S&P 500 companies grew capital expenditures (CAPEX) by 19.8% in 2022. With structural tailwinds this could be the beginning of a new CAPEX cycle, benefiting certain sectors and themes. Despite macro uncertainty, CAPEX spending is expected to increase by 6% in 2023, outpacing revenue and earnings growth expectations.1 We expect further capital investment due to labor market imbalances, continuous supply challenges, and the energy transition. Infrastructure, robotics/automation, and clean energy could gain the most from the next wave of spending. At the same time, companies may have to balance the higher cost of capital and labor to achieve productivity gains.

The Missing Labor Link

The impact of the pandemic on the labor force can still be felt today, even with an unemployment rate of 3.5%. The participation rate, which is the sum of employed and unemployed civilians divided by number of people in the labor force, dropped from 63.3% in January 2020 to a low of 60.1% in April 2020 and has recovered to around 62.3% for the past year.2 For the participation rate to be at the same level as pre-pandemic another 2.6 million people need to be included.3 So, where did this group go?

Employment rates in the United States, from beginning of 2020 to end of 2022, decreased by -5.6%.4 When isolating the data to only reflect low wage labor, where low wage is defined as an annual income below $29K, there is an estimated -21% decrease in employment.5 This reduced supply of labor has created structural constraints in the labor market, specifically in low wage work, where employers now have a growing need to substitute labor for capital. To solve for this companies have been investing more in capital expenditure (CAPEX) to automate their processes, boost productivity, and reduce the need for unskilled labor.

Companies Focus on Productivity

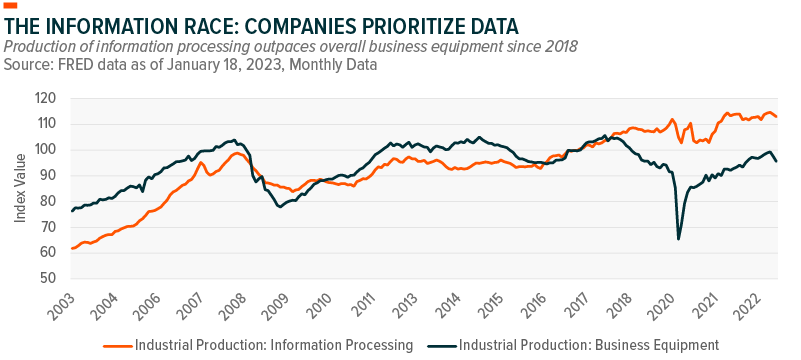

Productivity, or creating more per unit of input such as capital and labor, can help companies remain lean during economic downturns. The chart below shows a steady rise in industrial production focused on information processing, which outpaced overall business equipment production over the past four years. We expect digitization to be a focus of capital spending over the coming years.

Our sector views table below provides more detail on sector positioning and the current tailwinds and headwinds for each sector.

This post contains sponsored advertising content. This content is for informational purposes only and not intended to be investing advice.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.