Stocks ticked higher last week, with the S&P 500 rising 0.2% to close at 4,604.37. The index is now up 19.9% year to date, up 28.7% from its October 12, 2022 closing low of 3,577.03, and down 4% from its January 3, 2022 record closing high of 4,796.56.

Job gains continue at a healthy pace, but they have cooled significantly. (Source: @WhiteHouseCEA)

It’s great news that U.S. economy continues to create a lot of jobs every month. Just on Friday, we learned employers added a healthy 199,000 jobs in November.

Still, it’s worth having a frank discussion about how the economy is cooling. As you can see in the chart above, the pace of job gains has come down significantly from summer 2021 levels.

To be clear, this is not to suggest that we’re doomed for a recession. Rather, it’s an acknowledgement that some of the unusual massive forces that have been juicing growth over the past few years have been easing. And the data seems to confirm economic conditions have gone from very hot to something that’s a bit more normal.

A Quick Look Back

A year ago, many economists were warning the U.S. was barreling toward a recession.

At the time, it was a bit challenging to make sense of these bearish predictions considering the persistent massive economic tailwinds signaling future growth and the many other reasons for optimism.

Importantly, inflation at the time had already been cooling for months despite persistent economic growth — evidence that we could see a bullish “Goldilocks” soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession. (This is a narrative we’ve been repeating every week in TKer’s weekly review of the macro crosscurrents).

With the benefit of hindsight, we now know the economy created jobs every month year to date, consumer spending climbed to new record highs, and GDP growth remained positive and even accelerated in Q3.

Upgrade to paid

We’re Going From Great Times To Good Times

One of the most clicked and shared TKer newsletters ever is the March 4, 2022 issue: Three massive economic tailwinds I can't stop thinking about

Those three tailwinds: The unprecedented trillions of dollars worth of excess savings accumulated by consumers, the eye-poppingly high number of job openings, and the record-high levels of core capex orders.

These metrics are notable because they’re leading indicators: Excess savings represent extra money that has yet to be spent; elevated job openings represent hiring that has yet to happen, which also means incremental consumer spending power that has yet to be realized; and core capex orders represent capital goods businesses have yet to put in place, which means there’s still work to be done by manufacturers and that there’s more capacity coming for the businesses that ordered this stuff.

In recent months, these forces have trended toward more normal levels.

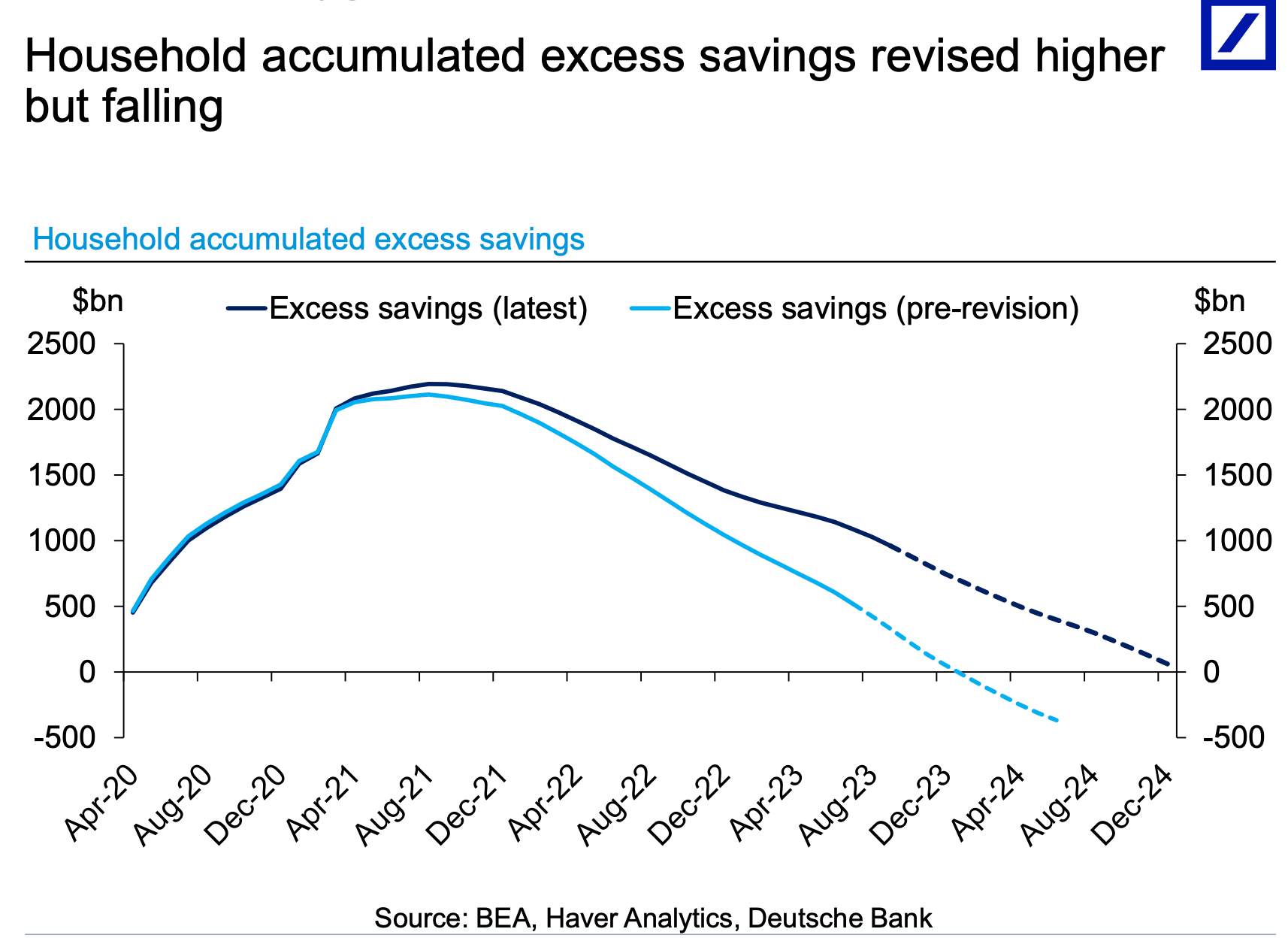

Excess savings have faded from peak levels, and most economists agree these balances will soon be depleted.

Excess savings are nearing depletion. (Source: Deutsche Bank)

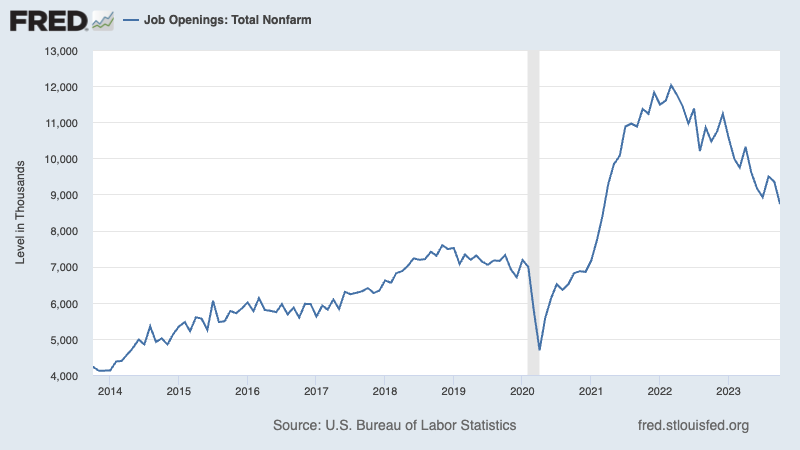

Job openings have come down significantly. According to the BLS’s Job Openings and Labor Turnover Survey, employers had 8.73 million job openings in October. This was the lowest print since March 2021, and it’s down significantly from the March 2022 high of 12.03 million.

The number of job openings have come down. FRED

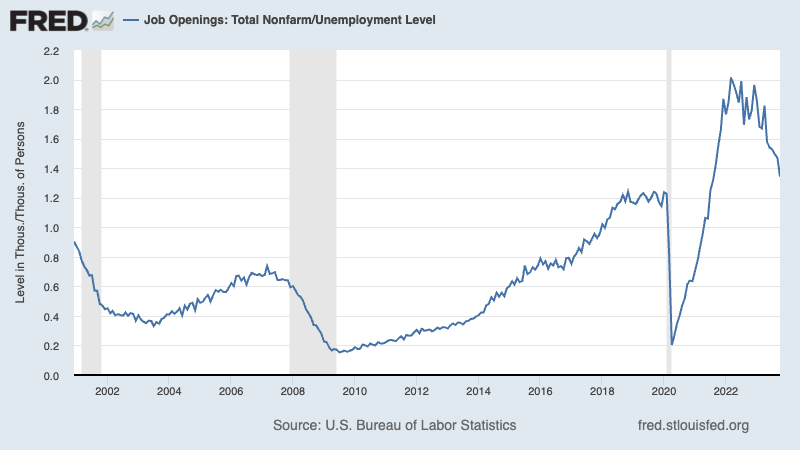

During the period, there were 6.50 million unemployed people — meaning there were 1.3 job openings per unemployed person. This metric — one of the most obvious signs of excess demand for labor — is close to prepandemic levels.

The ratio of job openings relative to the number of unemployed people is near prepandemic levels. FRED

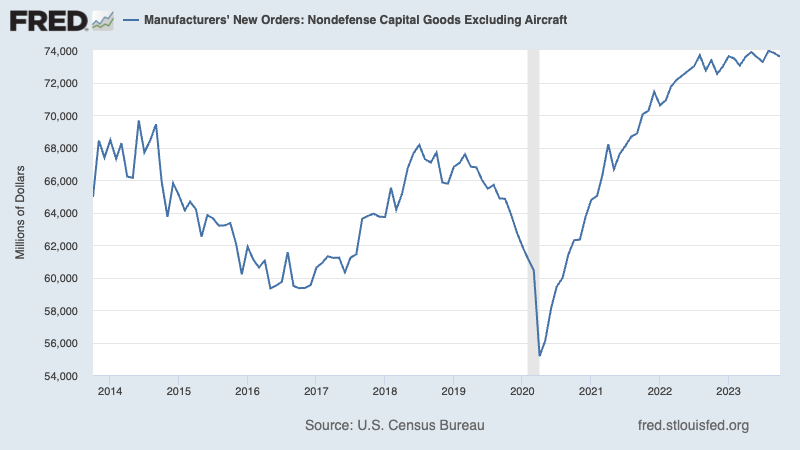

Orders for nondefense capital goods excluding aircraft — a.k.a. core capex or business investment — fell 0.3% to $73.59 billion in October. While this figure continues to trend near record levels, growth seems to be stalling.

Capex orders have been going sideways. FRED

Let’s Not Panic

Just because excess savings are down doesn’t mean people are out of money. People most definitely have money. People are sitting on a lot of wealth. It’s just that the extra cash sitting on top of all that money and wealth has largely been spent.

And just because job openings are down doesn’t mean the labor market is toast. There are still a lot of job openings. Furthermore, layoff activity remains low, hiring activity remains elevated, and claims for unemployment insurance remain depressed. It’s just that employers aren’t quite as desperate to fill open positions as they have been over the past two years.

And just because capex orders have gone sideways doesn’t mean business activity is going sideways. A lot of this equipment has yet to be delivered. Once in place, businesses are likely to be more productive than they once were.

Keep in mind that these cooling metrics are the intended effect of the Federal Reserve’s efforts to bring down inflation. (More here and here.) And in particularly good news, inflation rates have come down significantly from crisis levels.

Indeed, we seem to be realizing that bullish “Goldilocks” soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession. (Again, a narrative we’ve been repeating every week in TKer’s weekly review of the macro crosscurrents).

Here’s a great chart from economist Justin Wolfers tracking the trajectory of key measures of economic activity.

“What recession?” economist Justin Wolfers asks. (Source: @JustinWolfers)

As you can see, while the rate of growth may be decelerating for some key measures, they are nevertheless still growing.

“If I had asked you a year ago to sketch what you thought a soft landing might look like,” Wolfers tweeted after Friday’s jobs report, “it's likely you would have pretty much drawn the current economic data.”

But Let’s Also Not Get Complacent

I think it’s fair to say when growth rates cool and the forces juicing excess demand fade, you may be at greater risk of going into recession in the near future.

And let’s be realistic: Recessions happen.

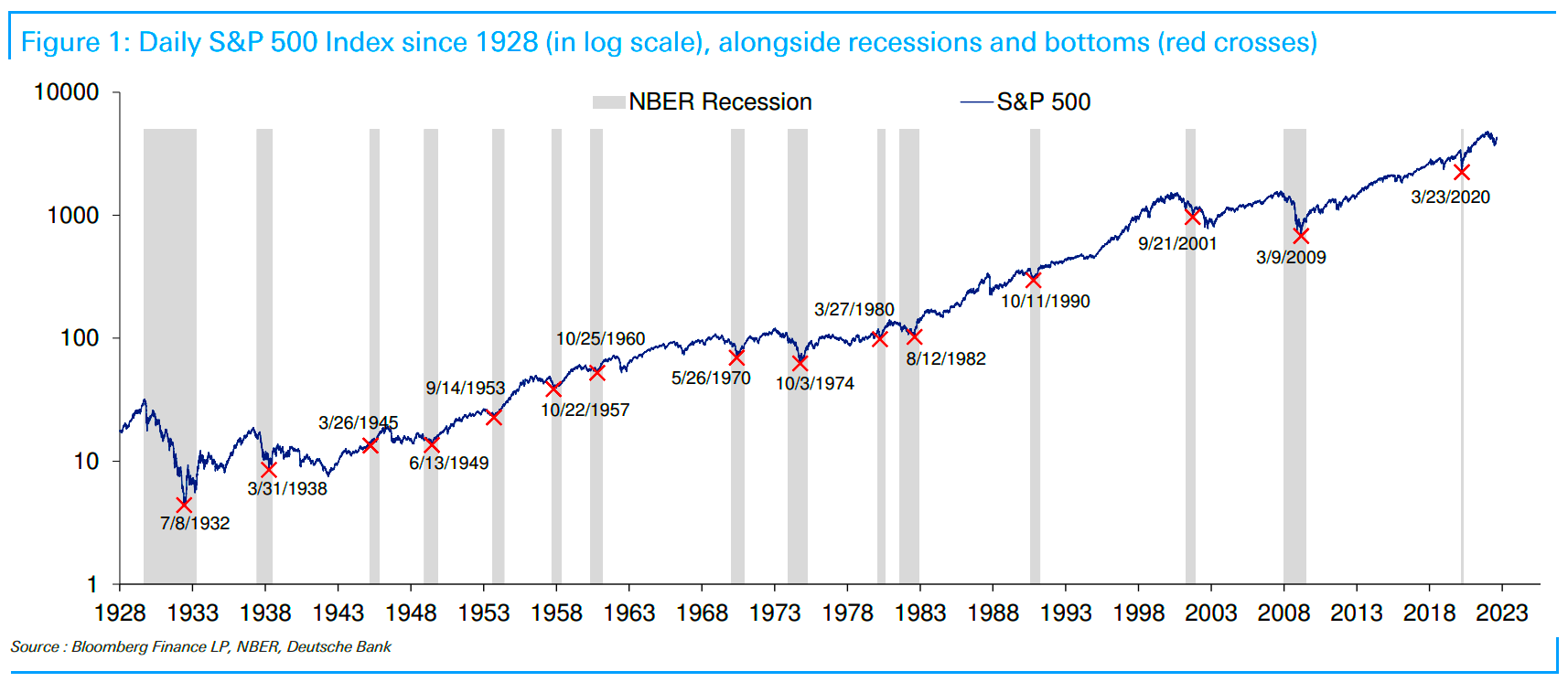

Recessions and the market volatility associated with economic downturns are unfortunate hurdles on the long-run path to building wealth in risk assets.

Long-term investors are almost certain to encounter a few recessions. (Source: Deutsche Bank via TKer)

Consequently, I don’t think it’s totally unreasonable that some economists are forecasting a recession in 2024.

At the same time, not all recessions are the same. It’s certainly possible that the next recession is a short and shallow one. And keep in mind that a recession at this point would begin as the economy is in an unusually and historically strong position — meaning that a recession may knock the economy from being very strong to just strong.

To reiterate, a recession in the near-term is no sure thing. But as the data continues to come in, we’ll have to be vigilant as we watch for signs that the economic narratives may be shifting.

A version of this post was originally published on Tker.co and appears here with permission.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.