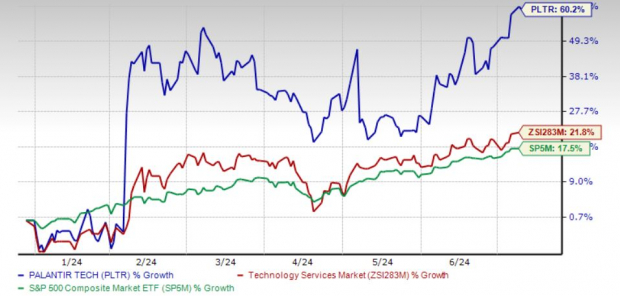

Shares of Palantir Technologies Inc. PLTR hit a 52-week high of $27.99 on Jul 8 before closing a tad lower at $27.7, up a whopping 61.3% year to date.

Since hosting its fourth AIP event on Jun 6, Palantir's shares have surged by 16.4%. This performance has significantly outpaced the 5% rise of its industry and the 4.3% increase of the Zacks S&P 500 composite. Interest in this prominent AI-focused stock remains strong, as investors seek opportunities to capitalize on the trend.

Year-to-Date Price Performance

Image Source: Zacks Investment Research

Similarly, other noteworthy AI stocks have experienced significant gains, reflecting the overall positive sentiment in the market. NVIDIA has risen 159% and SoundHound AI has rallied 98% year to date.

Given the continued strength in PLTR shares, investors might be tempted to buy the stock. But is this the right time to buy PLTR? Let's find out.

Artificial Intelligence Platform (AIP) & Bootcamps

Palantir's AI solutions play a crucial role in enhancing defense capabilities, especially amid rising geopolitical tensions. This is evident from its recent $480 million U.S. defense contract for its AI system, Maven. The company maintains a balanced revenue stream, with 55% coming from government contracts and 45% from commercial ventures. Palantir's expertise in AI-driven information warfare and cybersecurity positions it well for sustained growth as global security demands evolve.

Palantir's Gotham platform secures multiyear contracts from governments, contributing to steady double-digit sales growth and predictable cash flow. The company's unique AI integrations and product launches have been particularly well-received by its core government clients and its expanding enterprise customer base. In the first quarter of 2024, Palantir's government revenues increased 16% year over year, with U.S. government revenues improving 12%.

A notable trend for Palantir is its successful pivot from relying almost entirely on government contracts to making significant inroads into Corporate America. The U.S. commercial division's performance has been impressive, driven by AI-powered operating systems and boot camps as its primary market strategies. In the first quarter of 2024, commercial revenues rose 40% year over year, with total revenues increasing 21%. Additionally, the adjusted operating margin saw a substantial 1200 basis point growth compared to the previous year.

Healthy Returns on Capital

Return on equity (ROE), an indicator of profitability, shows how efficiently a company uses its shareholders' investments to generate earnings. PLTR's ROE was 19.3% at the end of the first quarter of 2024 compared with the industry's 6.1%.

Return on Equity

Image Source: Zacks Investment Research

PLTR has demonstrated effective investment in profitable areas, as reflected in its return on invested capital. The company's trailing 12-month ROIC is 7.8%, ahead of the industry average of 4.1%.

Return on Invested Capital

Image Source: Zacks Investment Research

Strong Top and Bottom-line Prospects

The Zacks Consensus Estimate for PLTR's 2024 earnings is pegged at 33 cents, indicating 32% growth from the year-ago level. Earnings in 2025 are expected to increase 20.8% from the prior-year actuals. The company's sales are expected to increase 21.6% and 21.2% year over year, respectively, in 2024 and 2025.

Stock Looking Pricey Amid AI Buzz

At its current valuation, Palantir is looking pricey. Based on EV-to-EBITDA, PLTR is currently trading at 275.1X, way above the industry's 58.44X. If we look at the Price/Earnings ratio, PLTR shares are currently trading at 75.99X forward earnings, well above the industry's 38.43X. Furthermore, the stock is currently trading above its 50-day moving average, with a relative strength index indicating that it is in the overbought zone.

Prospects High but Not a Right Time to Buy

Palantir's latest guidance suggests a 2.7% sequential increase in revenues for the second quarter of 2024, indicating a potential slowdown in business growth in the latter half of the year. Nevertheless, the company's agility in AI-led information warfare and cybersecurity continues to position it for sustained growth amidst evolving global security needs.

However, given the stock's current high valuation based on EV-to-EBITDA and Price/Earnings ratios and its position in the overbought zone, it might be prudent for investors to wait for a potential market correction before buying. Palantir remains fundamentally strong, but a better entry point could emerge if the stock undergoes some price adjustment.

PLTR currently carries a Zacks Rank #3 (Hold).

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.