With last week’s Hamas terrorist attack and the swift response by the Israeli government, war has once again taken over the global conversation. While the financial costs of war pale in comparison to the human costs, many investors are rightly worried about their portfolios.

To this end, I will explore how to invest during times of war both as an observer (i.e. someone who is not directly impacted by the conflict) and as a participant (i.e. someone living in a war zone). This article is not meant to minimize the tragic impact of global violence, but to provide a better understanding of how to preserve wealth during geopolitical instability.

Investing During Times Of War (As An Observer)

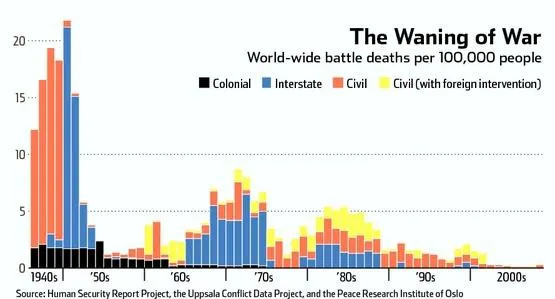

In 2011, Steven Pinker published an article in the Wall Street Journal titled Why Violence is Vanishing which demonstrated that global deaths attributable to war and large scale conflicts had been declining on a per-capita basis since the end of WWII:

Though other analyses have found that the number of interstate conflicts have actually increased since WWII, these conflicts have been less deadly than the World Wars that preceded them.

Due to this general decline in global violence, most people who invest during times of war in the future will probably be investing as observers not participants of war. Even in the United States, which has been involved in numerous conflicts since the early 1900s, the vast majority of its populous have been observers of war as well.

Given this, it is also likely that you will be investing as an observer of war too. As an observer, you don’t need to worry about the impact of war on your community or your immediate safety, but you do need to worry about how to preserve your wealth during a period of instability. So, let’s take a look at how some of the major asset classes perform during war time.

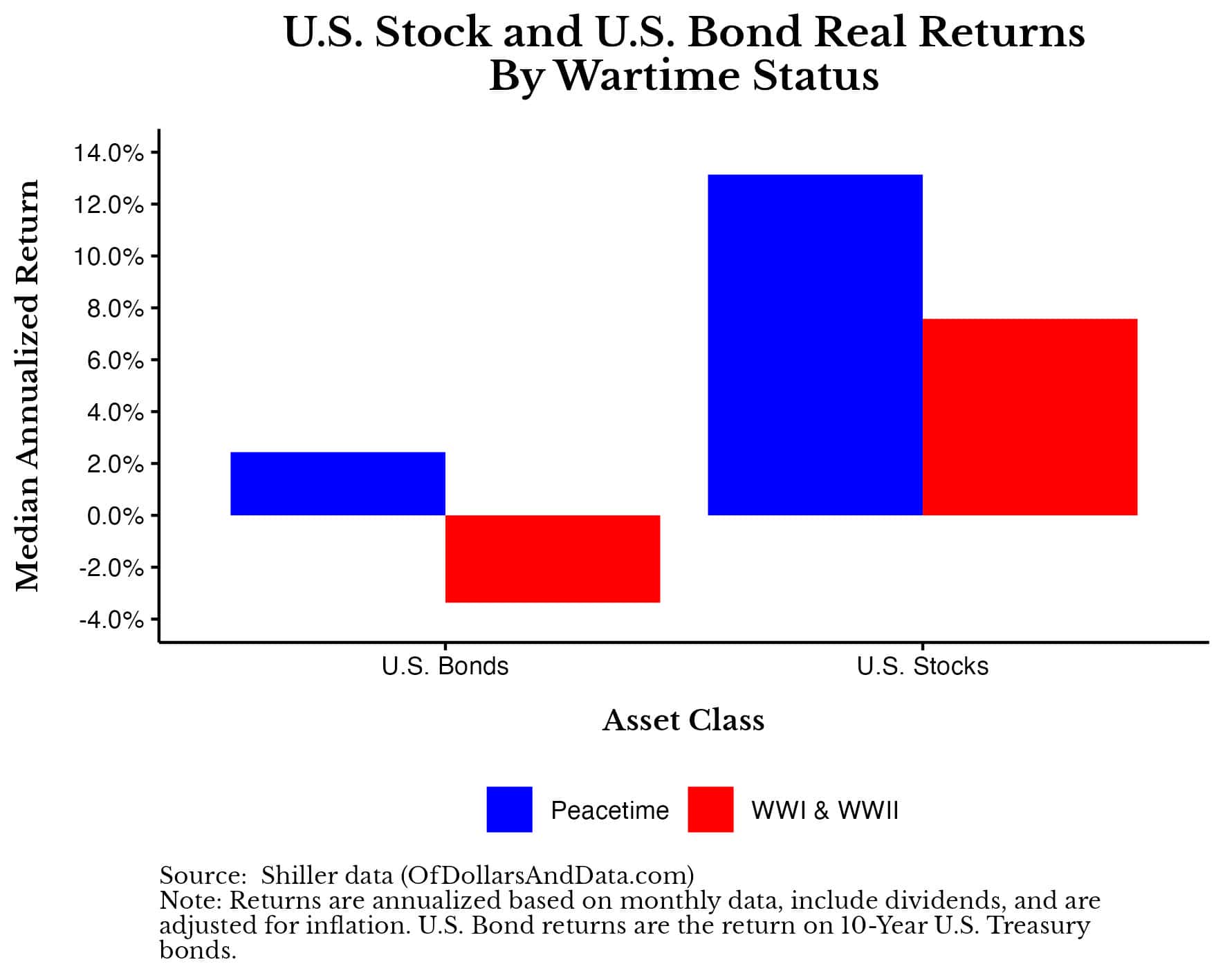

If we were to compare the median annualized return on U.S. stocks and U.S. bonds (10-Year Treasuries) during peacetime and wartime since 1900, we would see that both tend to underperform during periods of global war (e.g. WWI & WWII):

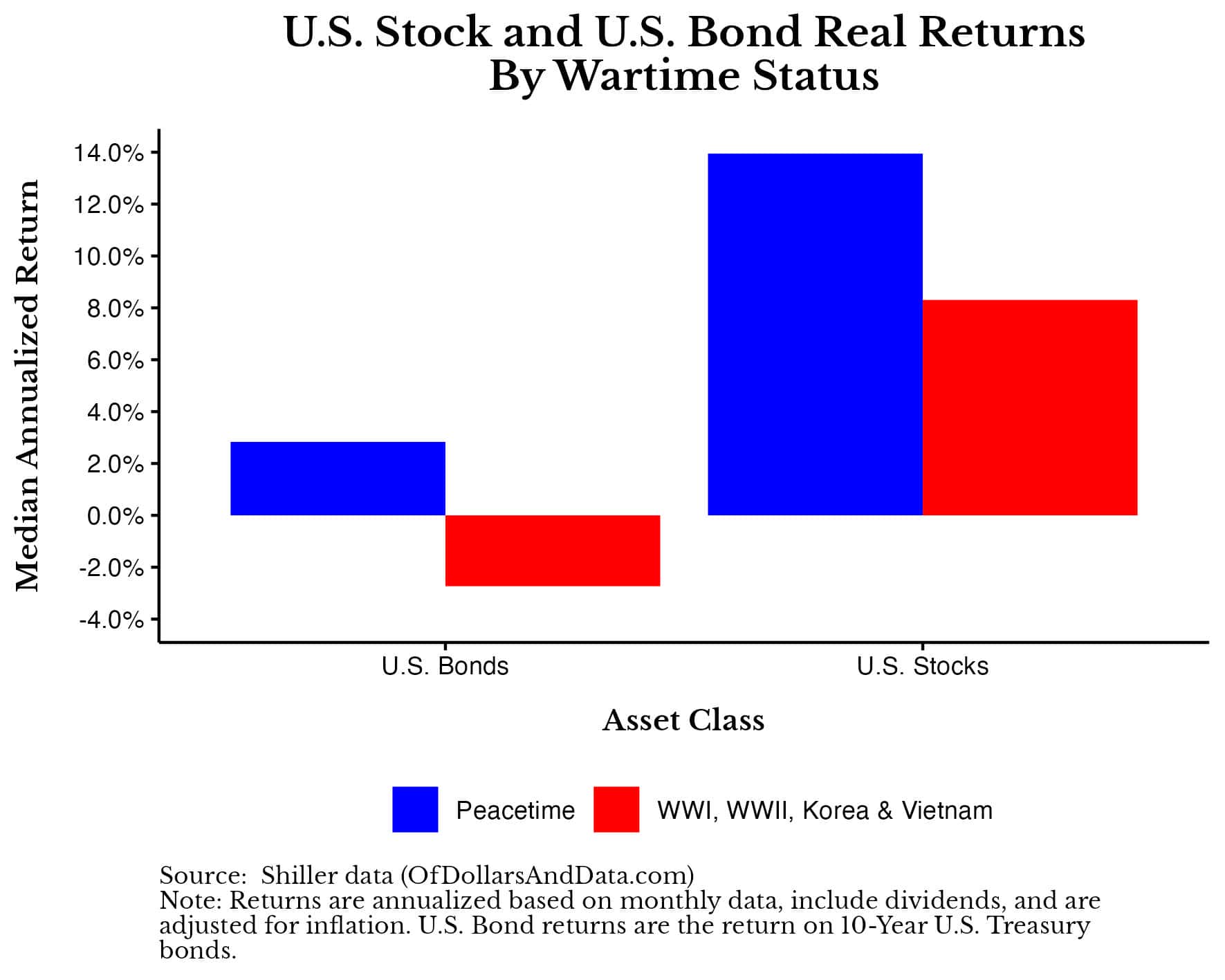

Even if we were to include the next two largest U.S. conflicts (the Korean War and the Vietnam War), we would still see underperformance by U.S. stocks and U.S. bonds during wartime:

In particular, both U.S. stocks and U.S. bonds had a median annualized real return that was ~5% lower during wartime than during peacetime. More importantly, the difference in the average return between wartime and peacetime was statistically significant for U.S. bonds at the 1% level, but not for U.S. stocks.

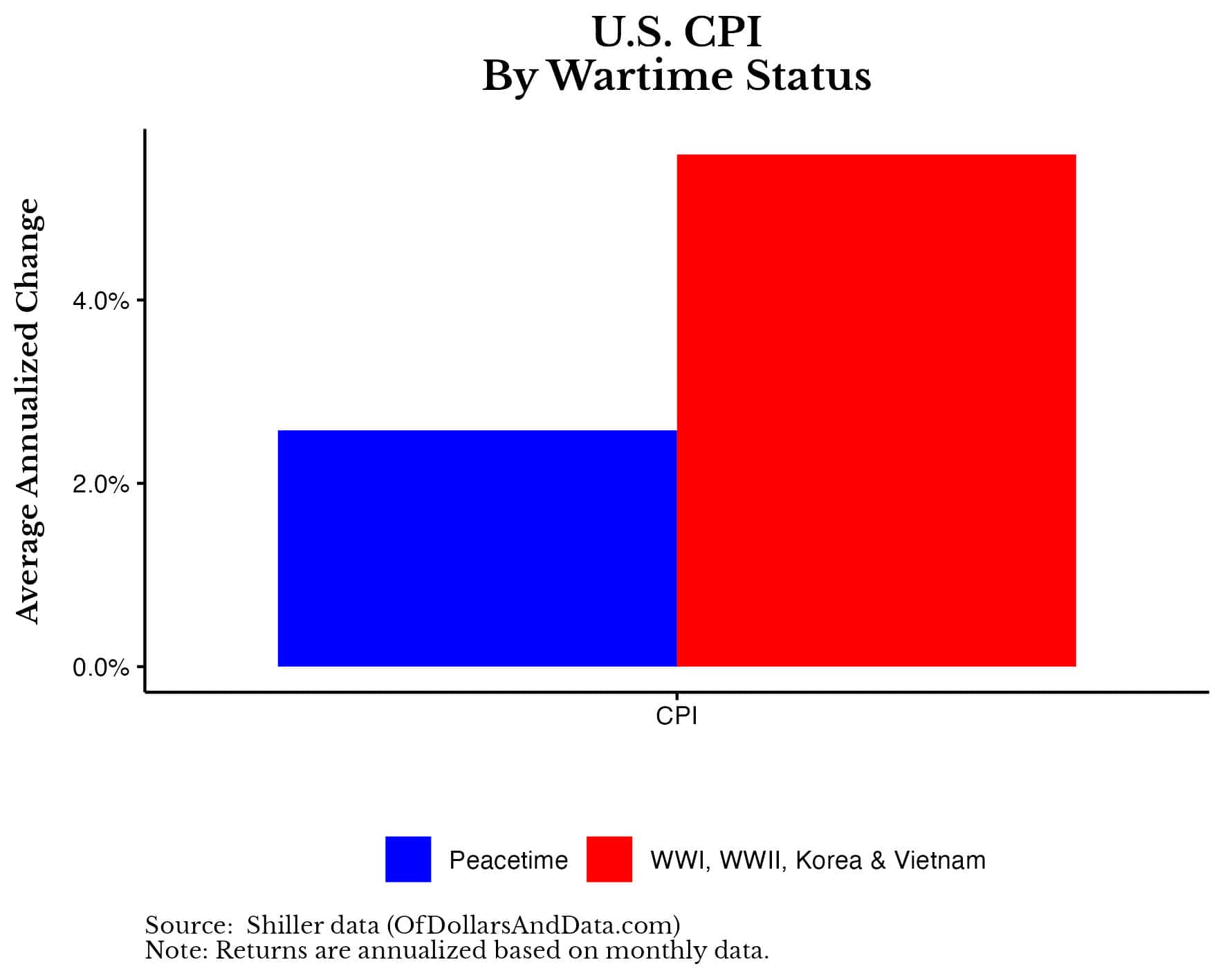

What is the cause of this wartime underperformance? Mostly higher inflation.

As you can see in the chart below, inflation (CPI) tends to run about 3% higher (on average) during wartime than during peacetime [Note: This difference is statistically significant at the 1% level]:

Given this information, if the U.S. were to enter into another war in the near future, it seems likely that inflation would ramp back up due to increased government spending.

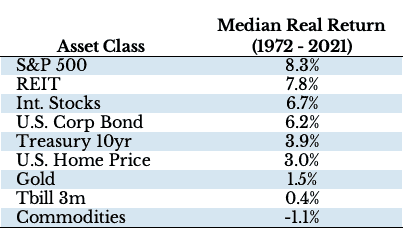

Therefore, we can infer that investing during wartime is mostly an exercise in investing during periods of high inflation. And the best assets to own during periods of high inflation are overwhelming stocks and real estate:

From this table you can see that U.S. stocks (“S&P 500”), real estate investment trusts (“REIT”), and international stocks are the best asset classes to own regardless of what is going on with inflation.

You could even argue that U.S. corporate bonds are a great asset class to consider owning today given their higher yields and lower risk profile compared to stocks and REITs. This is the exact argument that Howard Marks made last week in his follow up to his Sea Change memo (emphasis his):

In early 2022, high yield bonds (for example) yielded in the 4% range – not a very useful return. Today, they yield more than 8%, meaning these bonds have the potential to make a great contribution to portfolio results. The same is generally true across the entire spectrum of non-investment grade credit…Unless there are serious holes in my logic, I believe significant reallocation of capital toward credit is warranted.

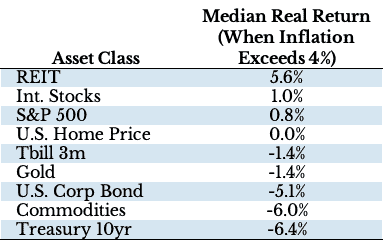

I don’t disagree with Marks’ logic, however, if war comes and inflation is higher than expected, than all fixed income instruments (including high yield bonds) will get crushed. You can see this clearly if you were to examine the real median calendar year returns of all asset classes (from 1972-2021) when inflation exceeds 4%:

No longer does fixed income look particularly attractive (even with today’s higher yields) in a high inflation environment. This doesn’t mean you shouldn’t own fixed income today, only that high inflation is an ongoing risk, especially for those bonds with longer maturities.

After reviewing the data on asset class returns, the evidence suggests that you should own equities, real estate, and short-duration fixed income instruments if you want to preserve your wealth during periods of international conflict.

But don’t just take my word for it. Barton Biggs, the author of Wealth, War, & Wisdom, concluded his wonderful book on the same topic with:

In my considered but not necessarily correct opinion, a family or individual should have 75% of its wealth in equity investments. A century of history validates equity as the principal, but not the only, place to be.

Unfortunately, if you came to this article wondering what kinds of equities to own during wartime, than you will need to go elsewhere. Not only is the data on this difficult to find historically, but shifting your equity portfolio in and out of defensive or energy stocks based on news headlines is not something I would recommend. Following such a strategy is akin to stock picking and marketing timing, both topics I’ve opined on previously (here and here).

To sum it up, investing during times of war as an observer boils down to managing risks—particularly, inflation risk. Stocks, real estate, and short duration bonds are a great place to invest to counteract this, however, you will also need to remain disciplined to stay the course during this difficult time.

Now that we’ve looked at investing during times of war as an observer, let’s tackle the more difficult task of investing during wartime as a participant.

Investing During Times Of War (As A Participant)

If you find yourself living in a country that is undergoing an active war, realize that wealth preservation will be low on your priority list. Finding food, clean drinking water, and keeping you and your loved ones safe will outweigh everything else.

With that being said, the best ways to hedge against the risk of war in your locality come down to asset portability and geographic diversity. Let’s look at each of these in turn:

- Asset Portability: When it comes to preserving wealth during times of conflict, your best bet is to own assets that are portable. You want to be able to take your wealth with you, wherever you go. As important as stocks and real estate are to building wealth during wartime, they won’t be able to help you much if you can’t access them. Stock exchange shutdowns and land confiscation are both common occurrences during wartime that could evaporate your wealth in a hurry. Therefore, if you want to make your wealth more portable, consider the following:

-

- Precious metals: Owning gold, silver, and other kinds of precious metals as bullion or coins are an easy way to make your wealth portable in the event you need to flee quickly.

- Fine jewelry/diamonds: In addition to metals, jewelry and diamonds can make for a great portable wealth preserver as these items tend to be smaller and more discreet than larger bullion.

- Cryptocurrency in a cold wallet: Knowing the seed phrase to a cryptocurrency wallet that you control is arguably the most portable wealth ever invented. Unlike any other portable asset mentioned thus far, you can have access to a technically unlimited amount of cryptocurrency wallet just by memorizing a set of words. And, unless someone knows your seed phrase, no one can take this wealth from you.

- Downsides: Unfortunately, the risk of having portable wealth is that it is very easy for someone else to take it from you even if you aren’t in a war. Jewelry and previous metals are both easy targets for theft as is cryptocurrency if you aren’t careful about your seed phrase. In addition, moving lots of wealth across international borders without going through the proper procedures is illegal in many circumstances. While preserving wealth is important, keeping yourself out of prison is even more so.

- Other considerations: The last, and arguably the most portable asset you should consider investing in is—yourself. Unlike all of the assets mentioned above, no one has the ability to take your knowledge away from you. While the knowledge you have won’t be as valuable in every location and under every circumstance, it’s better to have it than not have it. As Barton Biggs concluded in Wealth, War, and Wisdom, “Perhaps brains or a skill are the most portable and best wealth preserver.”

-

- Geographic Diversity: If you can’t make your assets more portable, another option is to spread them out geographically before the onset of a crisis. A few options for doing this include:

-

- Owning a safe haven/farm: Having a location that you can hide out in for a period of months (or even years) during wartime could be the difference between life and death. Whether that means having a country home or a remote farm that has access to food, owning a safe haven away from the areas of primary conflict can be of great use.

- The downside to owning a safe haven is that they are very easy to confiscate once discovered. Many individuals learned this the hard way during WWII as the Nazis looted their way across Europe.

- Having a foreign bank account: If you don’t want to invest in a safe haven, another option is to have some money in a foreign bank account that you can easily access after you escape your home country. Unfortunately, opening a foreign bank account is easier said than done. Many countries have strict regulatory requirements that you will need to meet to open a bank account. In addition, if you open a foreign bank account in a country with an unstable banking system, there is no guarantee that your money will be safe there.

- Owning a safe haven/farm: Having a location that you can hide out in for a period of months (or even years) during wartime could be the difference between life and death. Whether that means having a country home or a remote farm that has access to food, owning a safe haven away from the areas of primary conflict can be of great use.

- Downsides: While owning assets that are geographically diverse can help with wealth preservation, the difficulty in following this strategy is being able to escape your home country in the first place. While geographic asset diversity is a sign of planning ahead, making sure you have an escape plan in the event of a war is equally important.

- Other considerations: How much of your assets should you consider investing into a safe haven or foreign bank account? Barton Biggs suggested 5%-10%. My recommendation is directionally similar—enough to start over. Fleeing your home country due to war is a traumatizing event regardless of what happens to your wealth. Surviving such an ordeal and having the ability to start anew, even if it means losing 90% of what you’ve saved, is still a gift in and of itself. Don’t worry about what you lost, focus on what you saved.

-

Regardless of what strategy you choose to follow during times of conflict, realize that none of the proposals mentioned above are foolproof. As Barton Biggs ultimately concluded about wealth preservation during wartime:

There are no easy solutions or conclusions as to the best way to preserve or enhance wealth. If you have your wealth in a country that is conquered, occupied, or suffers an ecological or technological disaster, you are going to suffer immense losses unless you have escaped to a safe haven well in advance of the hostilities.

Preparing for the financial impact of war is fraught with uncertainty. The strategies mentioned above, from asset portability to geographic diversity, are about minimizing these uncertainties rather than eliminating them. Understand that during a war, the situation evolves rapidly and what works today may not work tomorrow. In the end, while we can’t predict what will happen during wartime, we can strive to be as prepared as possible if it ever arrives.

The Bottom Line

War is unpredictable and devastating, making wealth preservation during such times a secondary concern at best. However, if you’re looking for ways to safeguard your financial future in the face of conflict, remember—asset portability and geographic diversity are key. You want to move a portion of your assets before conflict erupts or be able to move them if it ever does.

For those not directly facing conflict, you should focus your investments on those assets that do well during periods of higher inflation since inflation tends to be higher during wartime. Historically this meant investing in global equities, real estate, and short-term bonds, however, the future may not necessarily be like the past.

While no one can guarantee the safety of your wealth during wartime, the principles above can help guide you in making hard choices during extremely difficult circumstances. Let us just hope that you never have to use them.

Lastly, my heart goes out to the millions of innocent civilians that have been impacted by the recent conflict in Israel. Thank you for reading.

If you liked this post, consider signing up for my newsletter or checking out my prior work in e-book form.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.