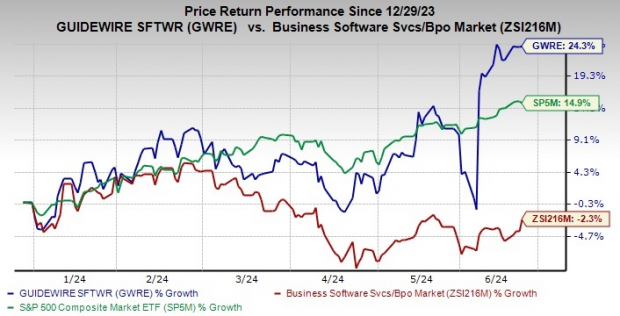

Guidewire Software's GWRE shares have been performing well on the trading front with a gain of 24.3% year to date compared with 14.9% growth of the S&P 500 composite. The sub-industry has declined 2.3% over the same time frame.

Guidewire is a provider of software solutions for P&C insurers. Its cloud platform boasts a trusted infrastructure with modular and interconnected cloud services to aid insurers in upgrading their core operations. The platform has scalability as well as the ability to embed analytics and core workflows. The company updates its cloud platform thrice a year to keep the system agile and nimble amid a constantly evolving P&C industry.

Solid financial performance is driving a good run on the trading front. The company's earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, delivering an average surprise of 109.2%.

Since the last earnings announcement on Jun 4, its shares have surged 25.5%. The stock is still down 1.8% from its 52-week high level of $138.15.

Image Source: Zacks Investment Research

Factors Driving Growth

The focus on cloud strategy has been paying off for Guidewire, as evidenced by increasing sales. In the last reported quarter, the company's total revenues were $240.7 million, up 16% year over year. The revenues surpassed the Zacks Consensus Estimate by 4%. The uptick was driven by solid Tier-1 deal volume and increasing migration activity, especially in Asia Pacific.

Guidewire Cloud continued to gain momentum in the reported quarter with eight deal wins. Management highlighted that including the eight deal wins, InsuranceSuite cloud wins now stand at 24 for the year-to-date period, representing a 33% increase from the prior-year level. Guidewire's InsuranceSuite Cloud comprises three primary applications, namely PolicyCenter Cloud, BillingCenter Cloud and ClaimCenter Cloud.

The company's focus on enhancing the Guidewire Cloud platform with new capabilities is expected to boost sales of subscription-based solutions.

Subscription and support segment's revenues (57.3% of total revenues) soared 28% from the year-ago quarter to $138 million in the fiscal third quarter. As of Apr 30, annual recurring revenues were $828 million, up 14.7% year over year.

Management also remains focused on driving cloud operations efficiently to boost cloud margins. Subscription and support segment's gross margin increased to 65.5% from 55.1% on a year-over-year basis, attributed to increased cloud infrastructure efficiency.

The company keeps fostering and expanding its network of partners that includes SIs and solution providers to drive sustained activity and greater value from the platform.

Raised Guidance

Management raised its guidance for fiscal 2024 owing to strong pipeline activity. GWRE expects total revenues between $968 million and $976 million compared with the previous guidance of $957-$967 million. ARR is now expected to be in the range of $856-$864 million (previously projected range: $852-$862 million). Non-GAAP operating income is estimated between $94 million and $102 million.

Cash flow from operations is now anticipated in the range of $130-$150 million compared with the previous guidance of $120-$140 million.

Estimates Moving North

The Zacks Consensus Estimate for fiscal 2024 and 2025 revenues is pegged at $970.8 million and $1.08 billion, respectively, indicating growth of 7.2% and 11.6% from the year-ago levels.

The consensus estimate for fiscal 2024 and 2025 EPS is expected to rise 245.7% and 55%, respectively, from the prior-year actuals to $1.21 and $1.88.

The consensus mark for fiscal 2024 and 2025 EPS has increased 8% and 8.1%, respectively, in the past 60 days, reflecting analysts' optimism.

Headwinds Persists

Service revenues are getting affected as the company invests more in its ecosystem of implementation partners.

Rising research and development costs and integration risks are major concerns for this Zacks Rank #3 (Hold) company. In the last reported quarter, total operating expenses increased 1.4% year over year to $158.9 million.

Stocks to Consider

Some better-ranked stocks in the broader technology space are Alphabet GOOGL, Arista Networks ANET and Woodward WWD, each currently sporting a Zacks Rank #1 (Strong Buy).

The Zacks Consensus Estimate for Alphabet's 2024 EPS is pegged at $7.60, up 12.1% in the past 60 days. GOOGL's earnings beat the Zacks Consensus Estimate in each of the last four quarters, the average surprise being 11.3%. The long-term earnings growth rate is 17.5%. Shares of GOOGL have risen 43.4% in the past year.

The Zacks Consensus Estimate for Arista Network's 2024 EPS is pegged at $7.92, up 5.7% in the past 60 days. The long-term earnings growth rate is 15.7%. ANET's earnings beat the Zacks Consensus Estimate in each of the last four quarters, the average surprise being 15.4%. Shares of ANET have gained 121.9% in the past year.

The Zacks Consensus Estimate for Woodward's fiscal 2024 EPS has increased 11.6% in the past 60 days to $5.88. WWD's earnings beat the Zacks Consensus Estimate in each of the last four quarters, the average surprise being 26.1%. The long-term earnings growth rate is 16.5%. Shares of WWD have risen 59.1% in the past year.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.