Stocks rallied last week, with the S&P 500 climbing 1.3% to close at 4,415.24. The index is now up 15% year to date, up 23.4% from its October 12, 2022 closing low of 3,577.03, and down 7.9% from its January 3, 2022 record closing high of 4,796.56.

While the overall data indicate continued economic growth, there are signs of stress developing that bear watching.

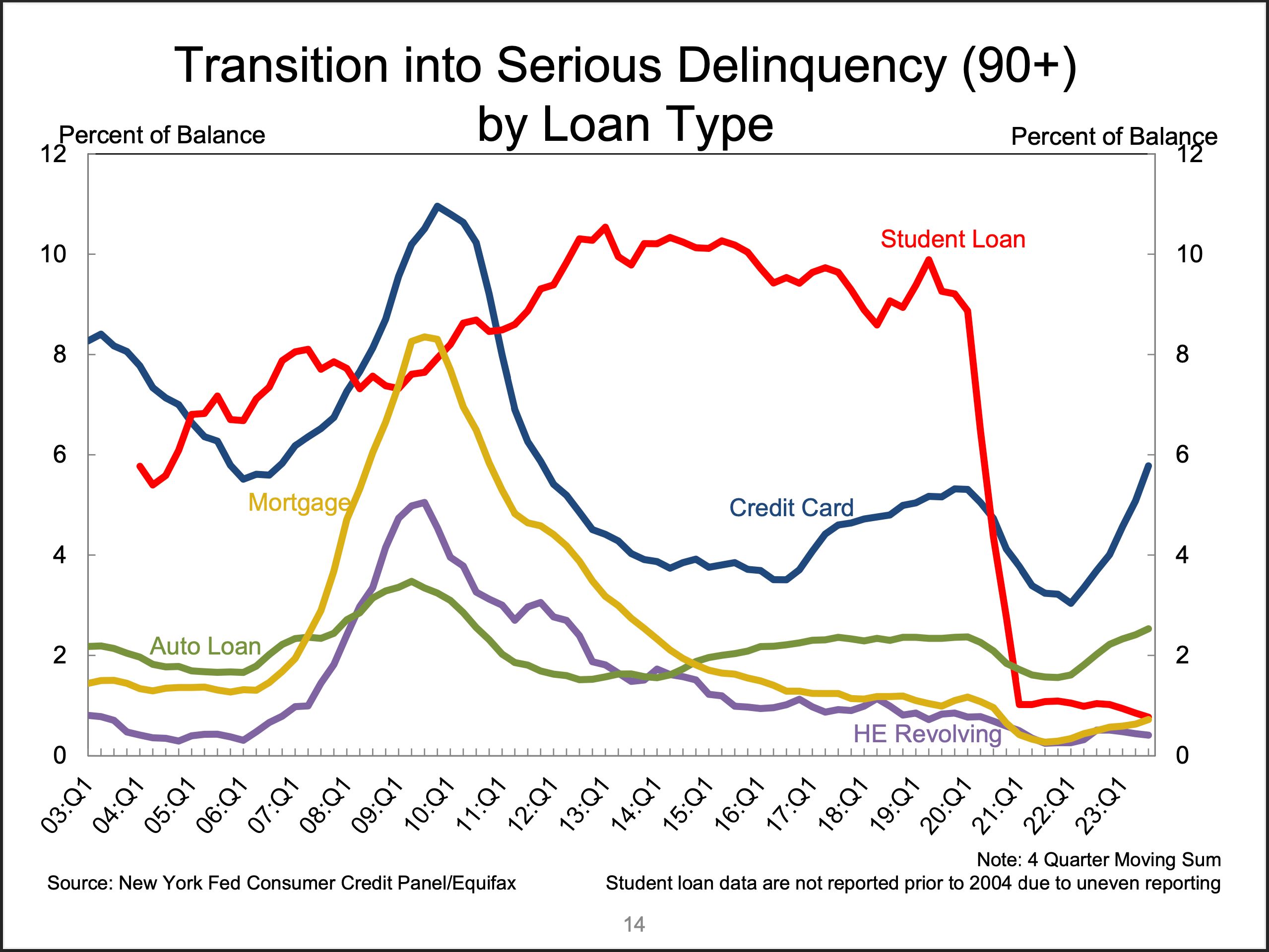

According to the New York Fed’s Q3 Household Debt and Credit (HHDC) report, the share of debt newly transitioning into delinquency continues to rise for mortgages, auto loans, and credit cards.

The share of debt newly transitioning into delinquency is rising. (Source: NY Fed)

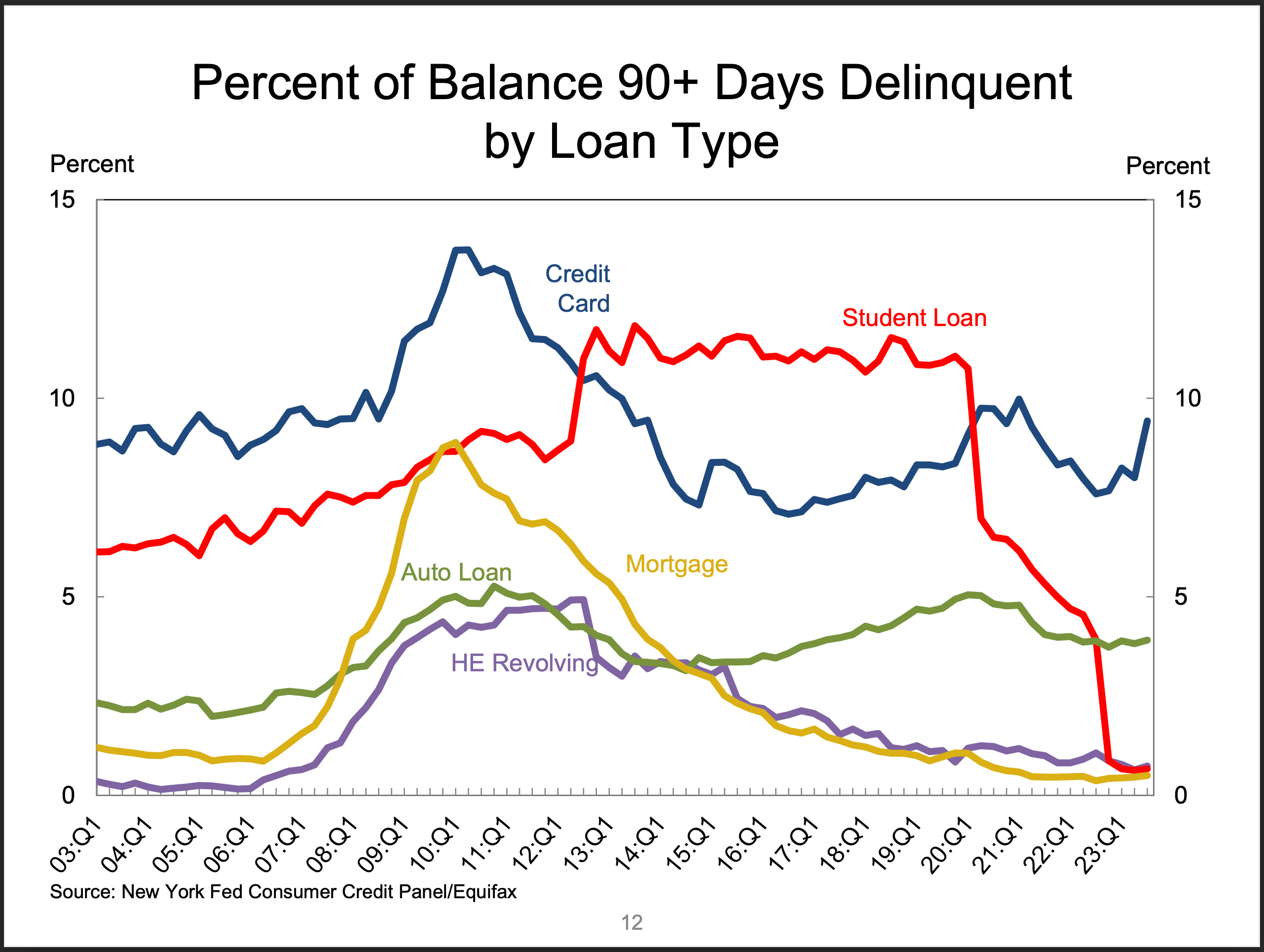

When you include the debt, the delinquency rates, while rising, continue to reflect a normalization back to prepandemic levels.

Aggregate delinquency rates are rising but remain below prepandemic levels.(Source: NY Fed)

In other words, while the “flow” into new delinquency has been picking up, the “stock” of delinquencies remains below prepandemic levels.

“As of September, 3.0% of outstanding debt was in some stage of delinquency, up by 0.4 percentage points from the second quarter yet 1.7 percentage points lower than the fourth quarter of 2019,” New York Fed researchers wrote.

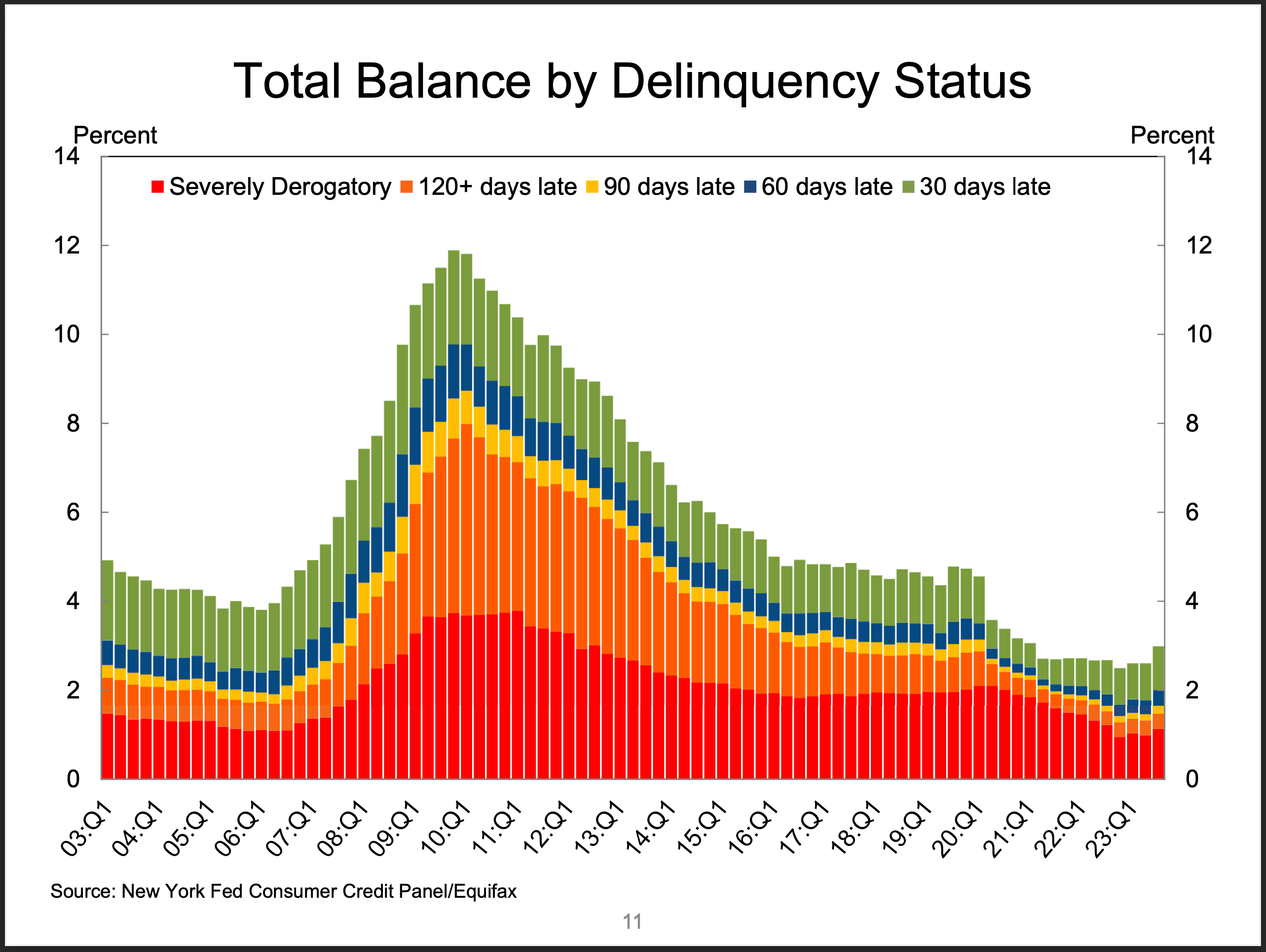

The total balance of debt in delinquency is rising but remains low by historical standards. (Source: NY Fed)

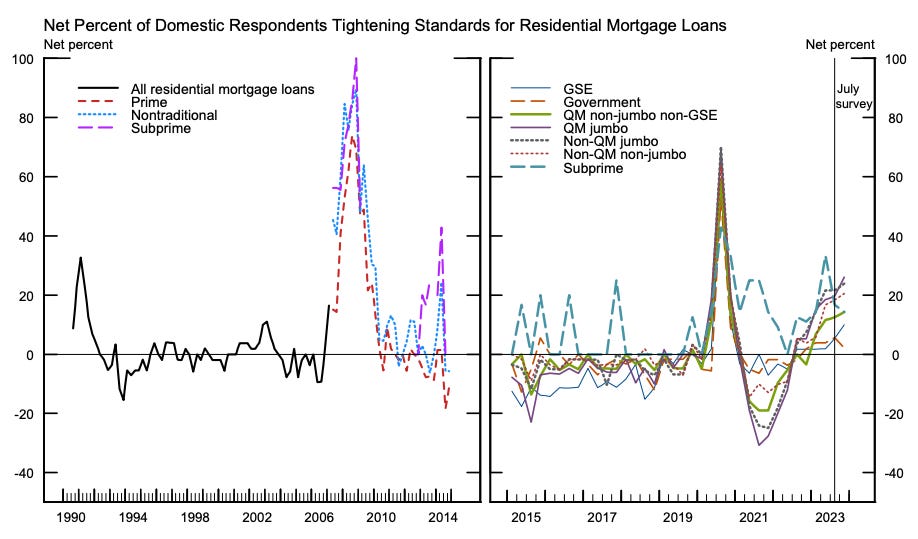

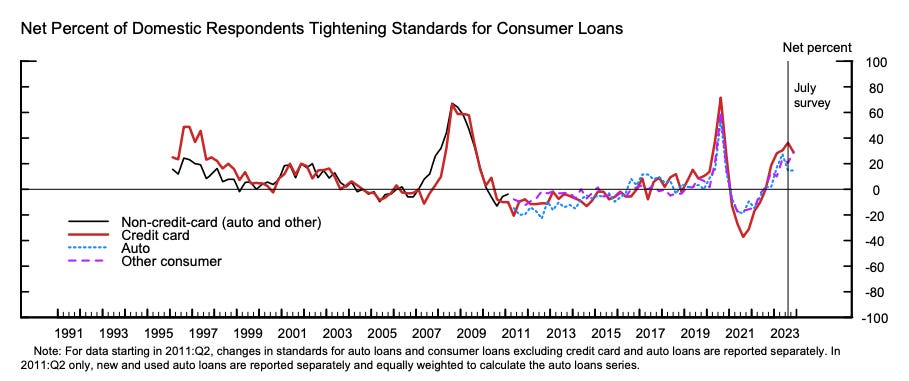

The rise in delinquencies comes as banks have been tightening lending standards.

According to the Federal Reserve’s October Senior Loan Officer Opinion Survey on Bank Lending Practices, lending standards have tightened for residential real estate loans…

Lending standards for residential real estate loans have tightened. (Source: Federal Reserve)

… and for consumer loans.

Lending standards for consumer loans have tightened. (Source: Federal Reserve)

Consistent With Softening, But Not Particularly Bad

There’s not much to celebrate here, especially if you are a consumer that’s affected or you are someone hoping for hotter economic growth.

These deteriorating metrics, however, do appear in line with the Federal Reserve’s ongoing efforts to bring down inflation by reining the economy by tightening monetary policy. Indeed, key labor market metrics have been cooling for over a year. Read more on the evolving labor market here, here, here, and here.

Upgrade to paid

That said, it’s also arguably premature to conclude that the decelerating economy is destined to transition into one that’s in an outright recession.

“Overall this looks consistent with a softening trajectory for consumer spending, but not a particularly bad one,” JPMorgan’s Daniel Silver wrote in response to the HHDC report.

Make no mistake: Consumer finances continue to be in remarkably good shape.

“We have emphasized that household balance sheets look very strong after a long streak of deleveraging following the Global Financial Crisis, and this could reduce the need for most households to tighten their belts,” Oxford Economics’ Daniel von Ahlen wrote on Friday. “The surge in equity and home prices since the pandemic mean that household net worth is at record highs.”

“Household balance sheets look very strong.” (Source: Oxford Economics)

For more on the strength of consumer finances, read this, this, this, and this.

Keep in mind that the deteriorating credit metrics discussed above occurred during a period of robust GDP growth, supported by resilient consumer spending growth. And the economy continues to be supported by many other tailwinds pointing to more growth ahead.

The Restart Of Student Loan Payments Have Had Limited Impact

So far, the resumption of student loan payments has had a limited effect on the consumer picture.

“We should also keep in mind that the 3Q [HHDC] report is probably too early to see potential negative effects of the end of forbearance on student loans, although the early read from some related data is that this likely will not end up being a huge drag on consumers,” JPM’s Silver said.

Upgrade to paid

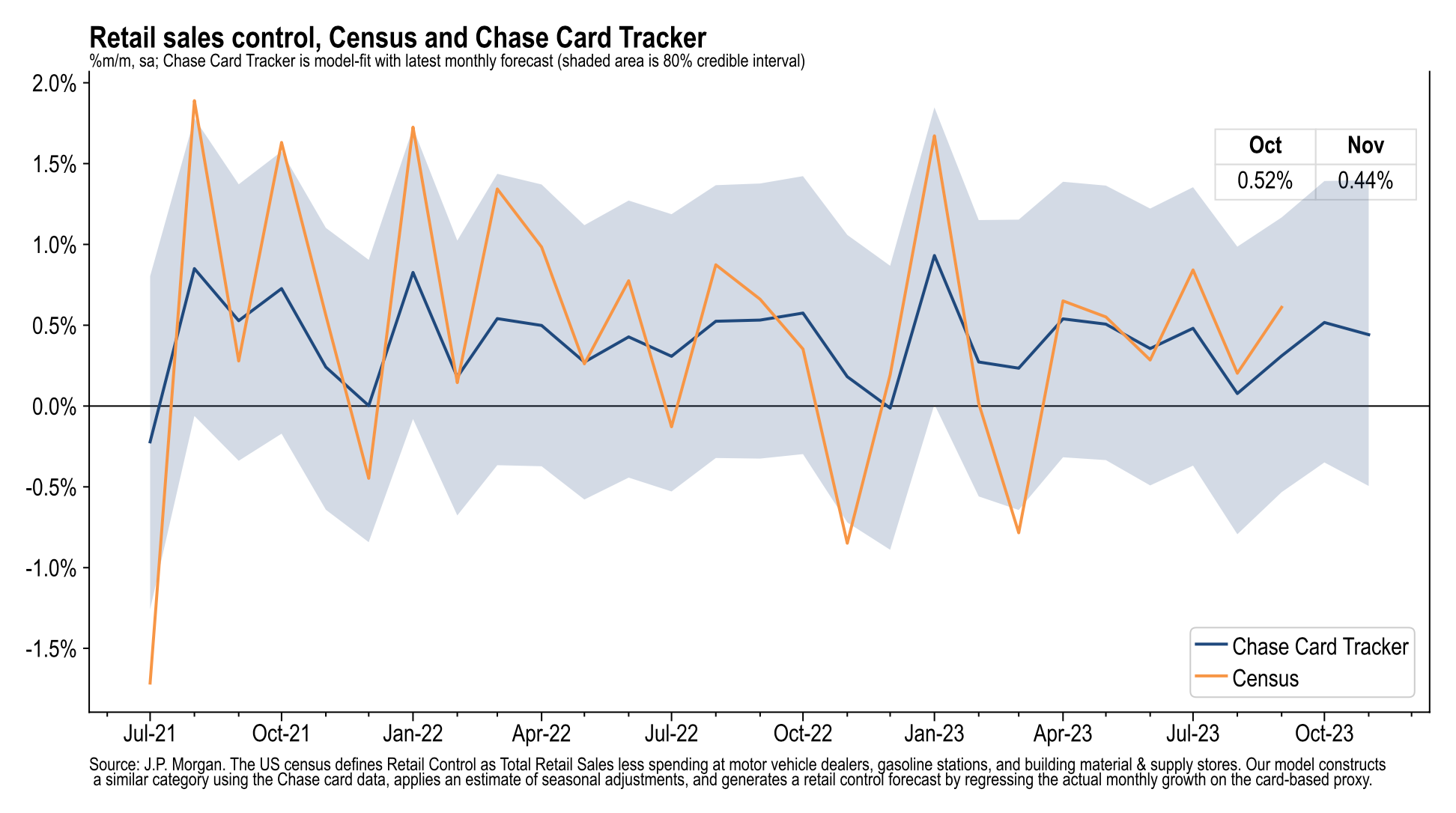

According to JPMorgan’s analysis, Chase Consumer Card spending data as of November 1 suggests the U.S. Census’ control measure of retail sales — which is used in calculating GDP growth — was up 0.52% month-over-month in October.

Card data suggests spending held up in October. (Source: JPMorgan)

Citing their own proprietary data, Bank of America analysts found card spending declined by 0.2% in October.

“With the end of the student loan moratorium, many are wondering if consumers will cut back on spending to make loan repayments,” Bank of America analysts wrote. “When we look at the spending of households who made a [student loan] payment for the first time in 2023 in October, we do not see any obvious sign of an adverse impact relative to other groups of households.“

Consumers who restarted student loan payments in October aren’t exactly getting slammed. (Source: BofA)

Be Vigilant

Just because the stock market usually goes up and the economy is usually growing doesn’t mean they are always doing so.

Bear markets and recessions are unfortunate hurdles on the long-run path to building wealth in risk assets.

To reiterate, the overall data indicate continued economic growth — and consequently suggest a bullish “Goldilocks” soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

But as the data continues to come in, we’ll have to be vigilant as we watch for signs that the economic narratives may be shifting.

A version of this post was originally published on Tker.co.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.