According to minutes from the FOMC’s July 25-26 policy meeting, most participants continued to be concerned by “significant upside risks to inflation.” The hotly anticipated transcript provides market participants with an opportunity to gauge the US central bank’s thinking regarding the likely path ahead for US rates.

This is especially valuable in August, with no FOMC meeting until September 20 the next opportunity for investors to study the Fed’s demeanour will be at the Jackson Hole symposium on Aug 24.

US equities extended losses following the release of the minutes, which further dampened risk appetites. Treasury yields and the US dollar also rose on the day. The tone of the minutes does indeed suggest a high degree of conviction and consensus among Fed officials regarding the Fed’s aggressively hawkish stance.

However, there are signs of growing dissension, with two FOMC members having favoured a pause at the previous meeting. The minutes also highlight a growing concern regarding the fear of overtightening, stating that the “risks to the achievement of the committee’s goals had become two-sided.”

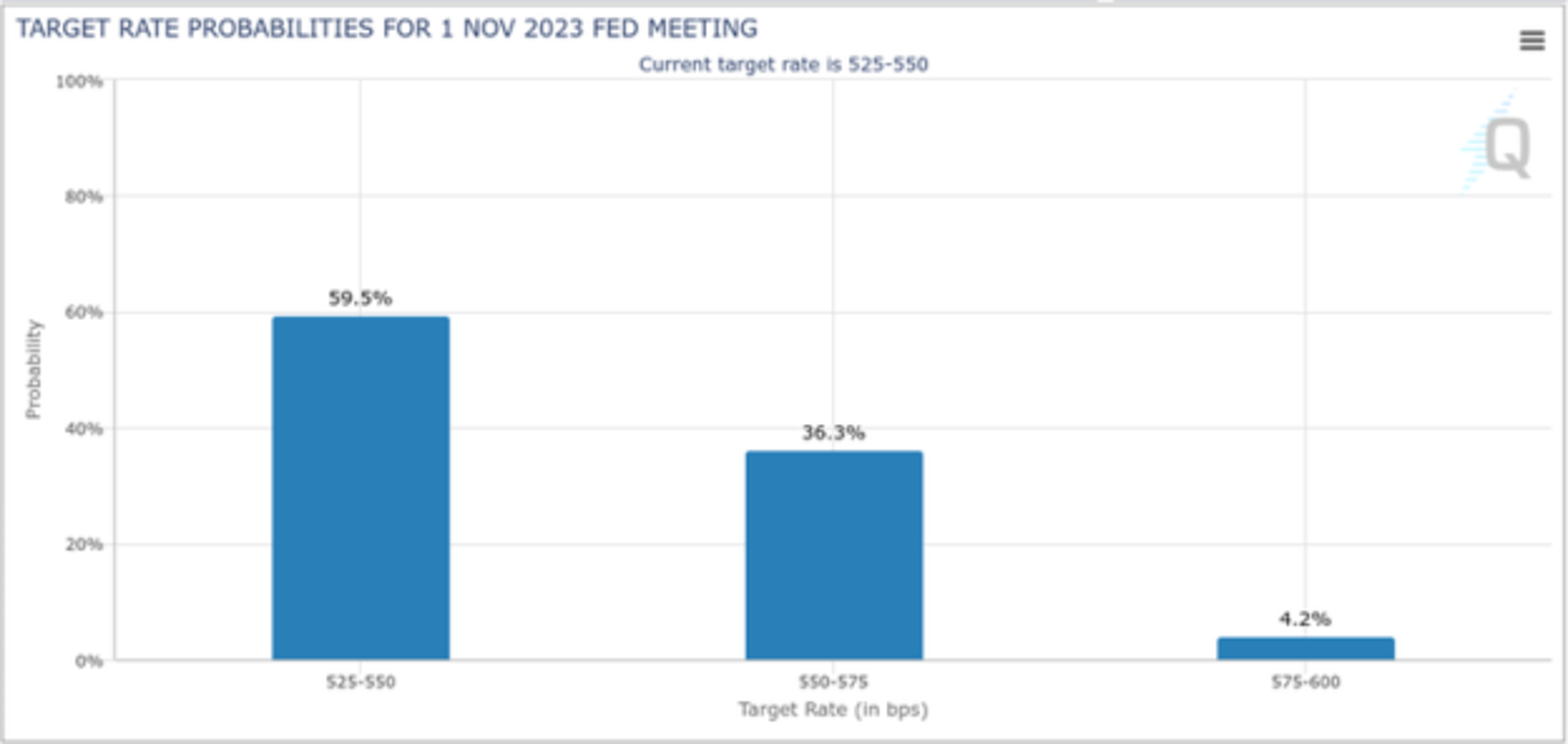

The CME’s FedWatch tool is currently predicting an 86.5% chance of the Fed keeping rates where they are at the next FOMC meeting in September, with slightly lower odds (59.5%) of it also pausing at the November meeting.

Shifting Narratives

Throughout the course of 2023, we’ve witnessed a number of narrative shifts in the way that markets have reacted to the Federal Reserve’s tightening path. Earlier in the year when problems emerged in several high-profile regional US banks, markets widely believed that the Fed would not be able to hike any further, and that the tightening in credit conditions following the bank turmoil could lead to a mild recession.

Then, when the worst fears surrounding regional US banks failed to materialise, stocks rallied on a narrative that the Fed was in all likelihood still done hiking, but there may not be a recession because perhaps the Fed had managed to pull off a soft landing.

Currently, market participants are still positioned as though the US economy has avoided a recession, but now fears are rising that the US economy may be too strong, and that the Fed is bound to keep hiking into that strength. This increases the possibility that the Fed will overtighten, which could have severe adverse effects on the pricing of securities should something break.

The expectation of continued hawkishness from the Fed currently has market participants (particularly those invested in US tech) taking profits from an otherwise good year in expectation of further selling should the Fed follow through with keeping US rates higher for longer.

Mixed Data

Economic data in August has been mixed, which is further adding to the sense of uncertainty. JOLTS job openings came in lower than expected at the beginning of the month. However, this was followed by the ADP employment report that showed an increase in 324k jobs and a year-over-year 6.2% increase in annual pay. This, in-turn, was followed by a disappointing Non-Farm Payrolls report showing that hiring in July had slowed to the lowest levels since January 2021.

Meanwhile, CPI came in unchanged from the previous reading at 2.0% month-over-month, with the yearly reading registering an incremental increase from 3.0% last month to 3.2% in the August release. PPI also showed a slight increase, up to 0.3% from a 0.1% reading on both the core and broader measures last month.

The US consumer also showed further signs of strength, with retail sales confounding analyst expectations of 0.4% for both readings, instead core retail sales came in at 1.0%, while the broader reading came in at 0.7%.

Bears Take The Initiative

For the moment, at least, it appears as though the bears have taken control. Following three consecutive weeks of declines, the Nasdaq 100 is currently 6.5% off its highs and the S&P 500 currently is around 4.5% off its own highs. Before the recent sell-off, both indices had set weekly higher-highs, however, those highs remain lower-highs when compared to their respective November 2021 - January 2022 peaks.

For 2023’s bull trend to remain intact, the bulls will want these indices to come down and set higher-lows while holding one of the major moving averages or, indeed Fibonnacci retracements, as support. This would add conviction to the thesis that further upside is in store, perhaps even a rally to test those former all-time highs. The 23.6% retracement for both indices is currently located just above their respective 20-week moving averages at around 4350 in the case of the S&P 500 and at around 14600 in the case of the Nasdaq.

Of the big tech names that were previously holding up the entire market by virtue of their sheer size and 2023 outperformance, Nvidia has performed best, currently still trading within reach of its all-time highs despite having shed more than 9% of its value in August. Apple is over 10% off its own highs, Microsoft is currently around 12.5% off its July peak, with Meta having given back around 9.7% in August, while currently being more than 20% down from its September 2021 peak. Google finds itself in a similar position to Meta, down only 3.5% in August, however 15% down from its November 2021 highs. All these companies’ shares can be invested in with zero commission at HYCM*.

Can Gold Still Shine Into The Year End?

Recent market uncertainty has also caused gold to sell off. Despite this it remains one of the most traded symbol at HYCM. A certain contingent of investors is still positioning themselves for the scenario that the Fed does actually break something if it continues to pursue its tightening policy as doggedly as it has thus far in 2023. Are gold prices still set to rise into the year end?

Trade with HYCM: https://www.hycm.com

*Zero commission stocks are not available for trading under HYCM (Europe) Ltd and HYCM Capital Markets (UK) Limited. Other fees may apply such as withdrawal fees, dormant account fees, swaps, and spreads.

About: HYCM is the global brand name of HYCM Capital Markets (UK) Limited, HYCM (Europe) Ltd, HYCM Capital Markets (DIFC) Ltd, HYCM Ltd, and HYCM Limited, all individual entities under HYCM Capital Markets Group, a global corporation operating in Asia, Europe, and the Middle East.

High-Risk Investment Warning: Contracts for Difference (‘CFDs’) are complex financial products that are traded on margin. Trading CFDs carries a high degree of risk. It is possible to lose all your capital. These products may not be suitable for everyone, and you should ensure that you understand the risks involved. Seek independent expert advice if necessary and speculate only with funds that you can afford to lose. Please think carefully whether such trading suits you, taking into consideration all the relevant circumstances, as well as your personal resources. We do not recommend clients posting their entire account balance to meet margin requirements. Clients can minimise their level of exposure by requesting a change in leverage limit. For more information, please refer to HYCM’s Risk Disclosure.

Any opinions made in this material are personal to the author and do not reflect the opinion of HYCM. This material is considered a marketing communication and should not be construed as containing investment advice or an investment recommendation, or an offer of or solicitation for any transactions in financial instruments. Past performance is not a guarantee of or prediction of future performance. HYCM does not take into account your personal investment objectives or financial situation. HYCM makes no representation and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast, or other information supplied by an employee of HYCM, a third party, or otherwise.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.