(Thursday Market Open) Equity index futures were slightly lower ahead of the market open as investors sorted through a slew of economic data.

Potential Market Movers

The August U.S. Retail Sales report showed that consumers are starting to spend less. Core retail sales were expected to rise 0.1% but fell 0.3% month over month. Because the report isn’t adjusted for inflation, the decline in retail spending may be worse than what is reflected in the numbers.

Another sign of economic slowing came from the Philadelphia Fed Manufacturing Index which came in at -9.9 instead of the projected 2.8. The report reflects a slowdown in manufacturing orders.

On the other hand, the weekly jobless claims report was better than expected, which means the labor market remains tight. The Federal Reserve has been concerned about the tight labor market and its inflationary pressures on the economy. Investors are usually concerned about the effects a tight labor market has on a company’s earnings as labor expenses rise.

Unfortunately, these reports in light of this week’s hotter-than-expected Consumer Price Index (CPI) appear to paint a picture of stagflation. Stagflation is commonly defined with high unemployment, which is likely to come eventually. But, at this time, the strong labor market is playing big on the inflation side of the story.

In other news, railroad stocks were moving higher after the White House announced that the railroad companies and their unions have reached a tentative deal. The railroad workers were at risk of striking or being locked out by management which would have crippled the U.S. economy. Railroads carry almost 30% of the country’s freight and a work stoppage could have cost the economy $2 billion a day if shut down.

The Biden administration was scrambling to help broker a deal with the secretaries of labor, transportation, and agriculture all attending bargaining meetings over the last week. President Joe Biden personally reached out to the unions that were holding out to help push the deal forward.

The deal still has the be voted on but major carriers CSX CSX, Union Pacific UNP and Norfolk Southern NSC were up 2.4%, 2.8% and 2.5% respectively in premarket action.

Humana HUM was up 5.43 % in premarket action after raising its forward full-year earnings guidance. HUM cited lower than expected medical costs as a reason for the adjustment.

Adobe ADBE was down 8.89% in the premarket on the news that the company was looking to acquire private design firm Figma for $20 billion. ADBE is slated to report earnings after today’s close.

Reviewing the Market Minutes

Yesterday, the August Producer Price Index (PPI) showed that wholesale inflation moved as expected in August, falling 0.1%. However, the year-over-year (YOY) rate was actually lower than expected at 8.7% instead of the 8.8% target. Core inflation—which removes the more volatile oil and food prices—was hotter than expected, rising 0.4% in August instead of the forecasted 0.3%. Year over year, the core number came in at 7.3%, ahead of the projected 7.1%.

After Tuesday’s massive sell-off in reaction to the CPI report, stocks managed to hold their ground. The Nasdaq ($COMP) rose 0.74%, the S&P 500® index (SPX) increased 0.34%, and the Dow Jones Industrial Average ($DJI) eked out a 0.10% gain.

Investors may still be feeling a little shellshocked as the Cboe Market Volatility Index (VIX) pulled back a little from its high yesterday but remained elevated compared to its August lows.

The 10-year Treasury yield (TNX) jumped out of the gate Wednesday morning with a gain of five basis points to 3.47%, but later retraced that move and closed a single basis point lower to 3.41%.

WTI crude oil futures rose 1.3% to $88.58 per barrel on another day of volatile trading. The commodity has risen four out of the last five trading days and gained about 9%. The White House appears to be building a “floor” for oil, saying that it would start refilling the strategic oil reserves when the price falls to $80.

Rising oil prices helped the energy sector to rally with the Energy Select Sector Index surging 2.77% by the close. The materials sector was hurt by earnings warnings from Nucor (NUE) and Eastman Chemical (EMN), which fell 11.3% and 1.5% respectively. The Materials Select Sector Index dropped 1.23%.

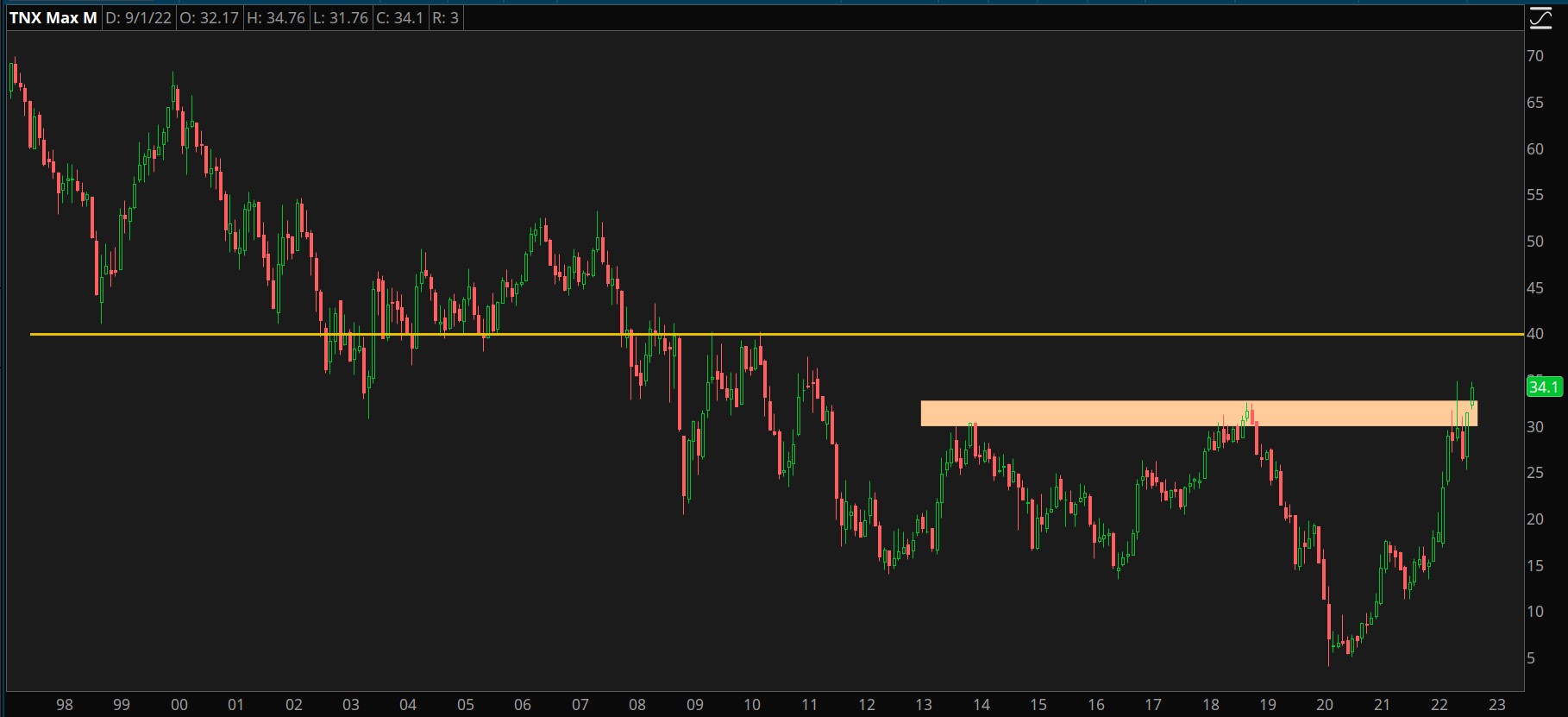

CHART OF THE DAY: The 10-year Treasury yield (TNX—candlesticks) is trading above its nine-year highs. In June, the 10-year yield was in this area but failed to hold. However, after this week’s inflation data, the markets may be ready to buy into the Fed’s hawkish tone which could sustain yields at this higher level. If inflation persists, the next level of resistance appears to be around 4%. Data Sources: ICE, S&P Dow Jones Indices. Chart source: the thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

Three Things to Watch

SECTOR SELECTION: BofA Securities’ Savita Subramanian told CNBC on Tuesday that she would avoid technology for the “foreseeable future” because of rising yields and a higher discount rate. Instead, the firm’s head of U.S equity and quantitative strategy suggested focusing on groups that are likely to see a more traditional surge in capital expenditures (capex) like those in the industrial sector. Due to rising inflation and a tight labor market, she pointed to automation companies as a potential beneficiary of capex spending. However, she didn’t expect to see a lot of capex investing in energy.

BALTIC STATES: The Baltic Dry Index (BDI) has fallen 50.3% YOY since the first of the month largely due to lockdowns in China and the Russia-Ukraine war. However, the BDI, which measures the cost of shipping goods around the world, has experienced a 13.3% surge over the last six weeks according to Trading Economics. Growth in the BDI is commonly considered a good sign that the economy and suggests that supply lines are normalizing.

Shipments in iron ore and coal have jumped 45% in a little over a month. As of Wednesday, coal and grain cargoes had risen 3.4% over the previous 10 days to a new two-month high.

The international shipping association BIMCO projects that shipping volumes will continue to grow between 1% and 2% through the end of the year and then increase 2% to 3% in 2023.

PRIVATE PLACEMENTS: Private equity companies have steadily been asking for more money from their investors, according to FactSet. A capital call is when a private equity fund exercises an agreement with its investors that requires investors to give them more money when needed. This is commonly done to help create and close deals. Using data from Cobalt, FactSet found that contributions as a percentage of unfunded obligations have risen from a low of 17% in 2009 to nearly 50% in 2021.

Rising capital calls could result in large investors taking from other investments like stocks and bonds and putting that money into private equity. The Federal Reserve’s easy money policies over the last decade and a half allowed large investors to borrow money at really low rates to fund capital calls, which left other investments in place. However, today’s higher rate environment means that investors are more likely to shift money than borrow money—which could result in the selling of stocks and bonds.

Notable Calendar Items

Sep 16: Michigan Consumer Sentiment

Sep 19: Earnings from AutoZone (AZO)

Sep 20: FOMC meeting begins, Building permits and Housing starts

Sep 21: Existing home sales, FOMC interest rate decision and Fed Chairman Powell’s press conference, and earnings from General Mills (GIS), Lennar (LEN), H.B. Fuller (FUL), and KB Home (KBH)

Sep 22: Earnings from Costco (COST), Accenture (ACN), FedEx (FDX), FactSet Research (FDS), and Darden Restaurants (DRI)

Image sourced from Shutterstock

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.