My last recommendation was new to the value-investing club (see Buy CSCO CSCO : A Treat For Value Investors). This week, I bring back a classic value stock: Phillip Morris PM.

Focusing on the reported GAAP earnings of PM leads investors down the wrong path. Too many of my peers get lost in debt ratios, quick ratios or price-to-earnings ratios. These analyses miss the mark and do not capture the strength of PM’s underlying cash flows.

I recommend investors arbitrage the market’s disconnect in valuing PM based on GAAP earnings instead of its true economic earnings. My model shows that the marke’st expectations for PM’s future cash flows are lower than the consensus estimates for GAAP earnings.

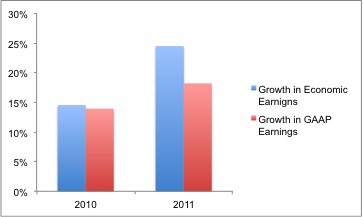

I believe this disconnect arises from the difference between PM’s GAAP earnings and economic earnings. Figure 1 shows how PM’s economic earnings over the past two years are growing faster than GAAP earnings.

One of the differences in economic and GAAP earnings for PM is the hidden, unusual charges that we remove from the company’s “marketing, administration and research costs” and “cost of sales”. In 2010, we remove $97mm; in 2011, we remove $125mm. The adjustments come from careful review of the MD&A section of the company’s 10-K report.

The biggest driver of the difference between economic and GAAP earnings is the company’s improved capital efficiency, which manifests in our model as more revenue per dollar of invested capital. Phillip Morris’ margins are rising. Everyone can see that. What other analysts are missing is that the company is getting more revenue out of each dollar of capital as well.

Figure 1: More Profitable Than Meets the Eye

Sources: New Constructs, LLC and company filings

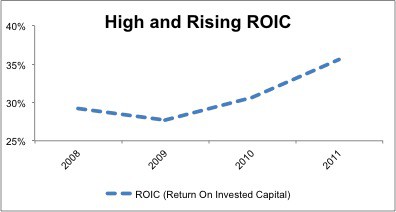

Rising margins and rising capital efficiency drive rising returns on invested capital (ROIC). A rising ROIC is exactly what investors want to see. Figure 2 paints a pretty picture of PM’s rising ROIC over the past couple of years. Note that PM’s ROIC is not only rising, but it is also significantly higher than its weighted average cost of capital (WACC), which we currently estimate at 5.2%. For profitable company’s like PM, a high debt-to-capital ratio is good for equity investors because it lowers the company’s WACC.

Figure 2: ROIC Easily Exceeds WACC at 5.2%

Sources: New Constructs, LLC and company filings

As my regular readers know, a profitable company is not always a good stock. To be a good stock, the market’s valuation has to imply the company will generate lower cash flows than what I expect (see “How To Make Money Picking Stocks”).

PM fits the bill for a good stock. It’s current price, ~$90/share, implies a permanent 4% decline in the company’s after-tax cash flow (NOPAT). The stock is worth over $94/share if the company’s profits never grow again. The take away is that market expectations for PM’s future cash flows are quite low.

Figure 3: Good Company and Good Stock

Sources: New Constructs, LLC and company filings

PM fits the bill for a good stock. It’s current price, ~$90/share, implies a permanent 4% decline in the company’s after-tax cash flow (NOPAT) from 2011. The stock is worth over $94/share if the company’s profits never grow higher than 2011’s level.

Consensus earnings estimates are currently forecasting 6% growth for 2012 and 11% growth for 2013! By focusing on economic earnings instead of GAAP earnings, we find an arbitrage opportunity and can exploit the misguided focus of the majority of investors on GAAP earnings.

I am not a smoker and never will be. However, I cannot deny the profit advantage that addictive products tend to have over products that are not addictive. And addictive products not only deliver higher profit margins, they also maintain steadier revenues as large numbers of users are not likely to quit cold turkey even if they know the product is killing them. In other words, I doubt PM’s profits will decline as the market price implies.

On the contrary, I think PM’s growth potential is solid. The company’s focus on international markets means it is targeting less mature and less saturated audiences for its products. The Marlboro man is no longer a common sight domestically, but he looms large in foreign markets.

Put simply, PM has the strongest brand in one of the world’s most profitable products. And it is focused on markets where demand for its products is growing. I see great growth potential. It may be slow and steady, but that is often how the stock market race is won.

PM’s high profits and low valuation earn it my Very Attractive rating. PM was also recently added to my Most Attractive Stocks list for August.

As my regular readers know, I also cover 7400+ ETFs and mutual funds. My predictive fund ratings leverage the deep research I do on all of the 3000+ stocks covered by my firm, New Constructs.

The ETFs and funds that allocate 8% or more of their portfolio to PM and get an Attractive rating are:

- Consumer Staples Select Sector SPDR XLP

- iShares Dow Jones U.S. Consumer Goods Index Fund (NYSE: iYK)

- Vanguard Consumer Staples ETF VDC

- Vanguard World Funds: Vanguard Consumer Staples Index Fund VCSAX

- ICON Funds: ICON Consumer Staples Fund ICLEX, (ICRAX) and (ICLCX)

New Constructs’ free fund screener provides free reports on 7400+ mutual funds and ETFs, including all of the funds mentioned in this article.

Disclosure: I am long PM. I receive no compensation to write about any specific stock, sector or theme.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.