Shares of the real estate investment trust Annaly Capital NLY slid to their lowest price in 14 years on Monday. Despite the abysmal long term performance of this REIT, nearly 32,000 Seeking Alpha readers are signed up to receive updates on it, and it’s probably been the subject of more Seeking Alpha articles than any sub-$10 billion market cap name. So why have so many moths been lured to this particular flame? In a word, yield. As of Monday’s close, Yahoo! Finance calculated a forward dividend yield of 11.9% for NLY. Slim consolation for NLY shareholders down 28% over the last 52 weeks though.

Annaly highlights a hazard of investing for yield. Securities with high yields often have those high yields because their prices have declined, for reasons that will continue to put downward pressure on their prices. Had Annaly longs simply put their money in the SPDR S&P 500 ETF SPY, they would have had a yield of only about 2%, but they’d be up about 19% over the last 52 weeks. Money is money, and investors with appreciated securities can always harvest some capital gains in addition to, or in lieu of collecting dividends. Nevertheless, for investors who would rather continue to hold NLY, here are a couple of ways of hedging it.

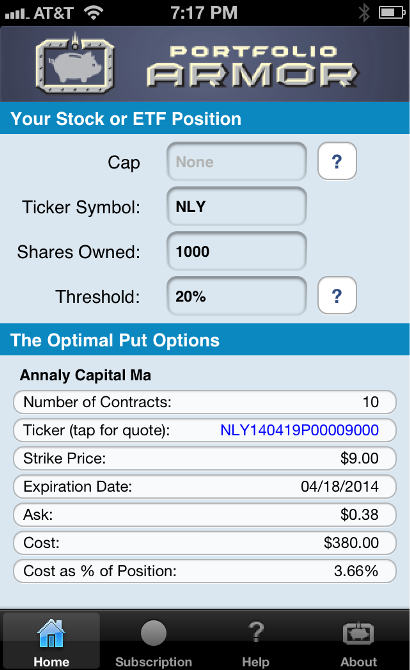

1) Hedging With Optimal Puts

Higher cost. Uncapped upside.

These were the optimal puts*, as of Monday’s close, to hedge 1000 shares of NLY against a greater-than-20% drop between now and April 18th.

As you can see at the bottom of the screen capture below, the cost of this protection, as a percentage of position value, was 3.66%.

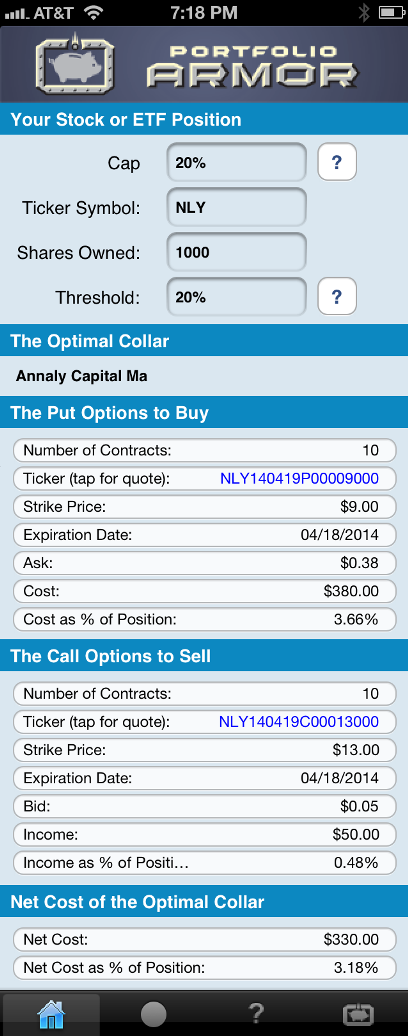

2) Hedging With An Optimal Collar

Slightly lower cost. 20% upside cap.

If you were willing to cap your potential upside at 20% between now and April 18th, this was the optimal collar** to hedge 1000 shares of NLY against a greater-than-20% drop over the same time frame.

As you can see at the bottom of the screen capture above, the net cost of this collar, as a percentage of position value, was only slightly lower at 3.18%. Recall that we saw a much larger reduction in cost from hedging with an optimal collar in this post on Celldex Pharmaceuticals CLDX recently. The reason there is relatively little cost savings with a collar in the case of NLY is that there is a lot less demand for out of the money calls on NLY. And there’s less demand for them because options market participants don’t see as much possibility of NLY climbing 20% over the next several months.

Note that, to be conservative, Portfolio Armor calculated the cost of this hedge by using the bid price of the call leg and the ask price of the put leg. In practice, you can often sell calls for more (at some price between the bid and ask) and buy puts for less (again, at some price between the bid and ask), so, in actuality, an investor opening the optimal collar above may have paid less than 3.18% to do so.

Possibly More Protection Than Promised

In some cases, hedges such as the ones above can provide more protection than promised. For a recent example of that, see this post about hedging shares of Tesla Motors, Inc. TSLA.

*Optimal puts are the ones that will give you the level of protection you want at the lowest possible cost. Portfolio Armor uses an algorithm developed by a finance PhD to sort through and analyze all of the available puts for your stocks and ETFs, scanning for the optimal ones.

**Optimal collars are the ones that will give you the level of protection you want at the lowest net cost, while not limiting your potential upside by more than you specify. The algorithm to scan for optimal collars was developed in conjunction with a post-doctoral fellow in the financial engineering department at Princeton University. The screen captures above come from the Portfolio Armor iOS app.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.