Speaking of bipolar - F5 Networks (FFIV) is up 11% off its earnings report and Netflix (NFLX) is down 9% as of this typing. We cut back positions in both yesterday since the gambling mentality around earnings reports is not our cup of tea. I thought both reports were quite good; the only issue with Netflix was a slight miss on revenue ... so despite a 10 cent beat on EPS the company is punished this morning. No surprise there because at that level of valuation you have to exceed the Street in every metric, and even then it's sometimes not enough.

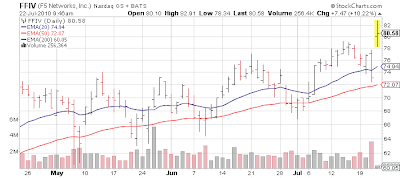

Technically, obviously F5 is as good as it gets right now... buy on pullbacks is the game plan. It is "safe" for the next 90 days, until we repeat the whole exercise. Netflix has some damage done by its gap down, so we'll assess how it does in the next few days. If it cannot recapture the 50 day of $111 it could have some trouble, but that is only $3-4 away.

A quick look at both names

F5 Networks (full report here) Not just an earning beat, and raised guidance but operating margins of 33.6%, increased gross margins and even a small share buyback.

Guidance:

F5's fiscal "year" ends in August 2010, so should earn $2.35+ for 2010. This is now around 34-35x forward estimates which is getting rich but with so few companies in America growing in excess of 25% on an organic basis, people are willing to bid up the few that can. Until the charts say the story has changed, it remains one to ride.

[Apr 22, 2010: F5 Networks Results Solid, but Market Expectations High]

[Jan 21, 2010: F5 Networks Executing Well]

[Apr 8, 2009: Stimulus Fire Hydrant (Worldwide) Should Benefit Networking Companies/Broadband]

--------------------------------------------

Netflix (full report here) The problem here is mostly a bar that has been raised so high. Very little not to like, and the continued growth of online streaming versus the old "postal" model is a big positive. Any incremental drop in postage costs is a good thing. The trick here is the streaming revenue is lower, but the costs are also much lower - so as the model changes, Wall Street will need to adjust. The Street is very short sighted and everything is about "the quarter" and "hitting X number", rather than seeing this is a very positive change; a world without postage costs for NFLX would be a very good thing. NFLX also added another 1M customers. (year over year subscriber growth over 40%)

We wrote a few weeks ago that the recently announced deal with Apple (iPad) could be a big boost to Netflix and it appears so.

Main issue of course is competition in streaming, but with very good customer service and the fact that most people are not going to change services once they sign up (barring a horrid experience) the first mover advantage for NFLX is going to be a boon. Very similar to Apples first mover in digital music. But we'll have to see how the competition - namely Hulu - shapes up in the coming year(s).

Last, while Netflix needs to worry about Hulu, so does Hulu need to worry about Netflix. NFLX is thought of as a "movie" company but it is charging hard into TV shows, where Hulu is "the man".

Guidance:

Obviously this type of growth does not come cheap.

Long Netflix, F5 Networks in fund; no personal position

Market News and Data brought to you by Benzinga APIsTechnically, obviously F5 is as good as it gets right now... buy on pullbacks is the game plan. It is "safe" for the next 90 days, until we repeat the whole exercise. Netflix has some damage done by its gap down, so we'll assess how it does in the next few days. If it cannot recapture the 50 day of $111 it could have some trouble, but that is only $3-4 away.

A quick look at both names

F5 Networks (full report here) Not just an earning beat, and raised guidance but operating margins of 33.6%, increased gross margins and even a small share buyback.

- F5 Networks Inc (FFIV)., whose products manage and route computer network traffic, said Wednesday its fiscal third-quarter profit soared as revenue grew amid improving demand. The results and F5's guidance for the current quarter beat Wall Street's expectations.

- For the three months ended June 30, the company earned $40.5 million, or 50 cents per share, up 78% from a profit of $22.8 million, or 29 cents per share, in the same period a year earlier. Excluding stock options expenses, the company earned 66 cents per share in the latest quarter.

- Revenue rose 46% to $230.5 million from $158.2 million.

- Analysts, on average, were expecting a profit of 59 cents per share on revenue of $218.4 million, according to a poll by Thomson Reuters.

- F5 said strong revenue growth and improvement in its product gross margin enabled it to hire about 80 new employees during the quarter.

- Reflecting the growth of new and renewed service maintenance contracts booked during the quarter, deferred revenue increased to $239.6 million, up 6% from the prior quarter and 41% from the third quarter of fiscal 2009.

- After repurchasing 291,027 shares of its outstanding common stock the company ended the quarter with $781 million in cash and investments.

Guidance:

- For the fourth quarter, the company forecast a profit of 53 cents to 55 cents per share, adjusted earnings of 69 cents to 71 cents per share and revenue of $242 million to $247 million. Analysts expect a profit of 62 cents per share on revenue of $230.2 million.

F5's fiscal "year" ends in August 2010, so should earn $2.35+ for 2010. This is now around 34-35x forward estimates which is getting rich but with so few companies in America growing in excess of 25% on an organic basis, people are willing to bid up the few that can. Until the charts say the story has changed, it remains one to ride.

[Apr 22, 2010: F5 Networks Results Solid, but Market Expectations High]

[Jan 21, 2010: F5 Networks Executing Well]

[Apr 8, 2009: Stimulus Fire Hydrant (Worldwide) Should Benefit Networking Companies/Broadband]

--------------------------------------------

Netflix (full report here) The problem here is mostly a bar that has been raised so high. Very little not to like, and the continued growth of online streaming versus the old "postal" model is a big positive. Any incremental drop in postage costs is a good thing. The trick here is the streaming revenue is lower, but the costs are also much lower - so as the model changes, Wall Street will need to adjust. The Street is very short sighted and everything is about "the quarter" and "hitting X number", rather than seeing this is a very positive change; a world without postage costs for NFLX would be a very good thing. NFLX also added another 1M customers. (year over year subscriber growth over 40%)

- Netflix Inc's (NFLX) second-quarter revenue missed Wall Street's expectations as many new subscribers signed up for lower-priced plans that offer unlimited streaming. While revenue fell short of forecasts, the Web video subscription service's earnings jumped 34% on improved margins as customers opted to stream movies and TV shows rather than order discs via mail, helping to drive down costs.

- 61% of all of Netflix’s subscribers streamed at least 15 minutes of content in Q2 — this is up from 37% a year ago, and 55% in the Q1 2010.

- Second-quarter revenue rose to $519.8 million from $408.5 million. Analysts on average had forecast earnings of 70 cents on revenue of $524.4 million.

- Netflix reported second-quarter net income of $43.5 million, or 80 cents per share, up from $32.4 million, or 54 cents per share, a year ago. Analysts expected 70 cents.

- Netflix ended the quarter with 15 million subscribers, up 42 percent from 10.6 million a year ago. The quarterly total was at the top of Netflix's own projected range for the quarter, but analysts had hoped it would blow past it.

- Netflix expects to end the third quarter with 16.3 million to 16.7 million subscribers, and the year with 17.7 million to 18.5 million subscribers.

- Churn was 4%, down from 4.5% a year ago, but up from 3.8% in Q3.

We wrote a few weeks ago that the recently announced deal with Apple (iPad) could be a big boost to Netflix and it appears so.

- Netflix's various deals to offer its streaming service through consumer electronic devices has paid off handsomely, and on Wednesday, Hastings said the recent introduction of Apple Inc's (AAPL) iPad has been a "big success" in terms of attracting new subscribers.

Main issue of course is competition in streaming, but with very good customer service and the fact that most people are not going to change services once they sign up (barring a horrid experience) the first mover advantage for NFLX is going to be a boon. Very similar to Apples first mover in digital music. But we'll have to see how the competition - namely Hulu - shapes up in the coming year(s).

- Analysts attribute much of the share price rise to the growing subscriber base and enthusiasm for the Internet streaming service market. But Wall Street is beginning to question when these near-term positives will give way to heightened competition and content cost inflation.

- "While Netflix enjoys the lead in Internet streaming, the barriers to entry are lower than ever, which will lead to more competition like Hulu Plus and an expected streaming service from Coinstar's (CSTR) Redbox," Scott said.

Last, while Netflix needs to worry about Hulu, so does Hulu need to worry about Netflix. NFLX is thought of as a "movie" company but it is charging hard into TV shows, where Hulu is "the man".

- In terms of streaming content, we are rapidly expanding our TV shows available for streaming and since our last call we have added thousands of TV episodes from new deals with Fox, MTV Networks and Warner Television. These shows include all seasons of “24,” “Futurama,” “Lie To Me,” “The Chapelle Show,” “Nip/Tuck” and “Veronica Mars,” and in a few weeks all seasons of “The Family Guy” will be available to stream as well. We see TV shows as equally important to our franchise as movies.

Guidance:

- For Q4, the company expects revenue of $580 million to $596 million, with profits of 58-73 cents a share, and quarter-end subscribers of 17.7 million to 18.5 million, up from a previous forecast of 16.5 million to 17.3 million.

- For the full year, the company now sees revenue of $2.14 billion to $2.16 billion, up from a previous range of $2.11 billion to $2.16 billion, with profits of $2.58 to $2.86 a share, up from a previous range of $2.41 to $2.63.

Obviously this type of growth does not come cheap.

Long Netflix, F5 Networks in fund; no personal position

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In: Communications EquipmentComputer HardwareConsumer DiscretionaryInformation TechnologyInternet RetailSpecialized Consumer Services

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in