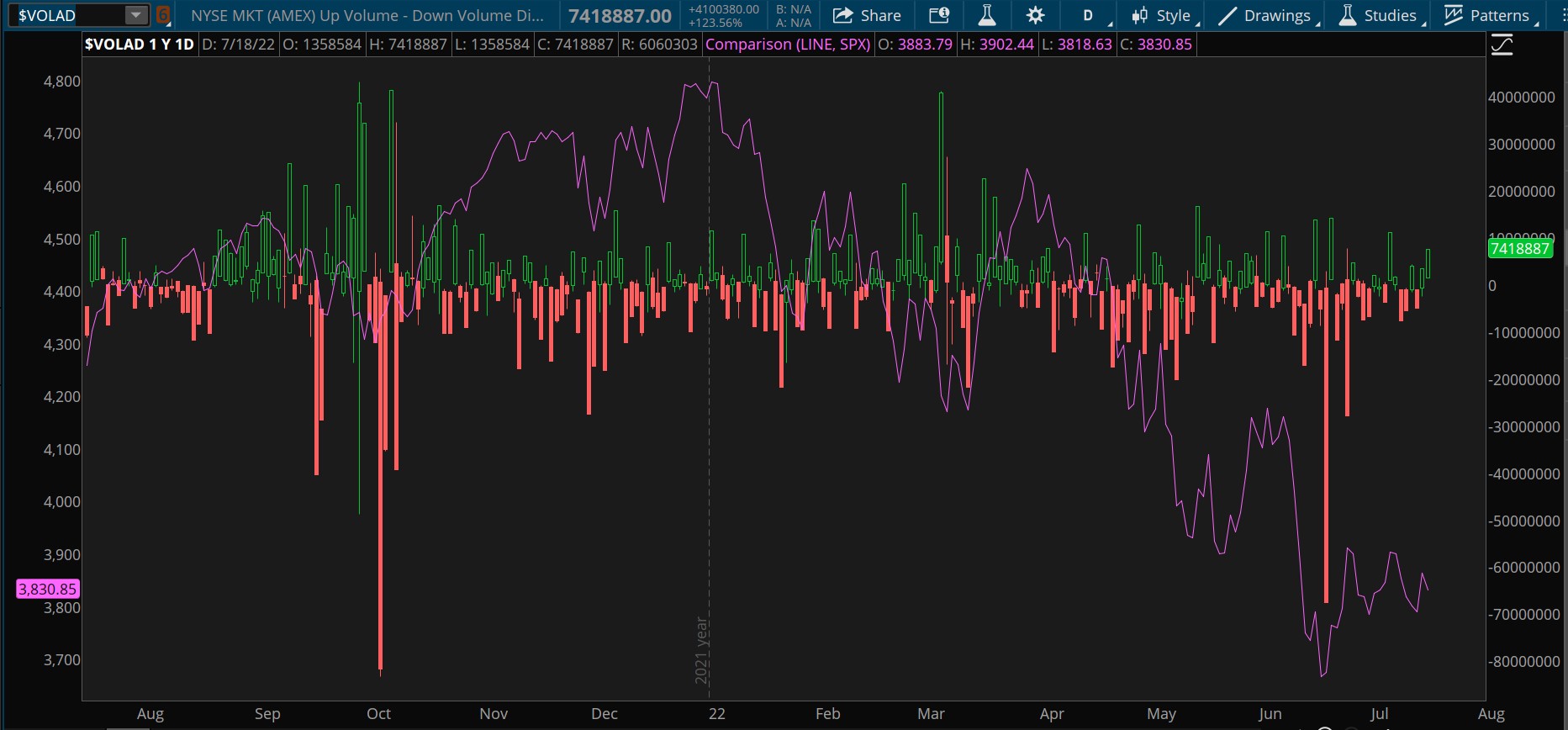

CHART OF THE DAY: CONVICTION. The NYSE Market Up Volume Minus Down Volume indicator ($VOLAD—candlesticks) helps to measure market breadth and investor conviction by comparing the trading volume of shares in advancing stocks versus the trading volume of shares in declining stocks. The S&P 500 (SPX—pink) tends to fall when declining volumes outpace advancing volumes. Data Sources: ICE, S&P Dow Jones Indices. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

CONVERSION: Despite the major indexes closing lower on Monday, the volume in advancing stocks was still higher than the volume in declining stocks for the second trading day in a row. While two days certainly don’t make a trend, if advancers can continue to attract more attention, investors may put more weight behind their conviction and put together a rally. However, the S&P 500 will have to sustain a break above its May lows and June highs if that rally is to have any legs.

ON THE MARGINS: While Q2 earnings season is just getting underway, FactSet is reporting that early reports are showing some compression in net profit margins for the second quarter in a row. So far, the blended net profit margin for the S&P 500 in Q2 is 12.4%. This is below the current Q2 estimate of 12.7% and below 2021’s Q2 margin of 13%.

With the tremendous rise in inflation, margin compression is expected to be an ongoing theme throughout this earnings season.

Still, it’s not all bad news. The Q2 net profit margin of 12.4% is still higher than the five-year average of 11.2% and above 2022’s Q1 average of 12.3%. How companies deal with higher input and labor cost is going to be vital for their earnings success.

INFLATION MYTH? If you’ve heard the idiom that “equities are a hedge against inflation,” then you may be wondering, “How can stock prices grow if margins are being compressed by inflation?” This is a good question. In fact, the CFA Institute shared research that shows that while equities tend to outpace inflation over time, it doesn’t necessarily mean they’re a hedge.

Looking at inflation from 1947 to 2021, the research found that average monthly return on equities at a zero rate of inflation is 0.7%. When inflation was greater than 0% but less than 5%, equities returns were 1.2%. Inflation greater than 5% but less than 10% coincided with returns of 0.9%. Finally, inflation greater than 10% saw returns of 1.2%. These numbers actually appear to confirm the market idiom—until you adjust returns for inflation. The real returns for each stage of inflation were respectively 0.9%, 0.9%, 0.4%, and 0.1%.

So, over the long haul, equities tend to outperform inflation by a wide margin. But it’s really more like a marathoner beating a sprinter over the long run.

Notable Calendar Items

July 20: Existing home sales and earnings from Tesla (NASDAQ: TSLA), Abbott Labs ABT, Kinder Morgan KMI, Biogen BIIB, and Baker Hughes BKR

July 21: European Central Bank interest rate decision, Philadelphia Fed Manufacturing Index and earnings from AT&T T, Philip Morris PM, Union Pacific UNP, Intuitive Surgical ISRG, and Freeport-McMoRan FCX

July 22: Earnings from Verizon VZ, American Express AXP, Schlumberger SLB, and Twitter TWTR

July 25: Earnings from NXP Semiconductors NXPI, and Whirlpool WHR

July 26: New home sales and earnings from Microsoft MSFT, Alphabet GOOGL, Visa V, Coca-Cola KO, McDonald’s MCD, United Parcel Services UPS

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.