Video games in the Asian markets boasts a global reputation. While Japan is already well-established in console gaming, South Korea has international prestige in online gaming and esports. The winds of change are blowing as the era of interconnected gaming requires console giants to rethink their approach, with esports becoming increasingly normalized alongside traditional sports, and new competitors in China and Southeast Asia expanding their foothold in the international gaming industry.

In this piece, we will explore how the paradigms of the video game industry are shifting in East and Southeast Asia. Specifically, we will cover:

- Japanese gaming giants that established themselves on consoles are not only adapting to mobile gaming, but are also preparing for next generation technologies

- Why regulatory approval trends could be indicative of a change in quality for Chinese-developed games, and why Chinese game developers are looking abroad amid domestic regulatory pressure

- South Korea’s 5G leadership could translate into leadership in cloud gaming and how Southeast Asia is helping normalize esports as a real sport

Asian Gaming at the Intersection of Multiple Trends

The economic and demographic differences within East and Southeast Asia imply different needs for gamers in each market. As an example, while Japanese game makers need to make games more inclusive for an older population, Vietnam is still working with a young and tech savvy population. Meanwhile, new trends such as 5G, cloud gaming, virtual reality and esports, that are revolutionizing gaming everywhere are impacting Asian game makers in different ways.

Japanese Console Giants Adjust for Era of Mobile and Interconnected Gaming

Gaming consoles by Nintendo and Sony helped make Japan a powerhouse in the video game industry. The success of recent titles like Animal Crossing prove console gaming is still strong, but Nintendo, Sony and other game makers are increasingly cognizant of the changing realities of the modern gaming market. Smartphone gaming already rose significantly over the past decade and the advent of cloud gaming, 5G and other technologies are transforming traditional notions of console gaming.

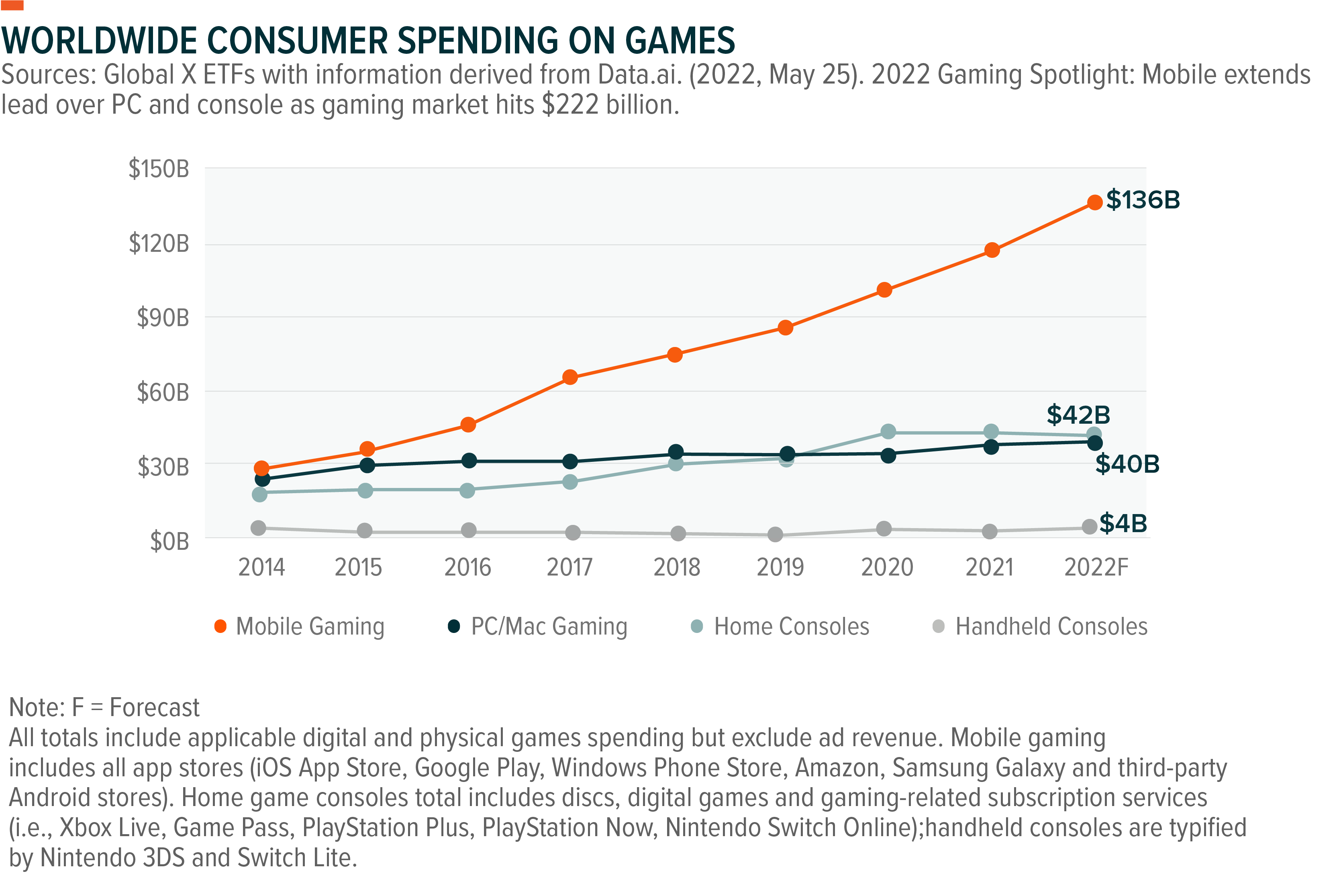

Mobile gaming is where much of the growth in spending has been in the past eight years.

Nintendo began its experiment with smartphone games in 2016, though those games and other IP related income only comprised 3.14% of Nintendo’s revenue in Fiscal Year (FY) 2022.1 For now, these games serve the purpose of expanding Nintendo’s brand recognition, particularly in countries where the Nintendo Switch is not available.2 While Nintendo’s future in smartphone gaming remains uncertain, the massive success of the Nintendo Switch, a high-power console that can be both plugged into a television or played on-the-go, unseated Sony’s PlayStation Vita and established Nintendo as the dominant player in hybrid consoles. Further advances in cloud gaming and smartphone power will likely add pressure to not only normalize hybrid consoles, but to innovate and find new ways to differentiate consoles from other segments of the gaming market.

With Nintendo’s track record as a disruptor that brought gamers motion-controlled gaming through the Wii and a new form of hybrid console gaming through the Switch, we are optimistic about how Nintendo will respond to the opportunities and challenges created by cloud and mobile gaming.

Other Japanese giants are choosing to embrace mobile gaming more than Nintendo. Square Enix opened a dedicated studio for mobile gaming in London in October 2021 and is offering free-to-play titles with in-app purchases.3 Between FY2019 and FY2022, Square Enix’s revenue from games on smart devices and browsers rose from 41% to 46%, becoming the top contributor to revenue in the three most recent fiscal years.4

The initiatives by Japanese game makers go beyond mobile and cloud gaming, with technologies like AI and the metaverse entering the mainstay. In 2022, Square Enix joined hands with the Japanese game maker Gumi, which already has experience developing games that utilize NFT technology, in a deal to launch operations related to the metaverse.5 Sony is moving to launch the next iteration of its VR gaming headset, known as the Playstation VR2, in February 2023. As part of its medium-term plan, Bandai Namco Holdings is looking to invest $113.2mn into the development of IP related to the metaverse and other Web3 technologies.6

In embracing and experimenting with mobile gaming and other emerging technologies, Japanese game makers are learning how to balance the creative forces that made them unique with new models of monetization. Iconic brands that were once console exclusive are now appearing in app stores under the “freemium” model, namely in which games are made free-to-play but with in-app purchases. In this process, it is important for Japanese game makers to not allow the “freemium” model to wear down the creative flare that made their games loved around the world.

Chinese Game Makers Eye International Expansion After Regulatory Crackdown

2021 was a tumultuous year for Chinese equities as regulators moved to reform industries and business practices that they perceived to be producing costs for society. Among these was online gaming for minors. In Q4 2021, China introduced heavy restrictions on online gaming for minors, only allowing them to play for one hour on weekends and national holidays.

Although this had an adverse effect on sentiment towards China’s gaming industry, that effect was somewhat mitigated by the fact that most online gaming revenue comes from a top group of power-players as opposed to minors who are not economically independent and can only rely on their parents for gaming purchases. Total revenue of the video game industry continued to increase from 278.69bn RMB in 2020 and 296.51bn RMB in 2021, and first half (H1) 2022 revenue came in at 147.79bn RMB, implying the overall effects of the restrictions were somewhat constrained.7

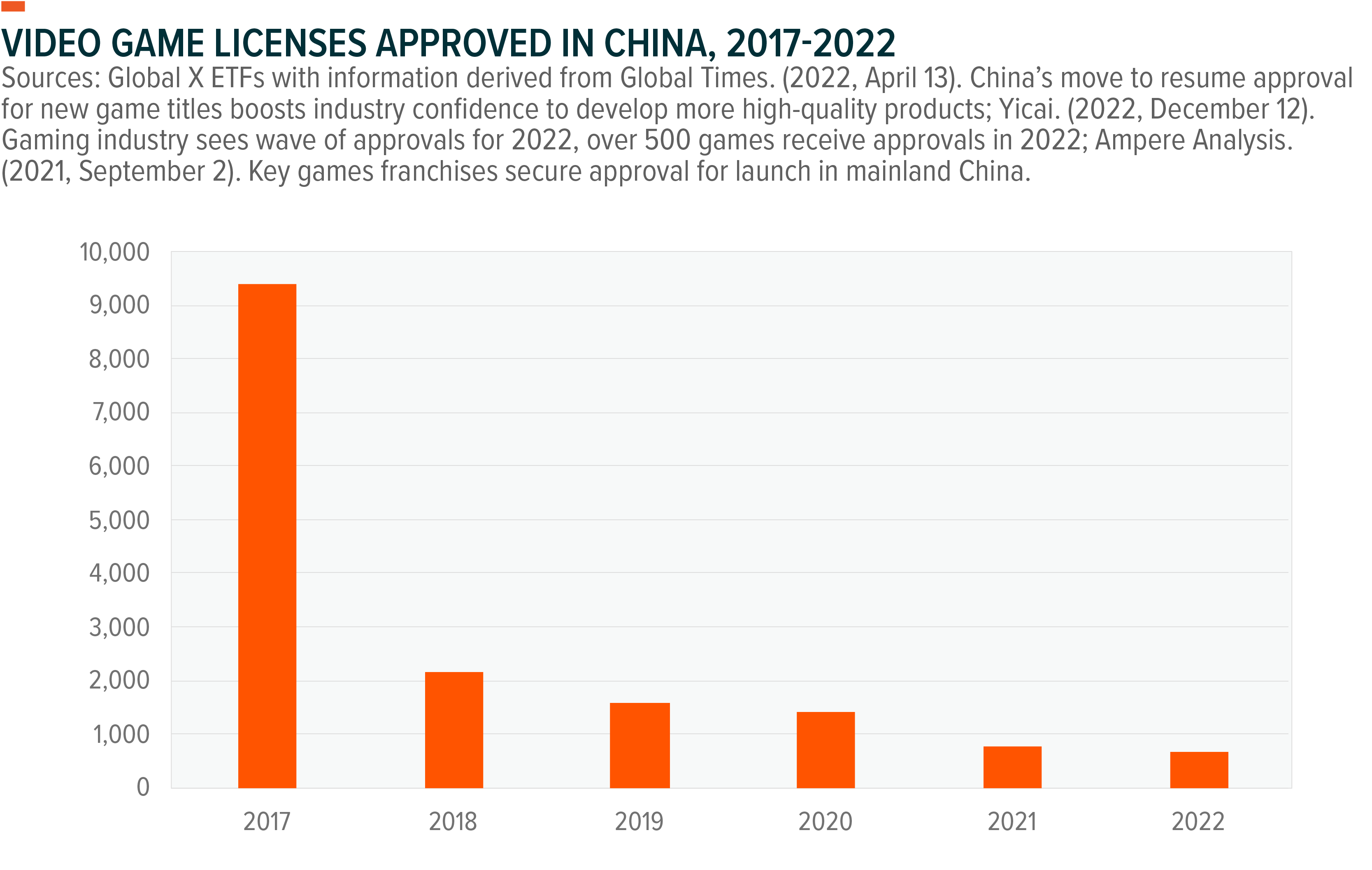

In 2022, game approvals helped thaw investor sentiment towards Chinese games. Game approvals are one of the indicators that can be used to get a sense of which way the regulatory winds are blowing. Over the course of 2022, investors looked towards batches of game approvals as signs of an easing in the regulatory crackdown. However, there is another side of regulatory approvals that is sometimes overlooked.

Zooming out beyond the past two years, recent trends in approvals seem to show a new emphasis on quality over quantity In fact, Chinese game approvals can be divided into three phases. Prior to 2018, regulators approved around 7000 games a year, which really gave room for games of various quality levels to enter the market. The relative ease of approvals incentivized some developers to churn out games fast, often at the expense of quality and creativity.

That changed when the number of gaming approvals abruptly dropped to 2141 in 2018. A higher hurdle to clear for regulatory approval meant developers had to tap the brakes and reassess their approach. The third phase began in 2021 as the number dropped to 755, only deepening the need for developers to prioritize not only quality but also attention to the social values being transmitted through their games. In this third phase of regulatory approvals, an increase in quality could go a long way towards improving the reputation of Chinese games.

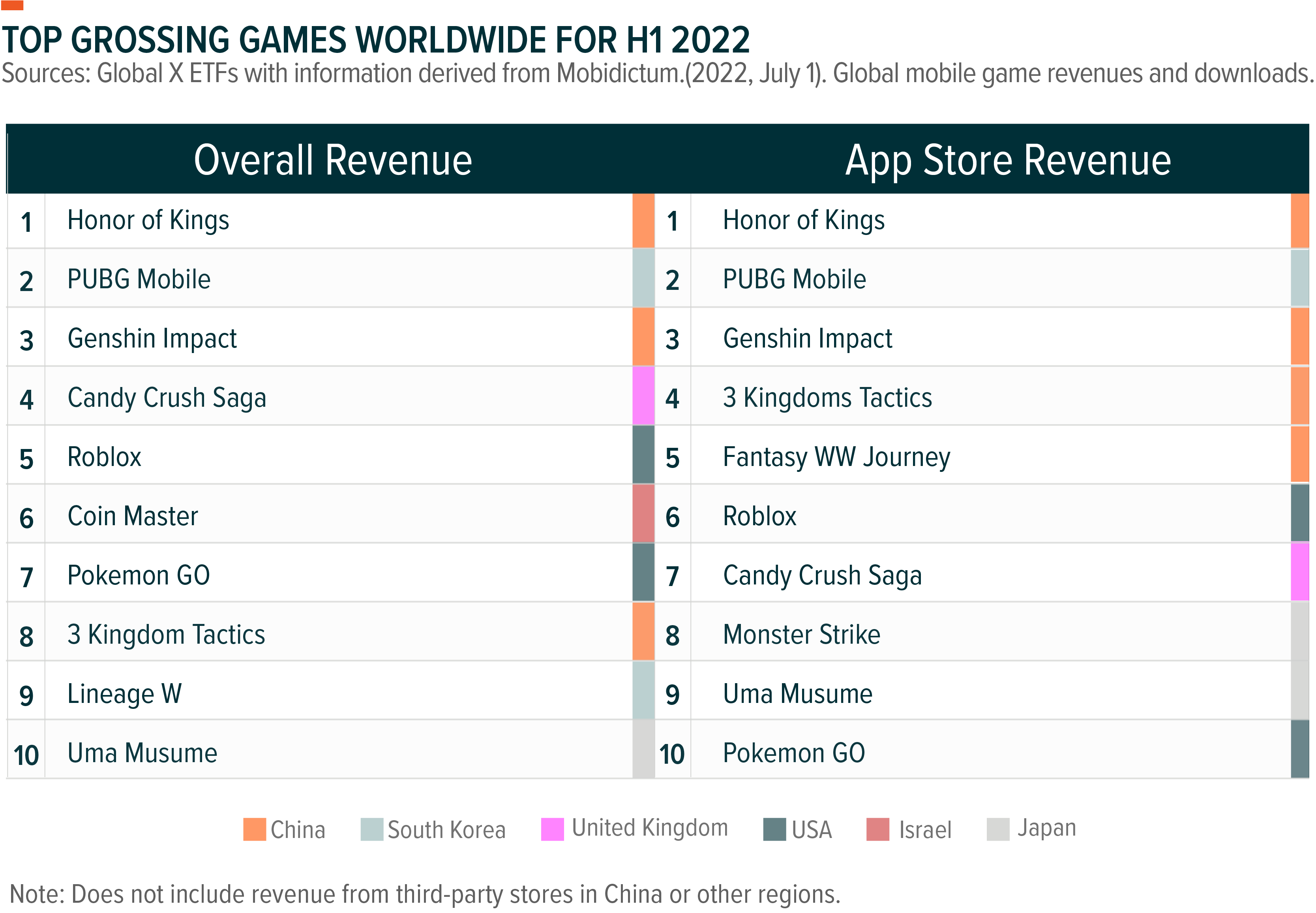

Such an increase in quality would be a crucial step in establishing international prestige. In the aftermath of tightened regulations, Chinese game makers also now have more global ambitions. Challenges exist but some early signs of potential success in the future are emerging. Genshin Impact, a co-op roleplaying (RPG) game developed by Chinese studio miHoYo, became a hit in 2020 on iOS, Android, and the PlayStation 4. With $986.2mn of revenue, Genshin Impact was the third highest grossing game worldwide in H1 2022.8

Genshin Impact shows the potential of Chinese-developed games to succeed on the international stage, albeit with challenges yet to be overcome. Critics of Genshin pointed out the game’s stylistic and mechanical similarities to Nintendo’s Legend of Zelda Breath of the Wild, underscoring the need for Chinese developers to continue working on originality and creativity as a prerequisite for international success.

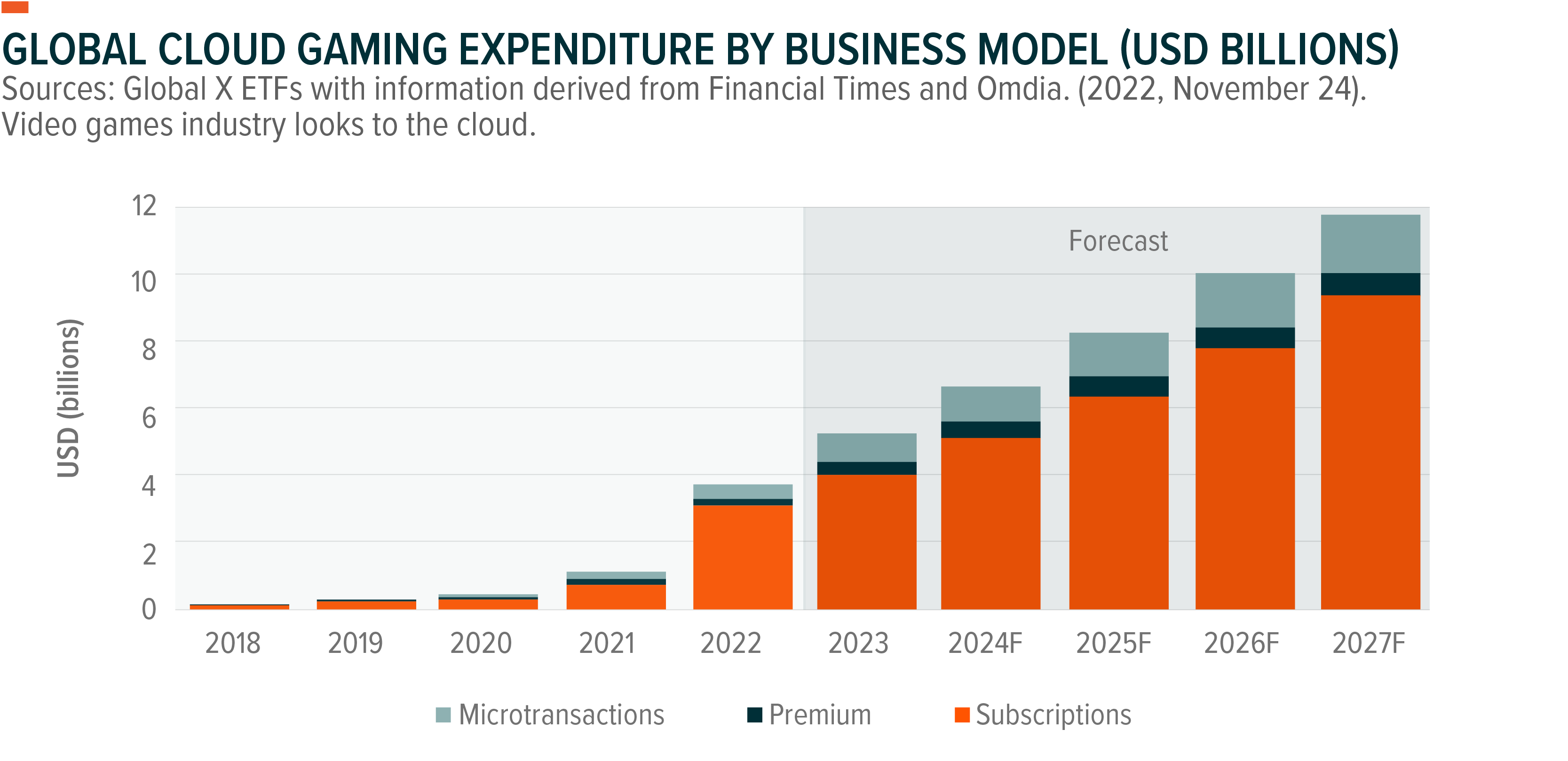

South Korean Telecom Firms Vie for Cloud Gaming Opportunities

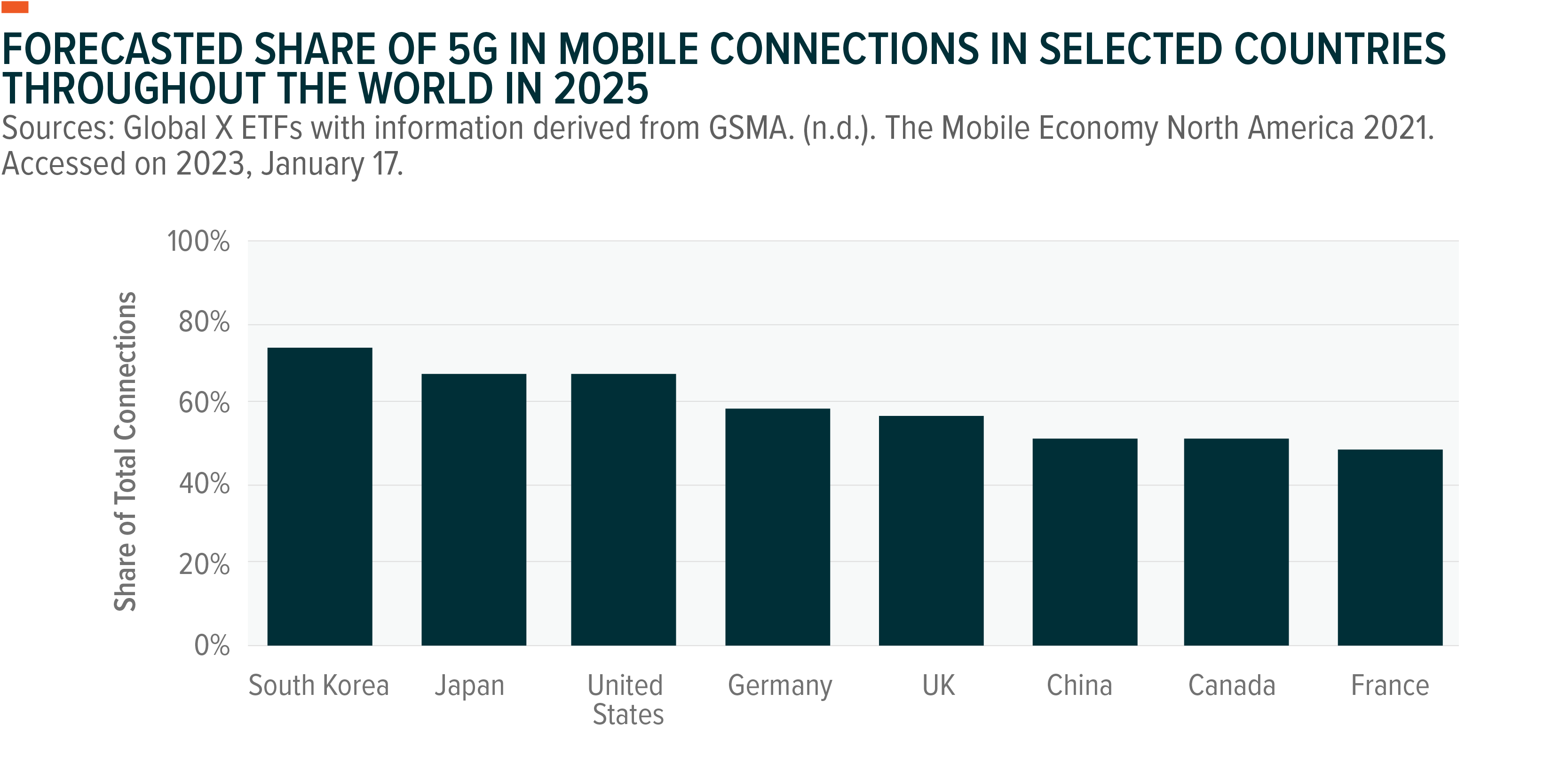

As a country known for advanced smartphones and high-tech infrastructure that includes a strong 5G network, South Korea appears well-positioned to be a leader in the adoption of cloud gaming in Asia. In particular, three South Korean telecom firms are leading the charge.

2020 is the year the race for cloud gaming dominance began in South Korea. Each of the major actors in this space are leaning into support from foreign partners like Microsoft, Nvidia and Ubitus. In 2020, SK Telecom worked with Microsoft to launch SKT 5GX Cloud Game, which allows players to access a large catalog of Xbox games for a monthly subscription fee.9 Meanwhile, KT launched the Gamebox cloud gaming service and worked with AskSys Co to build the SHAKS Gamepad, powered with Qualcomm technology.10 LGU joined the race by partnering with Nvidia to offer a 5G cloud gaming service called GeForce NOW.11 With cloud gaming expected to grow globally on the back of rising subscription revenues, a lot of value could be captured by South Korean services.

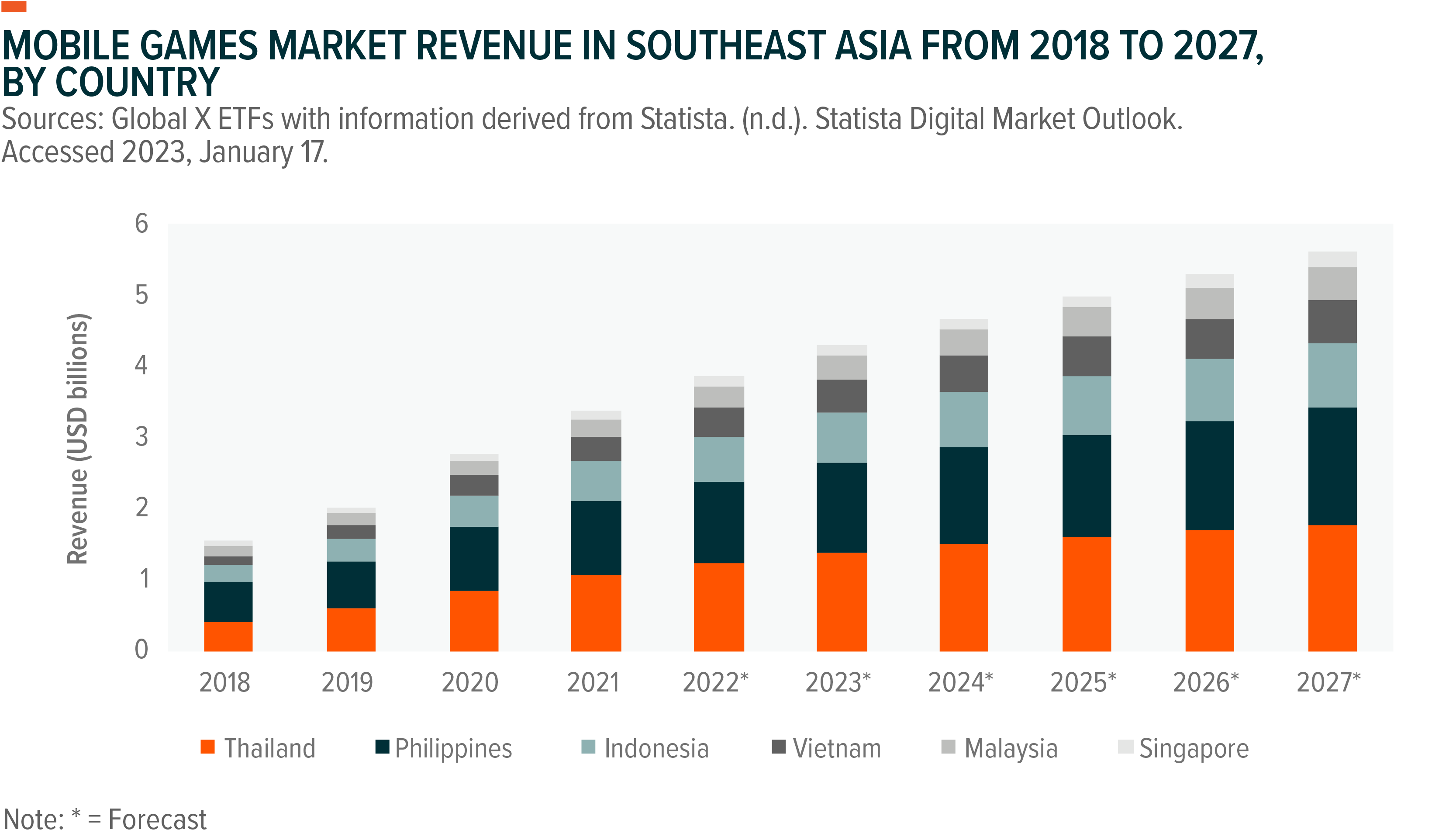

Southeast Asia Becomes Hub of Esports and Mobile Gaming

Esports are not typically given the same treatment as traditional sports like football or basketball. That is beginning to change and, surprisingly enough, much of that change is happening in Southeast Asia. As a testament to that, the 2019 Southeast Asian Games in Manila, Philippines included esports alongside traditional sports for the first time in the world at an event affiliated with the International Olympic Committee (IOC). Malaysia became the home of the country’s first esports hotel with the opening of SEM9 Senai esports Hotel in June 2022.12 In June 2023, Singapore is set to host the inaugural IOC-sponsored Olympic Esports Week, underscoring the important role Southeast Asia is playing in normalizing esports.13

The normalization of esports is reflected in the data for Southeast Asia, which shows rapid growth of revenue for esports. Within Asia, Southeast Asia is expected to have the second fastest revenue growth in esports in 2022 at around 17.2%, behind India at 18.3%.14 Esports companies are catering to a group of consumers that are relatively young, particularly compared to the neighboring Northeast Asian region. Young consumers tend to be tech-savvy and that is also becoming a tailwind for the growth of mobile gaming revenue. If countries like Indonesia, Vietnam, Thailand, and the Philippines continue to grow, the resulting growth in discretionary income will likely boost revenue for mobile games.

Conclusion

Asia played a significant role in the rise of video games and it should continue to be a source of both new consumers and fresh paradigms of the gaming experience. Rising interest rates and macro headwinds will likely drag down returns for video game stocks for at least part of 2023, as they did in 2022. However, innovation never stops. The efforts of Japanese video game makers to incorporate emerging technologies and Southeast Asia’s role in normalizing esports is a testament to that. We see Asia as a crucial part of the investment thesis behind the video games theme. As 2023 shapes up to be a potentially exciting year for generative AI technology, which is already being applied to video game development, the entire industry both abroad and in Asia could see increases in productivity and new modes of development.

Related ETFs

HERO – The Global X Video Games & Esports (HERO)

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.