By Lance Roberts

It’s that time of the year where Wall Street polishes up their crystal balls and pin targets on the S&P index for the upcoming year. As is often the case, while Wall Street is always optimistic, the forecasts prove pretty wrong.

For example, on December 7th, 2021, we wrote an article about the predictions for 2022.

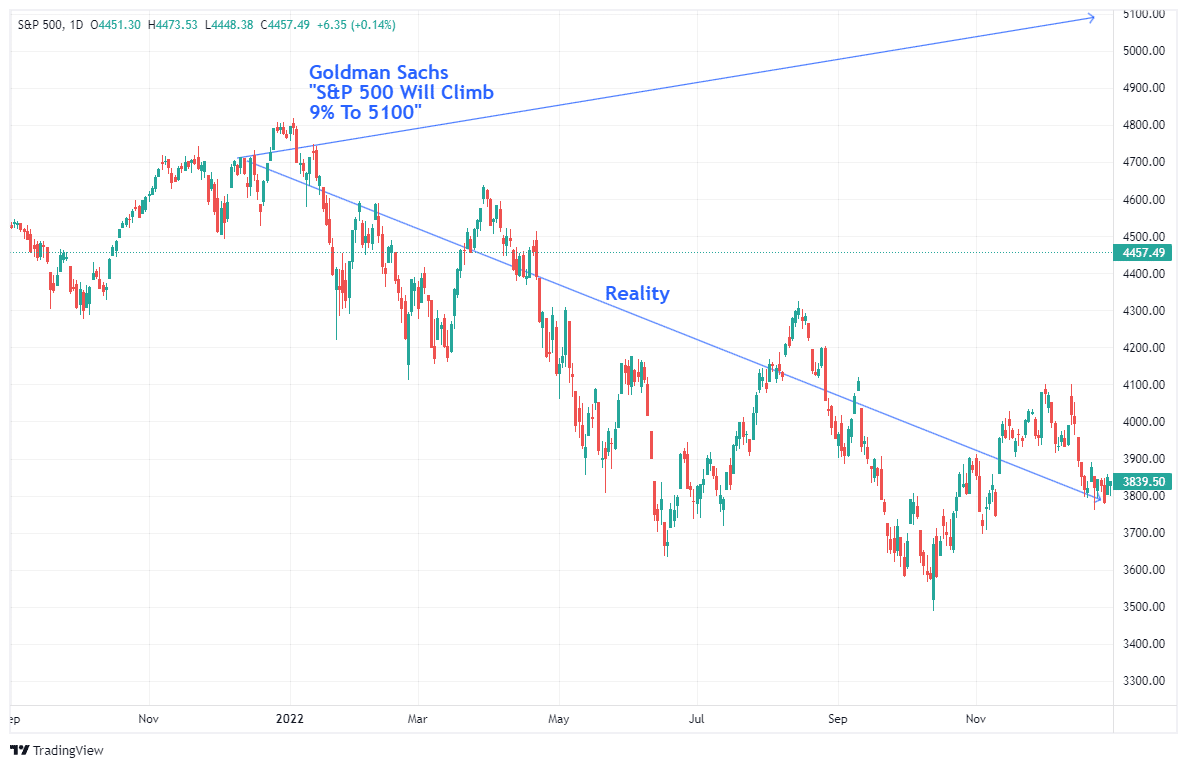

“There is one thing about Goldman Sachs that is always consistent; they are ‘bullish.’ Of course, given that the market is positive more often than negative, it ‘pays’ to be bullish when your company sells products to hungry investors.

It is important to remember that Goldman Sachs was wrong when it was most important, particularly in 2000 and 2008.

However, in keeping with its traditional bullishness, Goldman’s chief equity strategist David Kostin forecasted the S&P 500 will climb by 9% to 5100 at year-end 2022. As he notes, such will “reflect a prospective total return of 10% including dividends.”

The problem, of course, is that the S&P 500 did NOT end the year at 5100.

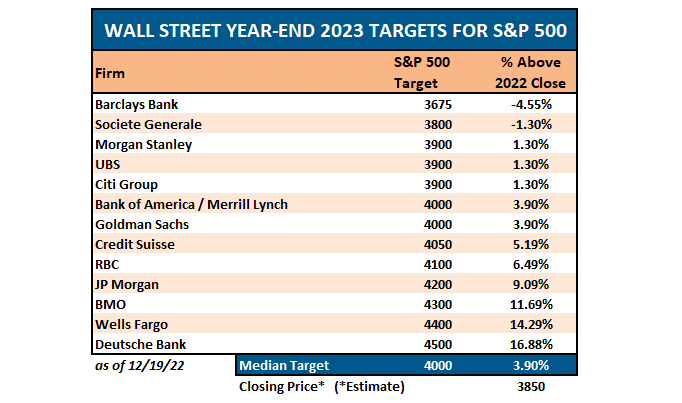

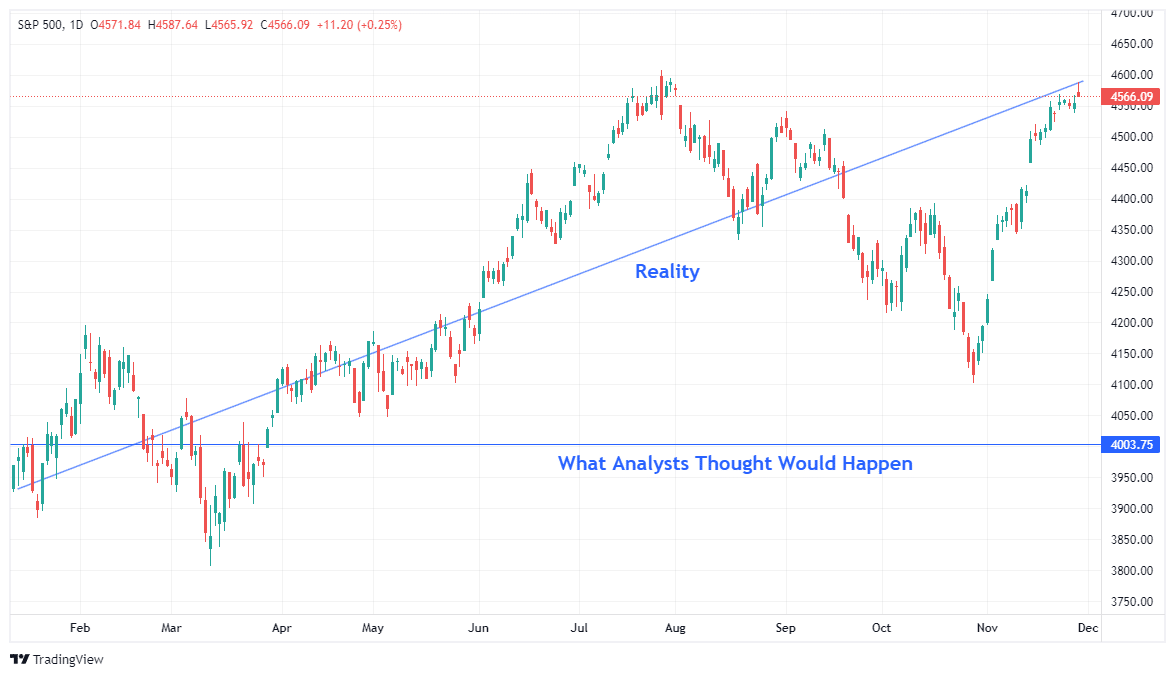

Then, in 2022, Wall Street analysts suggested that 2023 would be a year of meager return of just 3.9% with a median price target of 4000.

Of course, reality turned out to be markedly different.

However, the guessing game is an annual tradition of Wall Street analysts and, as is always the case, to borrow a quote:

“(Market) Predictions Are Difficult…Especially When They Are About The Future” – Niels Bohr

Okay, I took a little poetic license, but the point is that while we try, predictions of the future are difficult at best and impossible at worst. If we could accurately predict the future, fortune tellers would win all the lotteries, psychics would be richer than Elon Musk, and portfolio managers would always beat the index.

However, all we can do is analyze what occurred previously, weed through the noise of the present, and discern the possible outcomes of the future. The biggest problem with Wall Street, both today and in the past, is the consistent disregard of the unexpected and random events they inevitability occur.

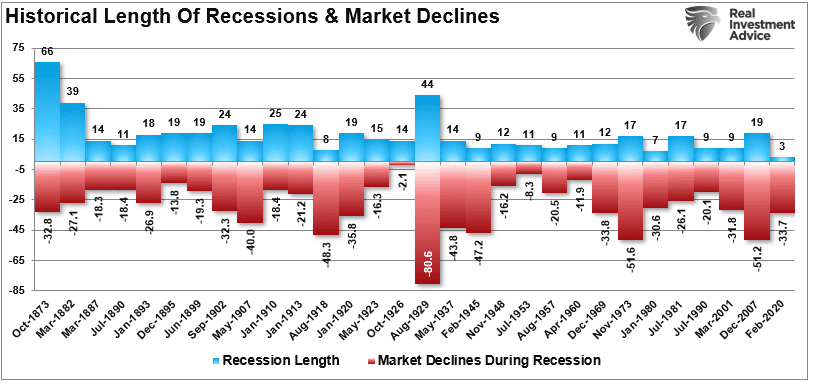

We have seen plenty, from trade wars to Brexit, to Fed policy and a global pandemic in recent years. Yet, before those events caused a market downturn, Wall Street analysts were wildly bullish that wouldn’t happen.

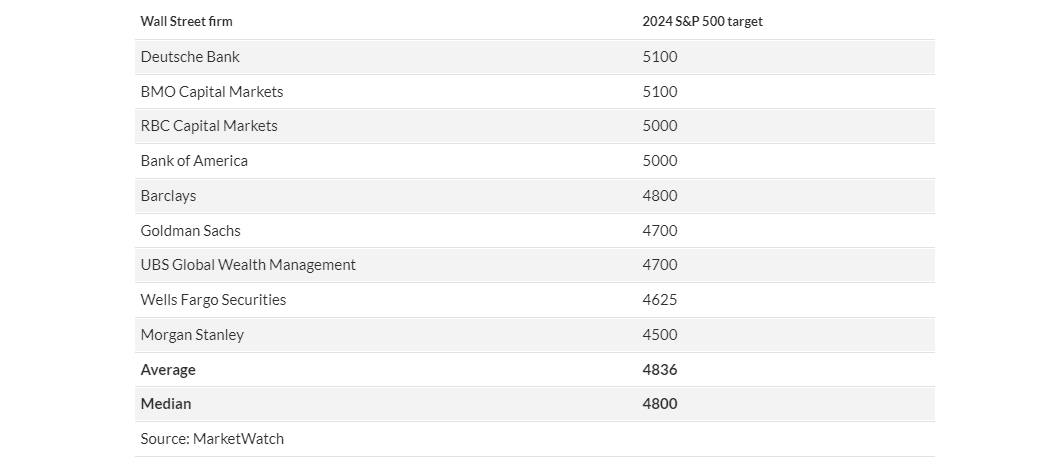

So what about 2024? We have some early indications of Wall Street targets for the S&P 500 index, and, as is always the case, they are primarily optimistic for the coming year.

“The estimates from sell-side strategists put the average target for the S&P 500 at 4,836 for the end of 2024, implying an advance of merely 6.3% from Monday’s close, according to MarketWatch calculations of the data (see table below). That is below the average yearly return of around 8% for the large-cap index since 1957 and its year-to-date surge of 18.5% in 2023, according to Dow Jones Market Data.” – MorningStar

Will next year be another bull market year for stocks, or will the bear finally come out of hibernation? We don’t have a clue but can make educated guesses about ranges given current valuations.

Estimating The Outcomes

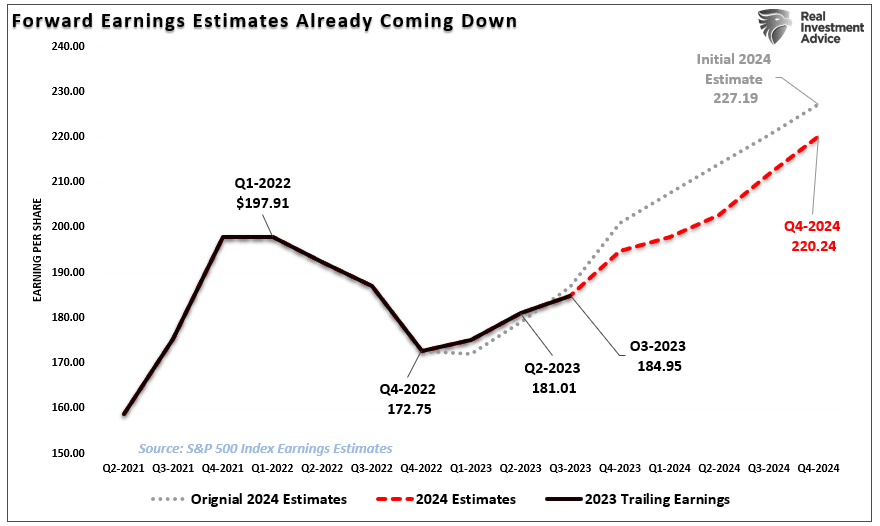

The problem with current forward estimates is that several factors must exist to sustain historically high earnings growth.

- Economic growth must remain more robust than the average 20-year growth rate.

- Wage and labor growth must reverse to sustain historically elevated profit margins, and,

- Both interest rates and inflation must reverse to very low levels.

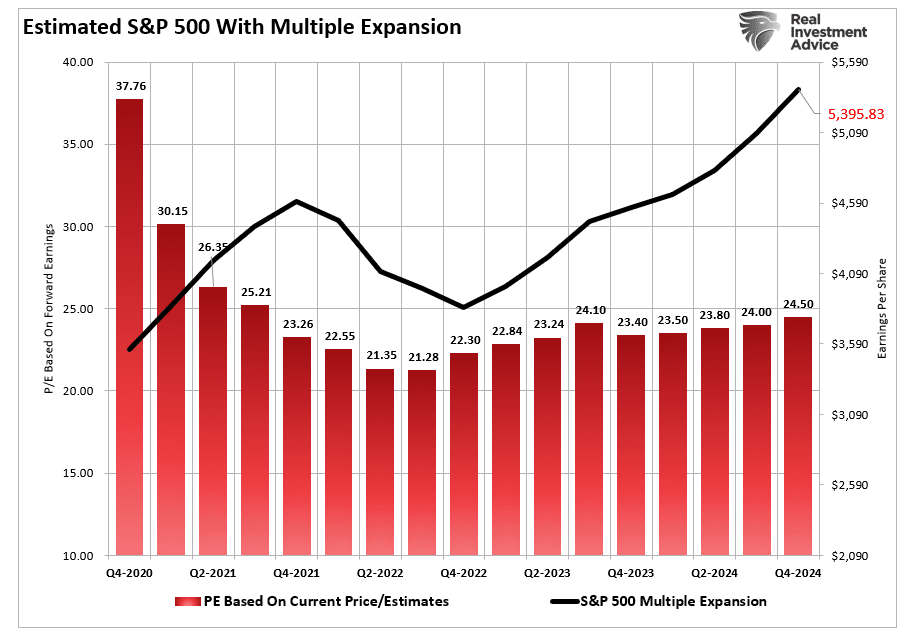

While such is possible, the probabilities are low, as strong economic growth can not exist in a low inflation and interest-rate environment. More notably, if the Fed cuts rates, as most economists and analysts expect next year, such will be in response to a near-recessionary or recessionary environment. Such would not support current strong earnings estimates of $220.24 per share next year. This represents roughly 20% from Q3-2023 levels, which is the most recently completed quarter.

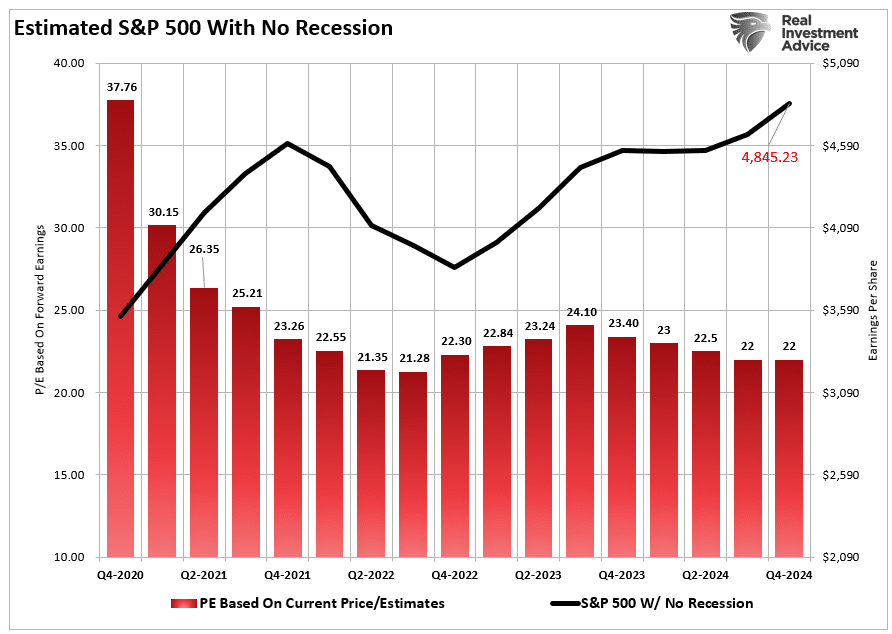

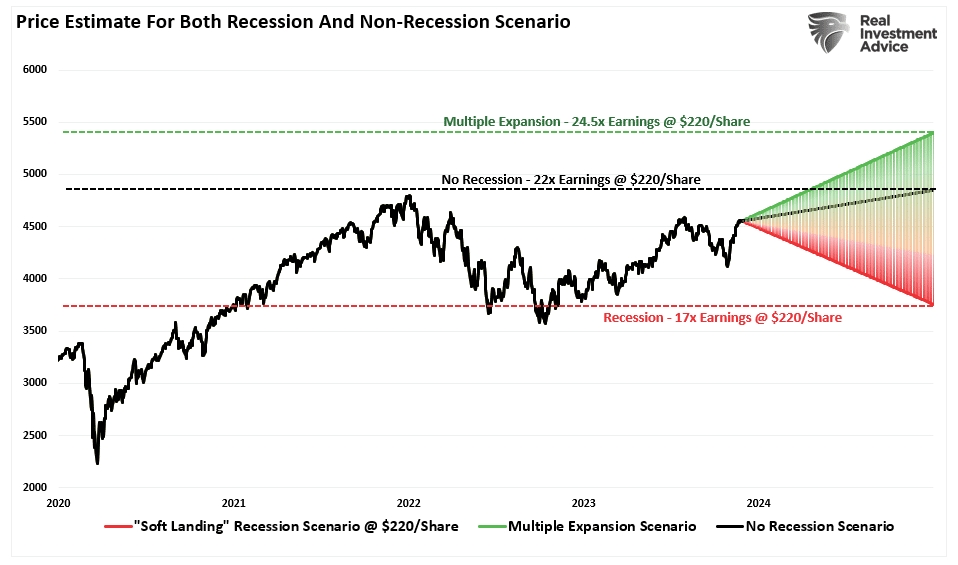

Nonetheless, with that said, we can use the current forward estimates, as shown above, to estimate both a recession and non-recession price target for the S&P 500 as we head into 2024. These assumptions are based on valuation multiples within ranges of current market levels.

In the NO-recession scenario, the assumption is that valuations will fall slightly as earnings increase to 22x earnings over the next year. (22x earnings has been the average over the last few years.) The S&P 500 should theoretically trade at roughly 4845 by 2024 based on current estimates. Given the market is trading at approximately 4550 (at the time of this writing), such would imply a 6.5% increase from current levels.

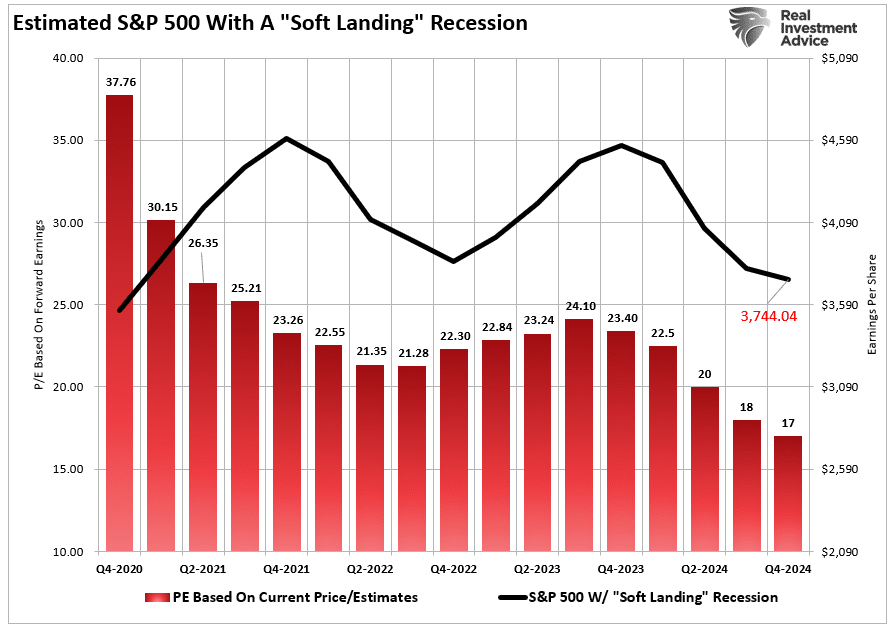

However, should the economy slip into a mild recession, valuations would be expected to revert toward the longer-term median of 17x earnings. Such would imply a level of 3744 or roughly a 17% decline next year.

While an additional 17% decline from current levels seems hostile, such would align with typical recessionary bear markets.

Which would also coincide with Fed rate cuts to offset the deflationary risk to the economy.

However, we must consider one more scenario.

Maybe The Bulls Are Right

We would be remiss in not providing for a bullish outcome in 2024. However, we must consider several factors for that bullish outcome to take shape.

- We assume the $220/share in year-end estimates remains valid.

- That the economy avoids a recession even as inflation falls

- The Federal Reserve pivots to a lower interest rate campaign.

- Valuations remain static at 22x earnings.

In this scenario, the S&P 500 should rise from roughly 4550 to 5395 by the end of 2024. Such would imply an 18.5% gain for the year. Given the market is up approximately 19% in 2023, such a gain

The chart below combines the three potential outcomes to show the range of possible outcomes for 2024. Of course, you can do the analysis, make valuation assumptions, and derive your targets for next year. This is just a logic exercise to develop a range of possibilities and probabilities over the next 12 months.

Conclusion

Here is our concern with the bullish scenario. It entirely depends on a “no recession” outcome, and the Fed must reverse its monetary tightening. The issue with that view is that IF the economy does indeed have a soft landing, there is no reason for the Federal Reserve to reverse reducing its balance sheet or lower interest rates.

More importantly, the rise in asset prices eases financial conditions, which reduces the Fed’s ability to bring down inflation. Such would also presumably mean employment remains strong along with wage growth, elevating inflationary pressures.

While the bullish scenario is possible, that outcome faces many challenges in 2024, given the market already trades at fairly lofty valuations. Even in a “soft landing” environment, earnings should weaken, which makes current valuations at 22x earnings more challenging to sustain.

Our best guess is that reality lies somewhere in the middle. Yes, there is a bullish scenario where earnings decline and a monetary policy reversal leads investors to pay more for lower earnings. But that outcome has a limited lifespan as valuations matter to long-term returns.

As investors, we should hope for lower valuations and prices, which gives us the best potential for long-term returns. Unfortunately, we don’t want the pain of getting there.

Regardless of which scenario plays out in real-time, there is a reasonable risk of weaker returns over the next year than what we saw in 2023.

That is just the math.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.