It is amazing what a few years will do to you. Not 2 years ago Ken Heebner of CGM Funds was the most celebrated mutual fund manager since Peter Lynch. [May 28, 2008: Ken Heebner - America's Hottest Investor] His mad dash concentrated style broke the mold in a staid profession. [May 6, 2008: Ken Heebner's Trading for CGM Focus Tripled in 2008] But the Fortune from mid 08 story pretty much tick tocked his performance. The next year was a disaster. [Jul 14, 2009: Bloomberg - Ken Heebner Slumps for 2nd Year] And this year has been no great shakes with a 11% loss YTD. Like I said in many pieces in 2008 and 2009 I don't think he got dumb overnight - his long term record still is remarkable - [Dec 31, 2009: WSJ - Best Stock Mutual Fund of the Decade] but in many interviews on CNBC I have been struck on how bullish Heebner has been (and continues to be) on the general economy. Most mutual funds do not short, but his charter allows him to - but it was rarely employed; a big error considering what happened in 08 and early 09.

I have not looked at the portfolio lately but I was in a bit of shock when I looked this morning; I've seen Heebner concentrated before but never like this. Ford (F) is 15% of the portfolio; the top 4 positions are nearly 40% of the portfolio. I can definitely see the reasons for Ford and Goldman Sachs but if he employed technical analysis many of these names would be nowhere near the top of his portfolio - but this is definitely a 'fallen angel' + 'commodity' playbook. Ex the one company every human on earth must own - Apple (AAPL) of course. I still admire the conviction to have a concentrated portfolio - I've long said anyone who holds 350 stocks (which is almost all funds!)... unless relatively concentrated in the top 10-20, is basically buying the market with a bit of a spin on it. But the trick to being concentrated is of course being in the right spots.

These are, of course, Q1 holdings as of March 31st and with his style the portfolio could have a different complexion by now; we won't know until mid August.

Via BusinessWeek:

Market News and Data brought to you by Benzinga APIs

I have not looked at the portfolio lately but I was in a bit of shock when I looked this morning; I've seen Heebner concentrated before but never like this. Ford (F) is 15% of the portfolio; the top 4 positions are nearly 40% of the portfolio. I can definitely see the reasons for Ford and Goldman Sachs but if he employed technical analysis many of these names would be nowhere near the top of his portfolio - but this is definitely a 'fallen angel' + 'commodity' playbook. Ex the one company every human on earth must own - Apple (AAPL) of course. I still admire the conviction to have a concentrated portfolio - I've long said anyone who holds 350 stocks (which is almost all funds!)... unless relatively concentrated in the top 10-20, is basically buying the market with a bit of a spin on it. But the trick to being concentrated is of course being in the right spots.

Top 10 holdings

| Security | Net Assets | |

| Ford Motor Company (F) | 15.12% | |

| Goldman Sachs Group, Inc. (GS) | 8.09% | |

| Freeport-McMoRan Copper & Gold B (FCX) | 7.97% | |

| Teck Resources Ltd Subordinate Voting Share (TCK) | 7.59% | |

| FedEx Corporation (FDX) | 6.23% | |

| Cliffs Natural Resources Inc. (CLF) | 6.04% | |

| Delta Air Lines, Inc. (DAL) | 5.89% | |

| Apple, Inc. (AAPL) | 5.46% | |

| Alpha Natural Resources Inc (New) (ANR) | 5.24% | |

| Morgan Stanley (MS) | 5.20% |

These are, of course, Q1 holdings as of March 31st and with his style the portfolio could have a different complexion by now; we won't know until mid August.

Via BusinessWeek:

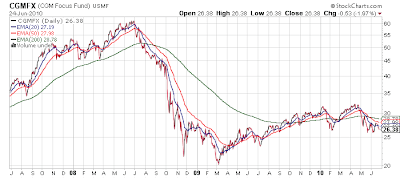

- Ken Heebner started the century making all the right moves for his CGM Focus (CGMFX) mutual fund. Deftly shifting into and out of sectors such as homebuilding and commodities, he posted returns averaging 32 percent annually from 2000 through 2007, a period when the Standard & Poor's 500-stock index returned just 1.7 percent a year.

- Then the magic stopped. CGM Focus, which Heebner runs from Boston, is the only domestic stock fund to trail at least 96 percent of its peers in 2008, 2009, and again this year, according to research firm Morningstar. The main culprits: bad bets on commodity and financial stocks. "He's been in all the wrong sectors at all the wrong times," says Jonathan Rahbar, a Morningstar analyst.

- Even with the losses, Heebner is holding his spot atop the 10-year chart. CGM Focus returned an average of 17 percent a year in the decade ended May 31, the best record of more than 3,200 U.S. diversified mutual funds. In second place was Lord Abbett Micro Cap Value, which gained 14 percent.

- Heebner, 69, the co-founder of Capital Growth Management, launched CGM Focus in 1997; it has returned 13 percent a year since then. He also manages CGM Mutual (LOMMX), which has returned 4 percent a year for the past decade, and CGM Realty (CGMRX), which gained 19 percent annually over the same stretch. He declined to be interviewed for this story.

- Heebner's nosedive rivals that of Bill Miller, the high-profile Legg Mason fund manager who beat the S&P 500 for a record 15 consecutive years, then dropped to the back of the pack from 2006 through 2008. Like Miller, Heebner has lost investors, with net withdrawals of $1.8 billion since August 2008, according to Morningstar. CGM Focus' assets are now $3 billion, down from a peak of $10.3 billion in June 2008, reflecting market losses and investor withdrawals.

- Unlike Miller, he lagged the market last year, gaining 10 percent while U.S. stock funds on average rose 33 percent. Miller's Value Trust was up 41 percent. Steven Rogé, who invests his clients' money in mutual funds, says the ballooning of Heebner's assets in 2008 convinced him there were better places to invest. "When a fund attracts assets that quickly, we worry about a manager's ability to handle it," says Rogé, whose firm, R.W. Rogé, oversees $200 million.

- Heebner is known for building big stakes in specific industries and for shifting gears quickly. CGM Focus' top 10 holdings represented 73 percent of assets of as Mar. 31, vs. 31 percent for the typical fund, according to Morningstar.

- The fund's turnover ratio, a measure of how much the portfolio changes in a year, is 464 percent, more than four times greater than peers. Heebner also bets on falling stock prices by selling short, a strategy that many funds don't pursue.

- In 2000 and 2001, Heebner profited by betting against technology stocks. At the same time he began buying shares of homebuilders, such as Lennar (LEN), before the boom in construction and home prices. By the start of 2005, before homebuilding stocks began their decline, he had sold them and moved into energy and commodity companies. The price of oil more than tripled between the end of 2004 and the middle of 2008. "Historically he has done phenomenally well knowing when to rotate," says Rahbar. (this was one great trend trade after another - nailed)

- More recently his moves have been ill-timed. Returns faltered in the second half of 2008, when Heebner's holdings in energy, metals, and agriculture stocks began to tumble. After selling the commodity stocks he bought financials. CGM Focus dropped 48 percent for the year (2008), compared with a decline of 37 percent by the S&P 500.

- Heebner sold his insurance holdings at a loss in the first quarter of 2009. That hurt: Many of those stocks soared after the market reached a 12-year low in March. Heebner is getting back into commodities and sticking with financial stocks. Metal and mining stocks accounted for 36 percent of his holdings as of Mar. 31. (of course these stocks have been hammered in May on European issues and fears of new global slowdown) Bank stocks represented 16 percent of the portfolio. (hammered on finreg) So far the strategy isn't paying off.

- The declines since 2008 "don't indicate Heebner has lost his talent or his expertise," says Ronald Sugameli, manager of the $130 million New Century Alternative Strategies Portfolio (NCHPX), a mutual fund that invests in other mutual funds. CGM Focus represented about 1.5 percent of Sugameli's fund as of May 31. While he expects Heebner's performance to bounce back, the fund manager isn't planning to boost his holdings of CGM Focus. Given the fund's volatility, Sugameli says, "it is best used in small doses."

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In: Air Freight & LogisticsAirlinesAutomobile ManufacturersCoal & Consumable FuelsComputer HardwareConsumer DiscretionaryDiversified Metals & MiningEnergyFinancialsIndustrialsInformation TechnologyInvestment Banking & BrokerageMaterialsSteel

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in