Celanese Corporation CE is expected to benefit from its investments in high-return organic projects, cost and productivity actions and synergies of acquisitions. However, it faces headwinds from weak demand in certain end markets and pricing pressures.

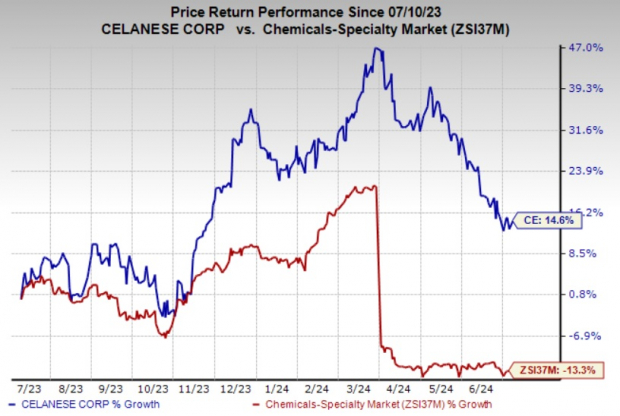

The company's shares have gained 14.6% in a year against a 13.3% decline of its industry.

Image Source: Zacks Investment Research

Let's find out why this Zacks Rank #3 (Hold) stock is worth retaining at the moment.

Acquisitions & Productivity Aid Celanese

Celanese's strategic acquisitions have provided it with opportunities for additional growth, investment and synergies. The acquisition of the majority of DuPont's Mobility & Materials ("M&M") business has allowed Celanese to enhance its growth in high-value applications. Celanese expects incremental M&M synergies of at least $150 million during 2024.

The acquisitions of SO.F.TER., Nilit and Omni Plastics are also expected to contribute to earnings expansion in the company's Engineered Materials segment. The Elotex acquisition also strengthened the company's position in the vinyl acetate ethylene emulsions space. Moreover, the purchase of Exxon Mobil's Santoprene business broadened the company's portfolio of engineered solutions and enabled it to offer a wider range of functionalized solutions to targeted growth areas, including future mobility, medical and sustainability.

Celanese also remains focused on executing its productivity programs including the implementation of several cost-reduction capital projects. Productivity actions are expected to support its margins in 2024.

The company is proactively implementing strategic initiatives recognizing the volatility and unpredictability of the current market landscape and competitive environment. These actions involve strengthening its commercial teams, aligning production and inventory levels with prevailing demand, implementing cost-saving measures and optimizing cash flow. These endeavors are expected to result in strong cash generation and a continuation of earnings growth.

Celanese has also completed the startup of a new 1.3-million-ton Clear Lake acetic acid expansion unit and a new vinyl acetate ethylene unit in Nanjing. It expects the Clear Lake expansion to contribute to higher earnings performance in the second quarter and into the second half of 2024.

Moreover, Celanese continues to generate strong cash flows and is focused on boosting shareholders' value and deleveraging its balance sheet. It generated a record operating cash flow of $1.9 billion and a free cash flow of $1.3 billion in 2023. CE returned $305 million to shareholders through dividend payouts during 2023. Moreover, the company reduced its net debt by $1.3 billion in 2023. It expects to continue reducing its net debt in 2024. The company, in its first-quarter call, said that it expects to repay over $2 billion in total debt maturities over the next four quarters.

Soft Demand & Pricing a Concern

CE is exposed to headwinds from demand softness in some of its end markets. It witnessed weak demand in several end markets and destocking in 2023. Soft demand led to inventory reduction and deferral of orders by the company's customers. Demand remains sluggish in industrial and consumer goods end markets. The company continues to see subdued demand in Europe. Demand conditions are yet to return to normal levels. Weaker demand recovery globally is likely to weigh on the company's volumes in the near term.

Celanese is also being challenged by significant competition. Competitive pressure is hurting its prices. CE saw lower pricing on a year-over-year basis across its segments in the first quarter. The company expects the pricing pressure to continue due to the challenging competitive dynamics in the second quarter of 2024.

Stocks to Consider

Better-ranked stocks in the basic materials space include Carpenter Technology Corporation CRS, Axalta Coating Systems Ltd. AXTA and Cabot Corporation CBT.

CRS beat the Zacks Consensus Estimate in three of the last four quarters while matching it once, with the average earnings surprise being 15.1%. The company's shares have soared roughly 93% in the past year. Carpenter Technology currently carries a Zacks Rank #1 (Strong Buy).

Axalta Coating Systems, carrying a Zacks Rank #2 (Buy), has a projected earnings growth rate of 26.8% for the current year. In the past 60 days, the consensus estimate for AXTA's current-year earnings has been revised upward by 5.9%. The company's shares have gained roughly 6% in the past year.

Cabot currently carries a Zacks Rank #2. CBT has a projected earnings growth rate of 26% for the current fiscal year. The company's shares have rallied around 33% in the past year.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.