The auto supplier base is a huge ecosystem from large to small; most of the public companies are the larger firms who have some good economies of scale. In my post about the potential General Motors IPO [Jun 16, 2010: What to Expect from a General Motors IPO], I mentioned how before the implosion of 2008 the unions had truly made some sea changes in their contracts both in terms of truly being able to fire people (rather than putting them in a room and paying them 90% of their wages), as well as a 2 tier pay system (new hires being paid just over what the average Walmart worker now gets). These companies have very levered models so with the dramatic cost cuts both now and those that should be rolling onto the books the next 5-10 years as the old guard retires, these companies are all quite interesting. (The supplier base already went to much lower wages in the blue collar far in advance of the Big 3 since competition is so much more cuththroat).

In a parallel sense the auto industry of 5-10 years ago was a lot like our local, state, and federal government is today - bloated and not adjusted to the new world order. . [Jan 24, 2010: For the First Time, More Union Workers Work in Government versus Private Sector] Since government can be run as a money losing operation (at least at federal level, and to some degree at the local level as federal government hands taxpayer money out as "stimulus") for apparently an infinite amount of years, we are still not seeing any true reform or adjustment in the public sphere. Certainly not when compared has happened in the auto sector where a wrenching period of adjustment has been happening not just the past 3 years, but the past 10 (ask a multitude of Midwest towns)

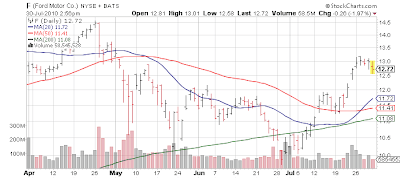

Hence these auto companies can now be profitable even with smaller revenue levels due to a far smaller labor base, with many employees paid far less than 5, 10 years ago....and many names in the sector are also benefiting from huge growth overseas in emerging markets. That should be a familiar theme by now across many industries - the main difference is other reasons i.e. global wage arbitrage (i.e. outsourcing) - is causing the lower labor costs in non automotive. Once again all these development are not so great for the American consumer or former middle class (many of which won't be able to ever buy a new cars at their new wages) but as the "cold hearted speculator class" who only cares about profits no matter what expense to a society (which is the hat we are forced to wear as a fund manager), believe it or not even at current levels of annual auto volume (which is about 70-75% of peak!) these companies are pumping out profits. We own BorgWarner (BWA) which reported today but many names that reported (including Ford) in this sector the past week have put up some impressive figures. See Tenneco (TEN) for an example.

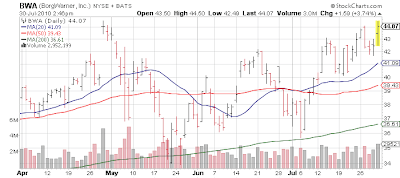

BWA is now approaching a retest of 52 week highs; I don't have a huge position due to earnings and taking some profits earlier in the month, but if I had a larger position what I would do is take another round of profits here and then buy back if the stock can show enough strength to clear the old high. Otherwise, buying on a pullback to support works. Since my position is not very big I am just going to keep what I have and add once I see how the stock and the general market acts in the weeks ahead.

Obviously despite the ability to mint money at far lower volumes than in the past, this industry is still cyclical and if the next leg of the Great Recession is a deep dive, these companies will suffer but I think instead we are just going to have years of malaise (the "square root" economy rather than V's, W's, U's)- until/when fears of sovereign debt levels strike at one of the big 3: Japan, UK, USA.

A quick look at earnings and the 11 cent beat.

[May 10, 2010: Beginning Stake in BorgWarner]

[Jun 15, 2010: Morgan Stanley & UBS Upgrade Auto Sector; Including BorgWarner]

Long BorgWarner in fund; no personal position

Market News and Data brought to you by Benzinga APIsIn a parallel sense the auto industry of 5-10 years ago was a lot like our local, state, and federal government is today - bloated and not adjusted to the new world order. . [Jan 24, 2010: For the First Time, More Union Workers Work in Government versus Private Sector] Since government can be run as a money losing operation (at least at federal level, and to some degree at the local level as federal government hands taxpayer money out as "stimulus") for apparently an infinite amount of years, we are still not seeing any true reform or adjustment in the public sphere. Certainly not when compared has happened in the auto sector where a wrenching period of adjustment has been happening not just the past 3 years, but the past 10 (ask a multitude of Midwest towns)

Hence these auto companies can now be profitable even with smaller revenue levels due to a far smaller labor base, with many employees paid far less than 5, 10 years ago....and many names in the sector are also benefiting from huge growth overseas in emerging markets. That should be a familiar theme by now across many industries - the main difference is other reasons i.e. global wage arbitrage (i.e. outsourcing) - is causing the lower labor costs in non automotive. Once again all these development are not so great for the American consumer or former middle class (many of which won't be able to ever buy a new cars at their new wages) but as the "cold hearted speculator class" who only cares about profits no matter what expense to a society (which is the hat we are forced to wear as a fund manager), believe it or not even at current levels of annual auto volume (which is about 70-75% of peak!) these companies are pumping out profits. We own BorgWarner (BWA) which reported today but many names that reported (including Ford) in this sector the past week have put up some impressive figures. See Tenneco (TEN) for an example.

BWA is now approaching a retest of 52 week highs; I don't have a huge position due to earnings and taking some profits earlier in the month, but if I had a larger position what I would do is take another round of profits here and then buy back if the stock can show enough strength to clear the old high. Otherwise, buying on a pullback to support works. Since my position is not very big I am just going to keep what I have and add once I see how the stock and the general market acts in the weeks ahead.

Obviously despite the ability to mint money at far lower volumes than in the past, this industry is still cyclical and if the next leg of the Great Recession is a deep dive, these companies will suffer but I think instead we are just going to have years of malaise (the "square root" economy rather than V's, W's, U's)- until/when fears of sovereign debt levels strike at one of the big 3: Japan, UK, USA.

A quick look at earnings and the 11 cent beat.

- Auto parts maker BorgWarner Inc (BWA) posted stronger-than-expected quarterly earnings on Friday and raised its full-year earnings forecast due to stronger vehicle production in North America, Europe and China.

- BorgWarner, which produces turbochargers, transmission components and other parts, said it expects its growth to outpace the market overall and for company record earnings for the year.

- The auto parts maker reported net income of $82.8 million, or 68 cents per share, in the second quarter, compared with a net loss of $35.9 million, or a loss of 31 cents per share, a year earlier. Excluding nonrecurring items, BorgWarner earned 78 cents per share.

- Sales rose to $1.42 billion in the quarter from $916.2 million a year earlier. (+55%) BorgWarner said it expected sales to rise 32 percent to 35 percent in 2010 from last year.

- Analysts on average expected it to earn 67 cents per share on that basis, according to Thomson Reuters I/B/E/S.

- A "volume shift in Europe toward vehicles with higher BorgWarner content, including diesels, also boosted results," Chief Executive Timothy Manganello said in a statement.

- BorgWarner raised its 2010 earnings forecast to a range of $2.60 per share to $2.80 per share, from a prior forecast for $2.20 to $2.50 per share.

- Analysts expect $2.42 per share.

[May 10, 2010: Beginning Stake in BorgWarner]

[Jun 15, 2010: Morgan Stanley & UBS Upgrade Auto Sector; Including BorgWarner]

Long BorgWarner in fund; no personal position

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In: Auto Parts & EquipmentConsumer Discretionary

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in