Campbell Soup Company CPB continues to demonstrate resilience amid a difficult consumer landscape, driven by a robust supply chain, successful innovations and effective marketing programs.

The company's savings plan has also been adding to its success story. Through the second quarter of fiscal 2024, the company generated $915 million in savings under its multi-year cost-saving program, including Snyder's-Lance synergies. Management remains on track to deliver savings worth $1 billion by the fiscal 2025-end.

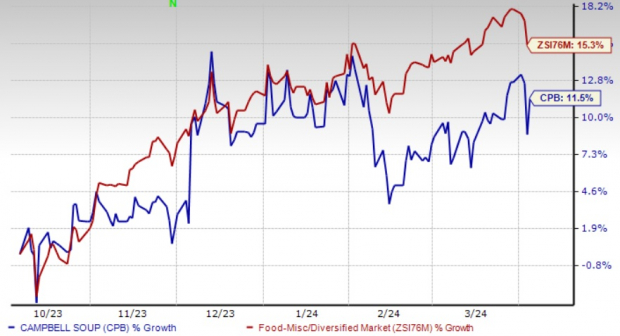

What's Working Well for CPB?

Campbell Soup is well-positioned to capitalize on various opportunities within its portfolio to align with evolving consumer trends. The company's strategies and plans are focused on three key areas, which include ensuring product affordability and maintaining competitive pricing within the boundaries of margin goals; sustaining marketing and innovation initiatives; and adhering to a disciplined and balanced spending approach with a focus on high return on investment and impactful plans.

The ongoing momentum, coupled with the acquisition of Sovos Brands (concluded in Mar 2024), positions Campbell Soup for accelerated growth, solidifying its position in the food industry. This acquisition is a significant step for Campbell as it enhances its Meals & Beverages portfolio with high-growth brands like Rao's sauce, Michael Angelo's and noosa. Sovos Brands brings a range of premium products to Campbell, including pasta sauces, dry pasta, soups, frozen entrées, frozen pizza and yogurts.

Image Source: Zacks Investment Research

Moving on, Campbell Soup has been benefiting from its Snacks business, which formed 43.7% of total sales in the second quarter of fiscal 2024. Net sales in the division rose 1% on an organic basis during the quarter, attributed to sales of eight power brands, which rose 4%. Despite a tough economic landscape, sales grew fueled by strength in brands like Goldfish, Lance, Kettle Brand and Cape Cod.

Management's direct store delivery (DSD) transformation initiative is expected to fuel further growth and margins in the Snacks division. This is expected to be achieved through three core elements, including the creation of one snacking DSD logistics and warehouse network, the modernization of tools and technology used by the company's important independent distribution partners and a focus on DSD routes.

What Else to Know?

Campbell Soup has been navigating a volatile consumer landscape. In second-quarter fiscal 2024, the top line declined 1% year over year. Organic net sales also declined 1% due to the soft volume/mix (down 2% year over year), somewhat offset by net price realization (up 1%). Macroeconomic headwinds are likely to continue affecting certain categories and consumer demographics in the near term.

For fiscal 2024, the company expects net sales growth between a 0.5% decline and an increase of 1.5%. Organic sales growth is likely to come between flat and an increase of 2%. On its second-quarter earnings call, management stated that the company was pacing toward the lower end of the fiscal 2024 net sales view, with expectations to witness a sequential improvement throughout the year. For the third quarter, management expects a flat to low-single-digit increase in organic sales, with a continued sequential increase anticipated in the fourth quarter.

Apart from this, Campbell Soup has been witnessing cost inflation for a while and expects core inflation to stay within the low-single-digit range in fiscal 2024. Management expects to continue brand-related investments in fiscal 2024. It envisions marketing and selling expenses to range between 9 and 10% as a percent of net sales in fiscal 2024, with more spending anticipated in the third quarter compared with the fourth quarter.

That said, the company expects earnings and margin improvements in the second half of fiscal 2024, mainly in the fourth quarter. This reflects a moderating inflationary landscape, together with ongoing productivity enhancements and improving volume trends.

For fiscal 2024, adjusted EBIT is forecasted to be up 3-5%. Adjusted EPS is envisioned to increase 3-5% to the $3.09-$3.15 band. In the third quarter, it expects the adjusted EPS to come in the low 70 cents range compared with the year-ago period figure of 68 cents.

Shares of the Zacks Rank #3 (Hold) company have rallied 11.5% in the past six months compared with the industry's growth of 15.3%.

3 Appetizing Bets

The Chef's Warehouse CHEF, which engages in the distribution of specialty food products, currently carries a Zacks Rank #2 (Buy). CHEF has a trailing four-quarter earnings surprise of 3.2%, on average.

The Zacks Consensus Estimate for The Chef's Warehouse's current fiscal-year sales and earnings suggests growth of 8.7% and 4.7%, respectively, from the year-ago reported numbers.

Vital Farms Inc. VITL offers a range of produced pasture-raised foods. It currently carries a Zacks Rank #2. VITL has a trailing four-quarter average earnings surprise of 155.4%.

The Zacks Consensus Estimate for Vital Farms' current financial-year sales and earnings suggests growth of 18.6% and 35.6%, respectively, from the year-ago reported numbers.

Utz Brands Inc. UTZ manufactures a diverse portfolio of salty snacks and currently carries a Zacks Rank #2. UTZ has a trailing four-quarter earnings surprise of 2.6%, on average.

The Zacks Consensus Estimate for Utz Brands' current financial-year earnings suggests growth of 17.5% from the year-ago reported numbers.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.