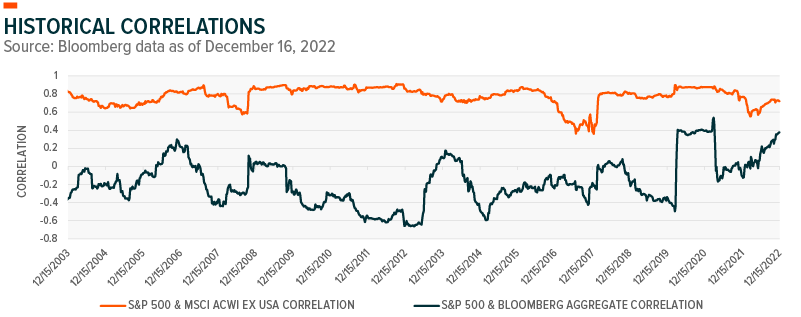

Rising Asset Correlations Went into Overdrive In 2022

Correlations across U.S equity, international equity, and fixed income rose in 2022 as global central banks increased policy rates to reduce consumer demand and curb inflation. For fixed income, the worst may have passed as the Federal Reserve (Fed) approaches a terminal rate of about 5%. For international markets, some headwinds have dissipated, while growth expectations in the U.S. have deteriorated slightly. As correlations between asset classes decline, we expect markets to find a balance between growth and value. So far, there have been clear winners and losers on the sector front, evidenced by the severity and breadth of the declines. This disparity could create investment opportunities, but selectivity will be key across asset classes and sectors amid tighter financial conditions.

Declining Correlations Could Create Opportunities In 2023

Conditions could be aligning for correlations between U.S. equities and fixed income to decline. The speed of rate increases in 2022 caused aggressive repricing in bonds and U.S. equities simultaneously. As the Fed policy rate nears 5.0%,1 the pace of rate hikes may subside.

Another factor is the cloudy outlook for U.S. equities in the first half of 2023 with investors expecting earnings contraction. About 55% of S&P 500 companies and 71% of the Nasdaq are trading below their 200-day moving averages (MA).2 In December, the estimated Q4 year-over-year earnings growth rate for the S&P 500 was revised to -2.8%, well below the 3.7% estimate at the start of the quarter.3 Weaker earnings growth could occur alongside rising recession risks, evidenced by the Conference Board Leading Economic Index’s (LEI) steep decline after peaking in February of 2022.4 The Conference Board projects a U.S. recession to occur around the beginning of 2023 and last through mid-year. In the meantime, a recession could lead to less restrictive monetary policy, creating investment opportunities.

Asset class correlations ebb and flow, as seen in the chart below, which measures 1-year correlations using weekly rolling data over the past 20 years. To buffer the impact of market downturns on overall investment returns, investors can build diversified portfolios that include assets with low correlations.

Improving Global Opportunities

International markets may benefit as peak pessimism fades. European energy shortage fears have dissipated with gas storage adequate for the winter, while China shifting away from their zero-COVID policy reflects an increased prioritization of economic growth. Thematic equity is global in nature and potentially stands to benefit from improving global opportunities. However, with slower global economic growth and restrictive financial conditions, this is an important area to be selective. Clean tech, clean energy, cybersecurity, and robotics are a few themes that we believe continue to have structural tailwinds in the current environment.

- Clean Energy and Clean Tech: The war in Ukraine highlighted the need to expand clean energy infrastructure and clean tech investment in Europe and beyond. Beyond the focus on renewable solutions, this conflict highlighted the importance of energy independence.

- Cybersecurity: Heightened cybersecurity risks are a tailwind for topline growth. In the near term, we expect cybersecurity revenue to grow faster than the economy or the broad market.

- Robotics & Artificial Intelligence: Broad structural forces are increasing the need for improved efficiency, driving increased demand for automation.

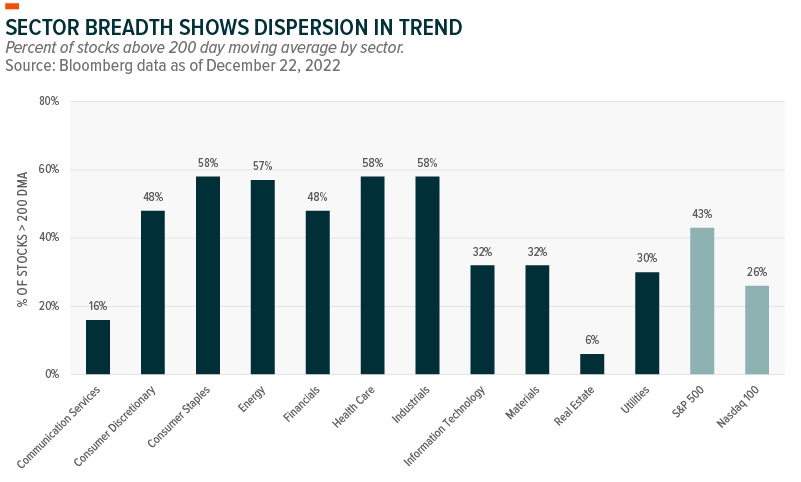

Sector Selectivity Will Be Key

Dispersion in sector price trends could narrow in 2023 as growth headwinds subside. The chart below shows the percentage of stocks in each sector trading above their 200-day moving average. Consumer Staples, Energy, Health Care, and Industrials have maintained their respective uptrends, especially relative to the S&P 500. However, Real Estate, Materials, Industrials, and Communication Services have significantly lower breadth readings. The weaker economy weighed on cyclical sectors, while rising interest rates adversely impacted high valuation growth sectors.

Breadth can also be a measure of overbought or oversold conditions. Stocks tend to revert to the mean after trading well above or below their 200-day moving averages. Investors may expect a catalyst to balance the scale between growth and value. A slower pace of rate hikes could benefit long duration assets, while improved global growth prospects may positively impact cyclical growth sectors relative to defensives. For now, there is still room for earnings expectations to decline, which could present downside risks in H1 2023.

Lower Earnings Expectations Closer To Reality

The S&P 500’s expected year-over-year earnings growth rate for 2022 is 5.1% (-1.8% excluding Energy), compared with estimates of 9.1% in June and 6.9% in September for the same period at different times.5 Lower expectations from 2022 will likely feed into 2023 alongside a decline in Buy ratings.

Energy, Communication Services, and Information Technology have the highest percentages of analyst Buy ratings, while Consumer Staples and Utilities have the lowest. The concentration of Buy ratings is essentially an inverse of the breadth chart above. December 2021 had a similar makeup of Buy, Hold, and Sell ratings, although sector performance outside of Energy greatly disappointed consensus ratings in 2022.6

Despite bearish earnings expectations, investors can still find opportunities. Positioning between sectors will be an important consideration for portfolio diversification in 2023. Declining earnings expectations and the normalizing correlations between stocks and bonds could cause a shift in the relative volatility between equities and bonds. Therefore, a tilt toward defensive and quality sectors could mitigate downside risk. However, as global growth conditions improve, growth sectors could gain, creating opportunities for thematic equities. Some of our high-conviction themes include Cybersecurity, Infrastructure, and Clean Energy, with each benefiting from improving demand.

Our sector views table below provides more detail on sector positioning and the current tailwinds and headwinds for each sector.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.