- BofA's Vivek Arya keeps Neutral on Intel with $50 target, expects Q4 in line but Q1 sales miss on various headwinds.

- Arya sees modest Intel growth, but challenges in regaining market share and reaching 60% gross margin target amid stiff competition.

- Up Next: Get 5 Dark Horse Stocks Wall Street Is Quietly Loading Up On

BofA analyst Vivek Arya reiterated a Neutral rating on Intel Corp INTC with a price target of $50.

The analyst expects a fourth quarter in line and modestly ahead, with $15.1 billion in sales, 46.5% gross margin, and ~$0.45 EPS. He modeled a first-quarter miss with $13.5 billion in sales, down 11% sequentially, well below the consensus decline of 6% sequentially on multiple headwinds, including Mobileye outlook cut, PC seasonality, weak industrial/auto, networking, and muted enterprise.

Also Read: ASML’s Latest Earnings Reveal: A Lucrative Quarter Amid Rising Chip Demand

Arya noted that the gross margin trajectory could surprise the upside as Intel benefits from its cost restructuring actions, leading to higher EPS. He lowered his calendar 2024 sales to $58.5 billion, +8.5% year-on-year versus +9.7% prior and below consensus $61.3 billion. However, he tweaked the calendar 2024 EPS to $1.48, though still below the $1.82 consensus.

While Intel has laid out a long-term 60% gross margin target, many things have to go right to get back to historical trends (calendar year 2014 to calendar year 2017), as those were achieved in a growing PC and data center market when Intel had 95% CPU value share (versus 71%), and when it had much lower capex intensity (~17.5% vs. 30-35%) and related lower depreciation burden (9-10% versus 14-15%).

Arya estimated Intel exited fiscal fourth quarter 2023 at around 46%-47% and will likely have a 60%-70% incremental margin trend for the next two years as it executes on its five nodes in 4 years (5N4Y) roadmap.

The analyst modeled calendar years 2024, 2025, and 2026 gross margins at 45.5%, 46.8%, and 48.4%, about 200bps below consensus.

Trending Investment Opportunities

Expanding gross margin to over 50% is critical for the chip designer to march towards the $3+ in EPS that bullish investors could seek.

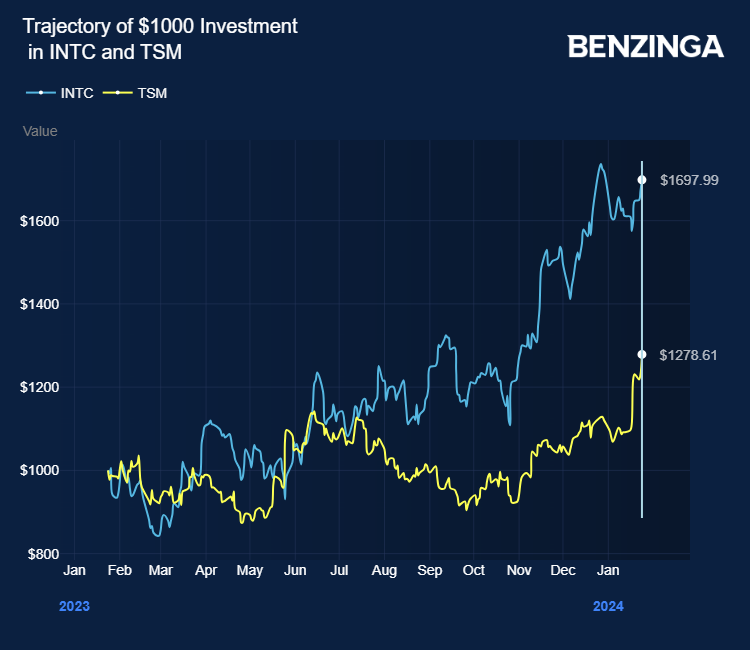

Intel’s 25x NTM PE is nearly 2x its historical 13x multiple, implying investors are placing a more significant probability on Intel’s ability to catch up to Taiwan Semiconductor Manufacturing Company Ltd TSM in manufacturing.

While Arya noted the possibility of Intel’s 18A progress and ability to sign up prominent foundry customers like Nvidia Corp NVDA, TSMC will remain dominant, especially when normalized for scale, manufacturing yields, and proven reliability.

He also noted that Intel might not be able to achieve more than a low single-digit foundry share as its fabless customers are too dependent on TSMC (and Samsung).

Separately, Arya still noted the potential for Arm Holdings Plc ARM to make more inroads into data center and PC markets over time.

Price Action: INTC shares traded higher by 0.38% at $49.08 on the last check Wednesday.

Photo via Wikimedia Commons

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|