When it comes to understanding new developments in the economy or the markets, the obvious and simplest explanations aren’t always the correct or complete ones.

Consider the impact of higher interest rates. Higher rates are bad, right?

Two years ago, the Federal Reserve began hiking interest rates aggressively in its effort to cool inflation by slowing the economy. Sure, inflation rates have come way down and many economic metrics reflect decelerating growth. But the impact of higher rates has been far less severe than many expected, as reflected by upward revisions to 2023 and 2024 GDP growth forecasts. There were even economists warning of recessions that never came.

The Wall Street Journal just published a feature on this recession that has yet to come. WSJ

That’s because higher rates aren’t only bad. There’s also a brighter side of higher interest rates.

Households and businesses have been earning more interest income on their cash and new bond holdings. From The Wall Street Journal on Wednesday:

Washington has pumped out trillions of dollars in recent years for pandemic relief, clean-energy projects and more, selling Treasurys to finance soaring budget deficits. The snowballing debt, coupled with the highest rates in more than two decades, pushed government interest expenses to a seasonally adjusted annual rate of nearly $1.1 trillion, according to first-quarter figures from the Commerce Department.

That is income for cash-rich companies or Americans who park savings in money-market funds, where 5% annual returns can turn into a surprise five figures…

Andy Constan, chief executive of the investment consulting firm Damped Spring Advisors, said the higher government-bond payouts likely boosted Americans’ overall spending.

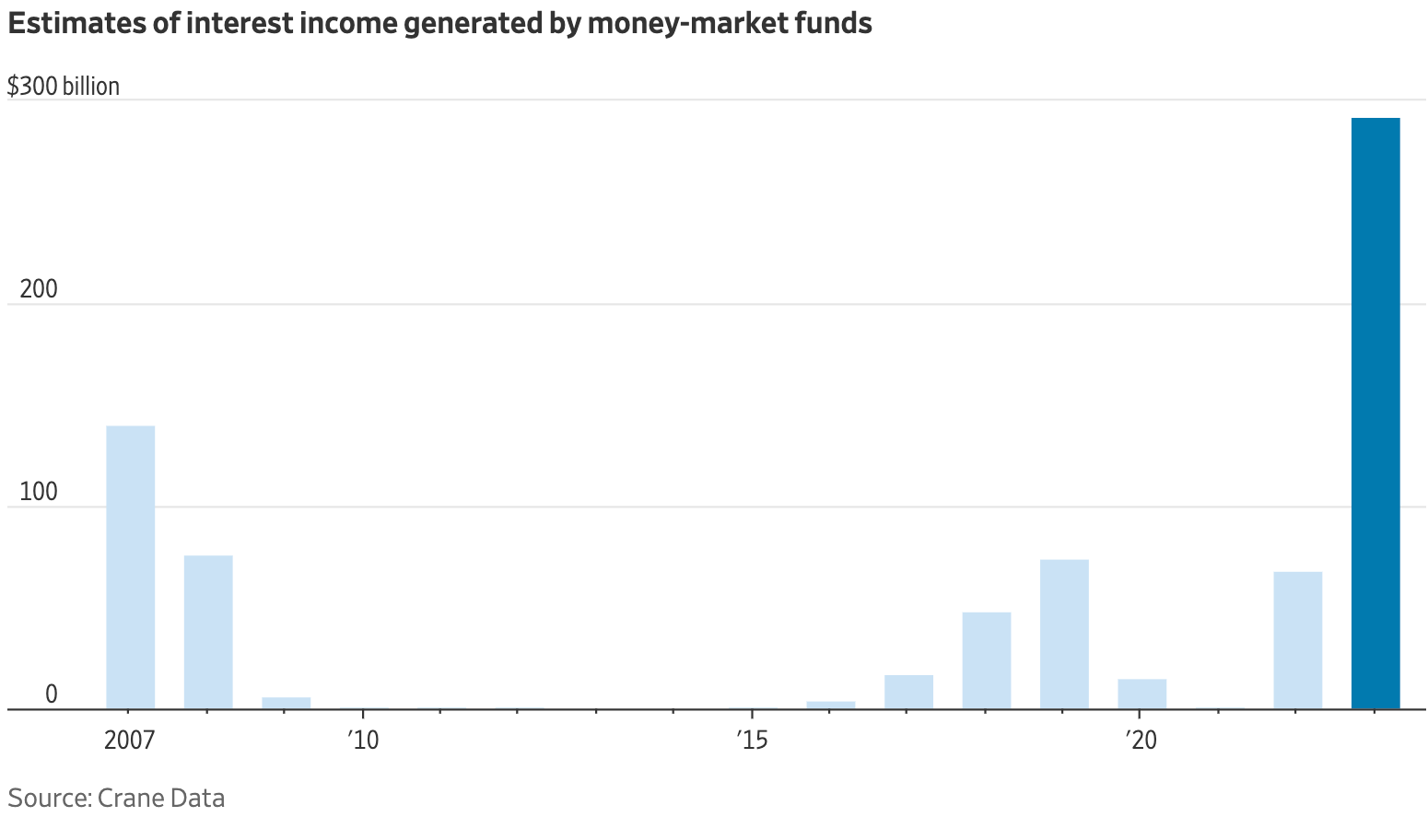

According to previous reporting by the WSJ’s Gunjan Banerji, “Investors parking cash in money-market funds [in 2023] reaped around $300 billion in interest income — more than in the prior decade combined.”

Investors generated a historic amount of income from money-market funds in 2023. WSJ

Of course, this financial tailwind mostly applies to those with a lot of cash and not too much debt.

In a research note published on Wednesday, JPMorgan’s Michael Feroli cautioned against jumping to the conclusion that higher rates are an obvious net benefit for economic activity: “[I]nterest income effects are only meaningful when the marginal propensity to consume of interest receivers is materially different from that of interest payers.“

Still, he concluded that “interest income flows may boost aggregate demand by a tenth or two of GDP.“

In other words, it’s possible higher interest rates have indeed been a tailwind — not a headwind — for the economy. Or as Yahoo Finance’s Myles Udland characterized it: a “backward problem” for the Fed.

A Low Saving Rate Isn’t Necessarily A Bad Thing

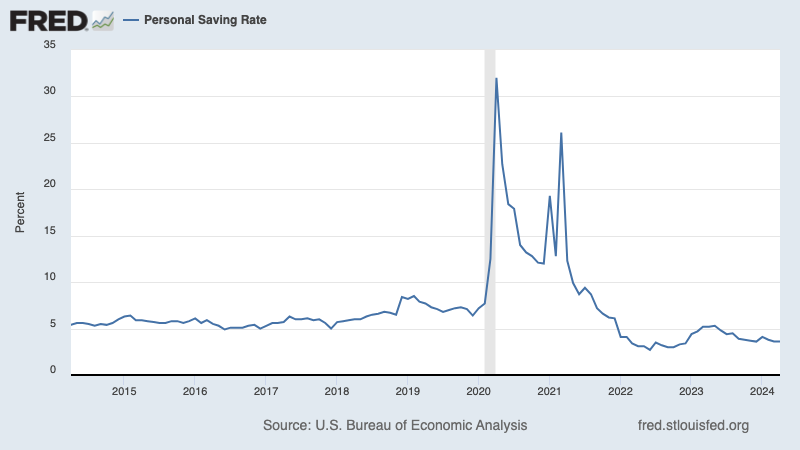

While we’re on the subject of household finances, we should talk about the personal saving rate (i.e., the percent of income left after spending money and paying taxes), which at 3.6% is down from its highs and is trending below prepandemic levels.

Americans aren’t putting away as much each month as they used to. FRED

A low saving rate intuitively sounds less than great. It sounds like people aren’t earning enough to save, or maybe they’re spending increasingly irresponsibly.

Or maybe it’s neither of those explanations.

Keep in mind that the personal saving rate reflects a snapshot of monthly behavior. So its decline doesn’t tell us much about cumulative savings.

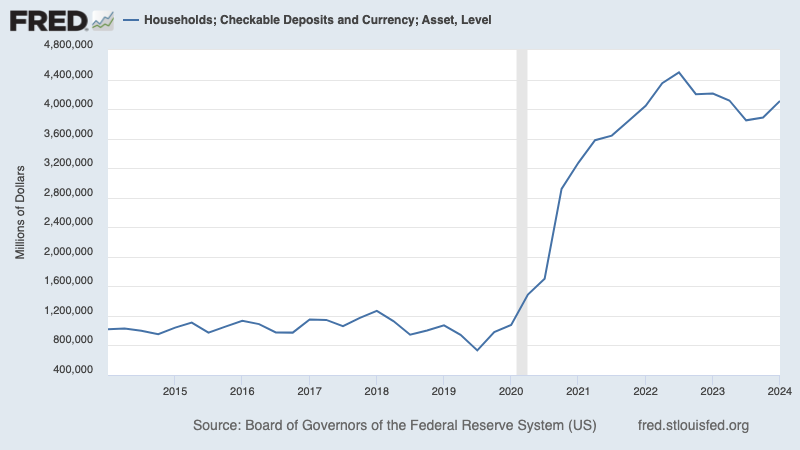

According to Federal Reserve data released Friday, households have over $4 trillion in checkable deposits sitting in bank accounts, which is about quadruple prepandemic levels.

American households have a lot of cash in the bank. FRED

And for households, it’s not just cash in the bank. Record high stock prices and higher home prices have helped fuel household net worth to record highs.

If you’re sitting on a ton of wealth, do you really need to be putting away more money?

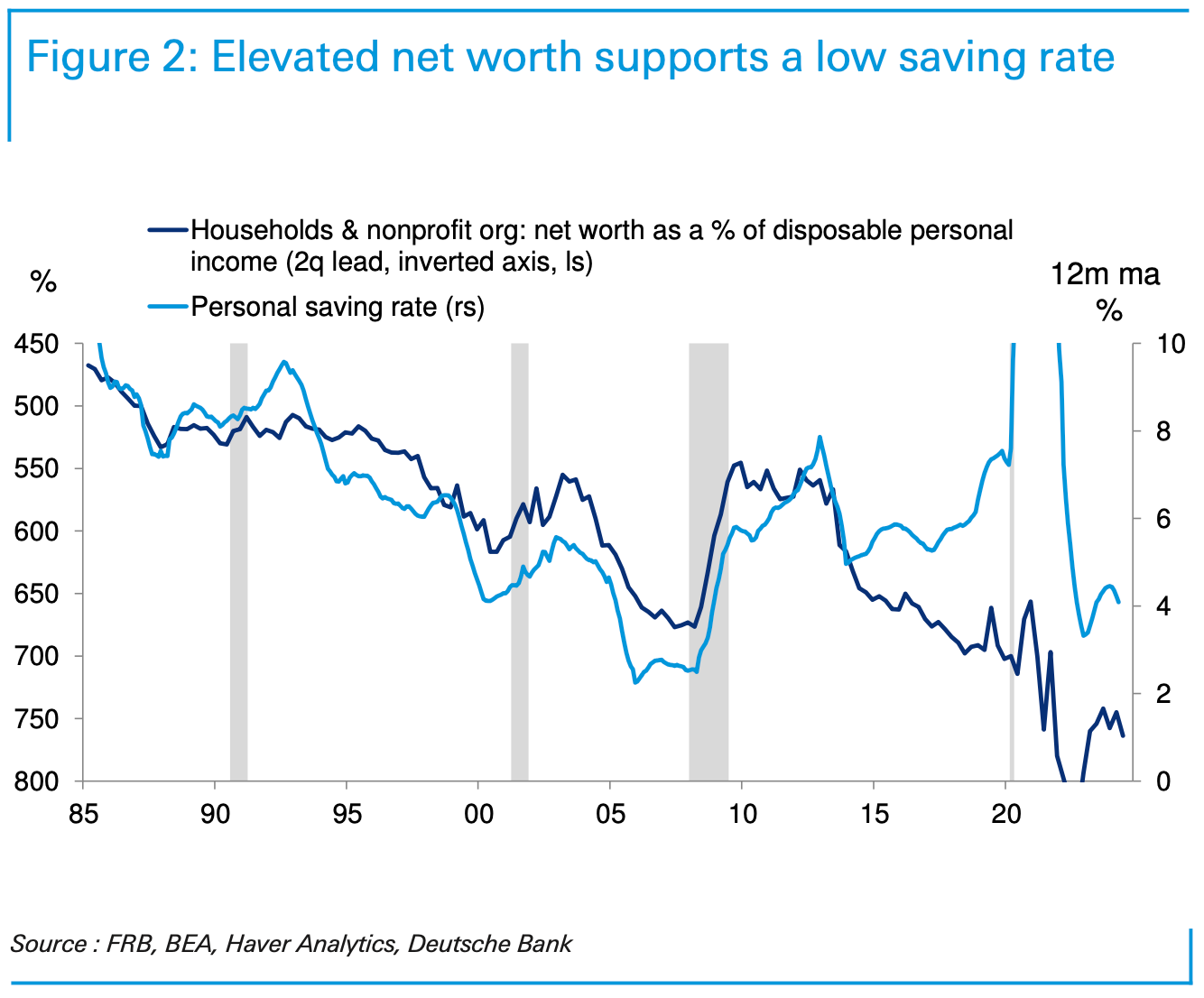

“Elevated net worth supports a low saving rate,” Deutsche Bank’s Matthew Luzzetti wrote on Monday.

Rising household net worth can be associated with a falling saving rate. (Source: Deutsche Bank)

TKer subscribers first read about this relationship last September when Renaissance Macro’s Neil Dutta explored this phenomenon.

“When you are ‘loaded,’ you have less reason to save,” Dutta wrote. “If my stock portfolio is rising and home prices are climbing, I don't feel like I need to be saving as much.“

Zooming Out

All of this speaks to TKer’s rule No. 1 of analyzing the economy: Don’t count on the signal of a single metric.

We’re lucky to have so many angles on the economy. Almost every day, we get periodic updates on things like jobs, manufacturing activity, housing, income, spending, sentiment, and so on. The confluence of these macro crosscurrents make for a rich mosaic on the economy.

Despite months and years of rising interest rates and falling saving rates, the bulk of the economic data has overwhelmingly confirmed consumer spending has been increasing, business investment has been rising, and aggregate wealth has been growing.

Keep this in mind as fear mongers and ill-informed commentators cherrypick data and mischaracterize it to suit their own interests.

A version of this post was originally published on Tker.co.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.