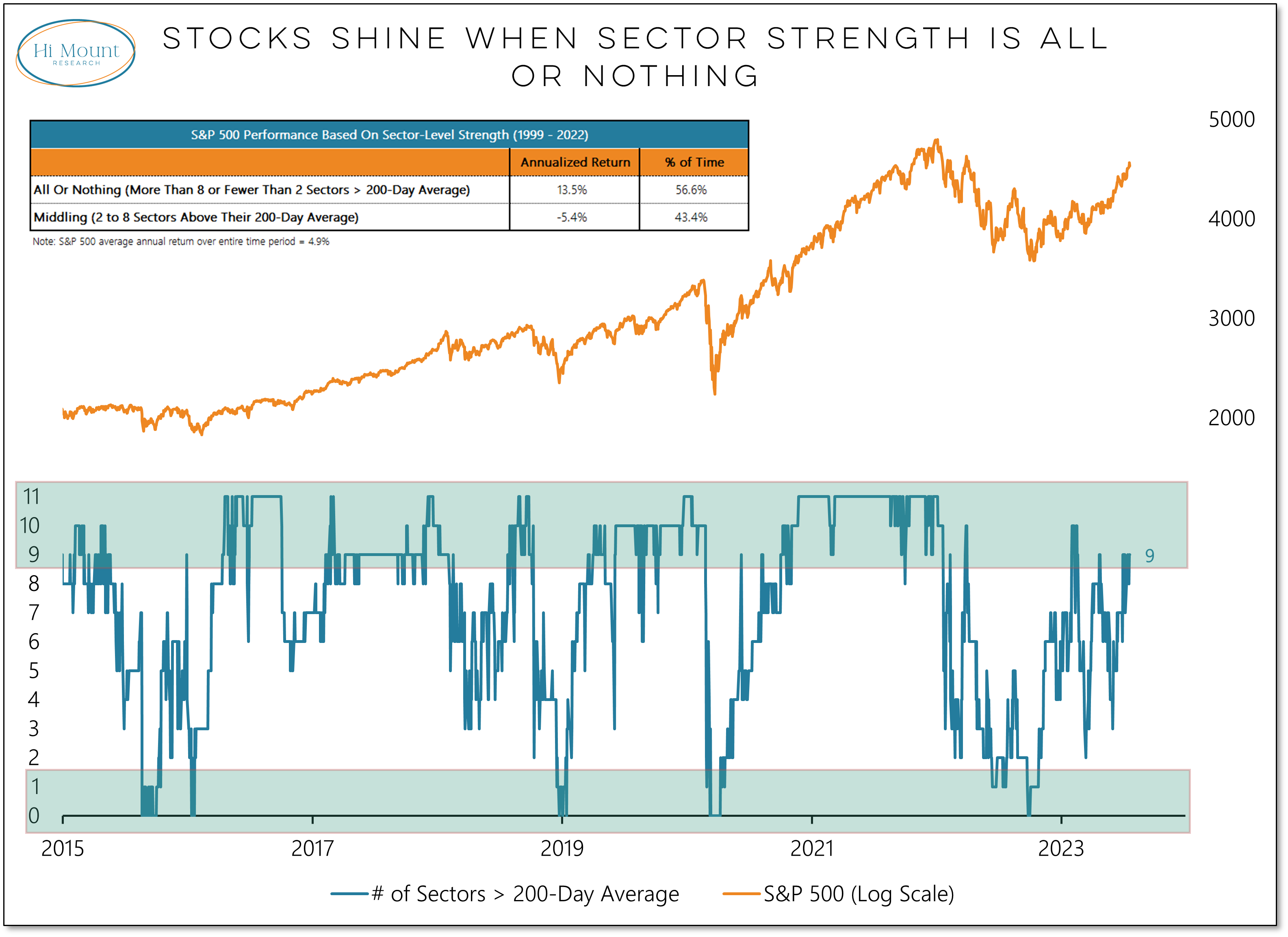

Key Takeaway: Equity call volume is surging but with sector-level trends having improved, the crowd may be justified in looking for higher prices.

This model is the sector-level corollary to our overall Fear or Strength model, which is positive in the face of either strength (new highs > new lows) or fear (VIX > 28.5). Concerns about speculative excesses are mitigated as long as the market continues to produce strength.

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

To add Benzinga News as your preferred source on Google, click here.