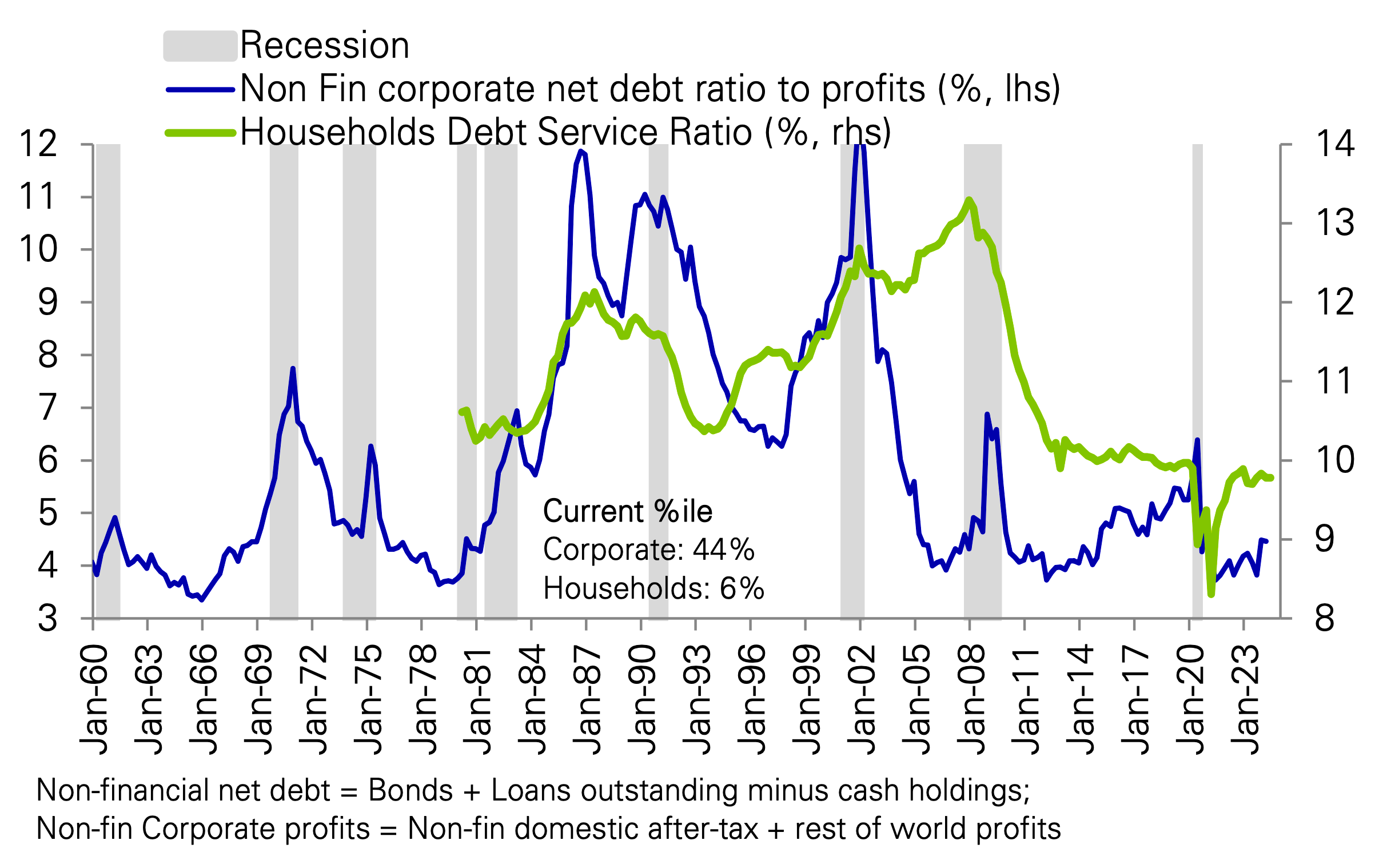

Consumer And Business Finances Are Healthy

The customers in the economy have the capacity to spend, which means economic activity should keep churning.

“As is well known, household and corporate balance sheets are strong,” Deutsche Bank’s Binky Chadha wrote in a Sept. 12 note. “This is very different from past down cycles.“

Consumer and business finances are healthy. (Source: Deutsche Bank)

You’ll continue to read unsettling news headlines about how the absolute levels of debt are historically high. But what actually matters is how that debt measures relative to the capacity to service that debt, which is historically strong.

And by the way, even though sentiment surveys suggest consumers and business managers are more pessimistic than usual, the hard data confirm that they all continue to spend — probably because they have the financial capacity to do so.

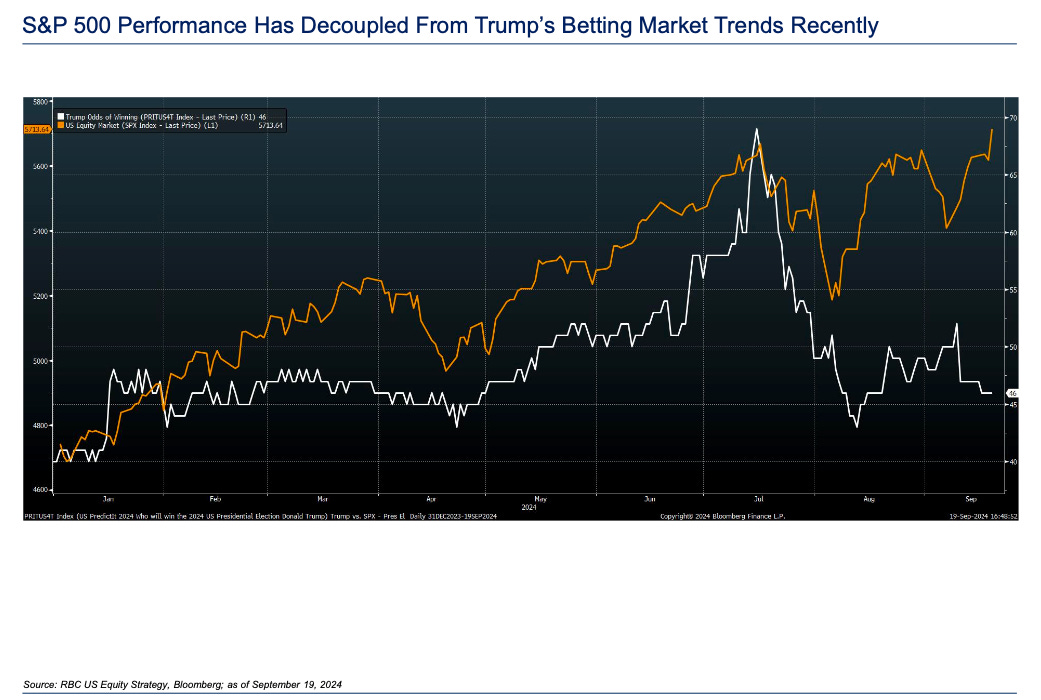

The Stock Market Decouples From Trump

It’s not uncommon to hear people argue that Donald Trump’s policy platform would be more favorable for the stock market than his Democrat opponent. Indeed, for a while it seemed that the stock market would move higher as Trump’s odds of winning the November presidential election improved.

“This relationship has broken down recently,” RBC’s Lori Calvasina observed in her September 23 research note.

Stocks have continued to rally even as Trump’s election odds have fallen. (Source: RBC)

This type of divergence isn’t totally unprecedented. For example, history shows that even amid corporate tax reform that led to higher tax rates, corporations eventually figured out how to grow earnings. And their stock prices followed suit.

Just because the person who ends up in the White House may be less business friendly than their opponent doesn’t mean that businesses will fail to grow earnings.

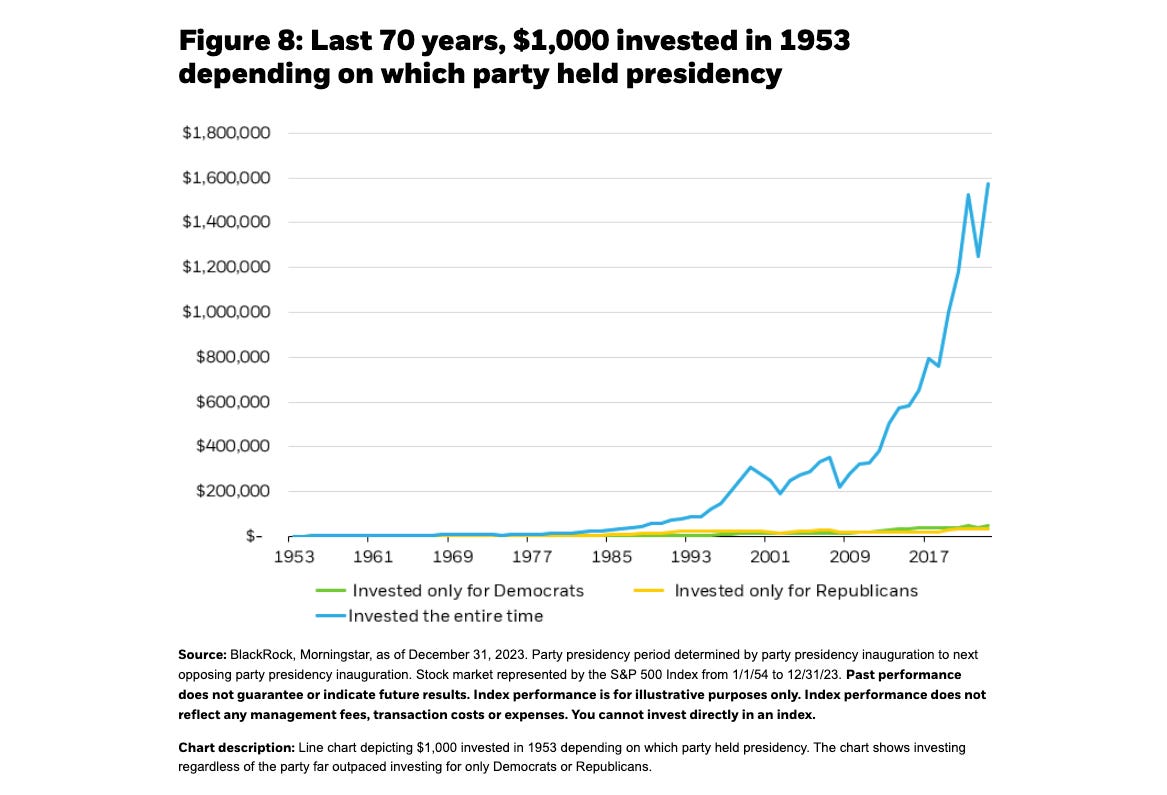

Compound Interest Is More Powerful Than Any Political Party

An investor who only invested in the stock market when a Democrat was president has done marginally better than the investor who only invested when a Republican was president.

However, both got totally smoked by the investor who stayed invested regardless of who occupied the White House. From BlackRock’s Gargi Chaudhuri: “At the index level, staying invested has been more important than which party wins the presidency. Investors who held the course as political winds changed earned nearly double those who shifted their strategy based on the election in the last decade — a trend only magnified over the very long term.”

Staying invested is more important than which party wins the presidency. (Source: BlackRock)

This is a reminder that time in the market beats timing the market. You don’t want to miss out on the incredible wealth generating power of compound interest.

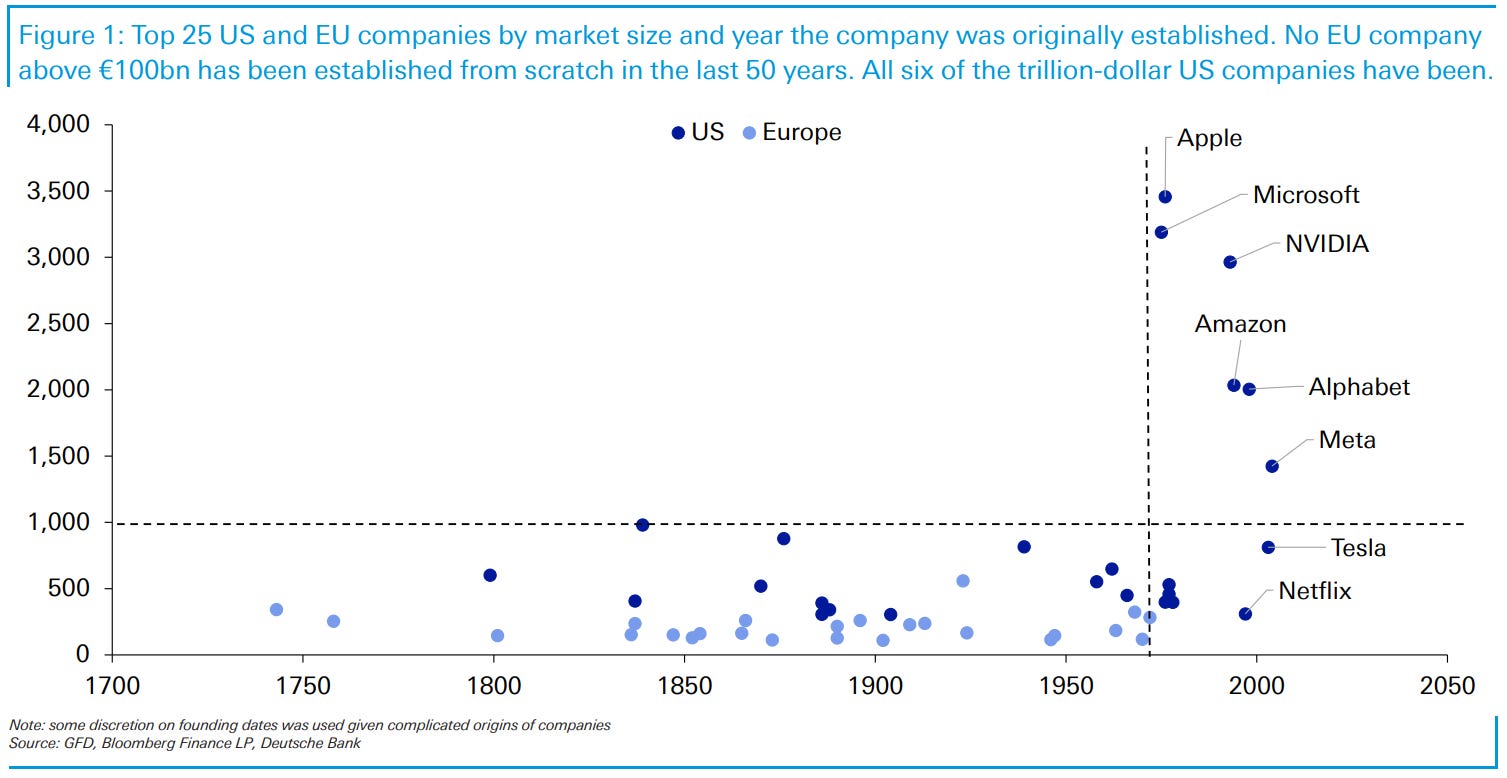

U.S. Companies Are Crushing It

Teeing off Mario Draghi’s controversial paper on European competitiveness, Deutsche Bank’s Jim Reid shared an interesting observation about U.S. vs. European companies in his Chart of the Day on Wednesday. From his note (emphasis added):

Earlier this month, Mario Draghi’s long-awaited report on European Union competitiveness contained an abundance of recommendations for the continent, including how it needed to spend up to €800bn extra a year to become more competitive with the US and China. Buried in the report was a fascinating line that said “...there is no EU company with a market capitalisation over €100 billion that has been set up from scratch in the last fifty years, while all six US companies with a valuation above €1 trillion have been created in this period.” … I thought it would be worth graphically representing Draghi’s point. Today’s CoTD shows the top 25 companies by size in the S&P 500 and Stoxx 600 against the year the companies' origins can be traced. There is some nuance here. For example, ASML is the third largest EU company and although it was incorporated in 1984, it emerged from a joint venture out of ASM (1968) and Phillips (1891). So the company wasn’t started from scratch within the last 50 years.“

There’s no EU company that was created in the past 50 years that’s worth more than €100 billion. (Source: Deutsche Bank)

As I wrote in the April 21 TKer: “There’s clearly something special going on right now in the U.S. that helps explain why its stock market has performed so well on the global stage. Maybe it’s the culture of innovation. Maybe it’s the business-friendly regulation. Maybe it’s the relatively strong corporate governance practices. Maybe it’s how shareholders incentivize company executives and employees. Whatever it is, it’s helping to drive earnings higher. As a result, investing in the U.S. stock market has been a winning trade for a long time, and there’s little reason to believe it won’t continue to be in the years to come.“

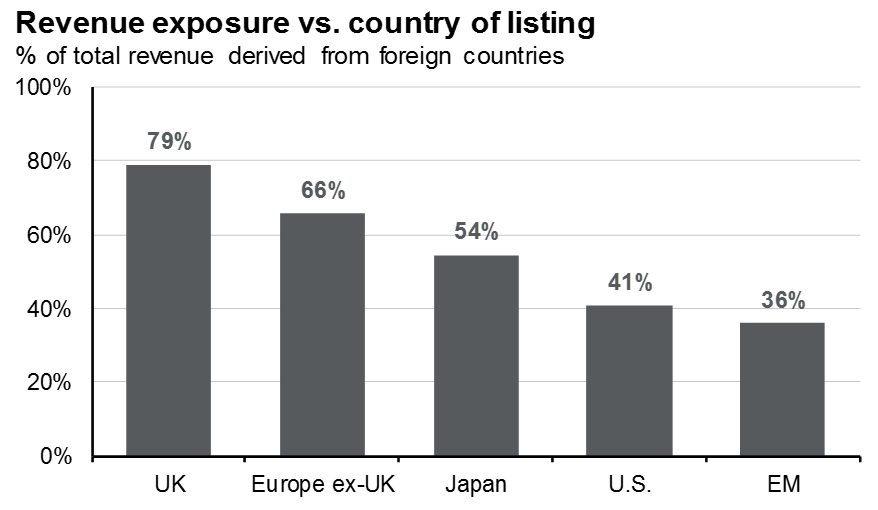

There Are No Borders In Business

Sure, U.S. companies probably benefit from operating in the largest economy in the world. But if you’re a big company, then you probably do at least some business outside of your home country.

In fact, as this chart from JPMorgan shows, publicly traded companies in the U.K., Europe, and Japan generate most of their revenue abroad.

Publicly traded companies in the U.K., Europe, and Japan generate most of their revenue abroad. (Source: JPMorgan)

This is a reminder that you don’t necessarily have to buy stocks outside of your home country to get foreign exposure. If you want exposure to foreign forms of management and corporate governance, that’s another story.

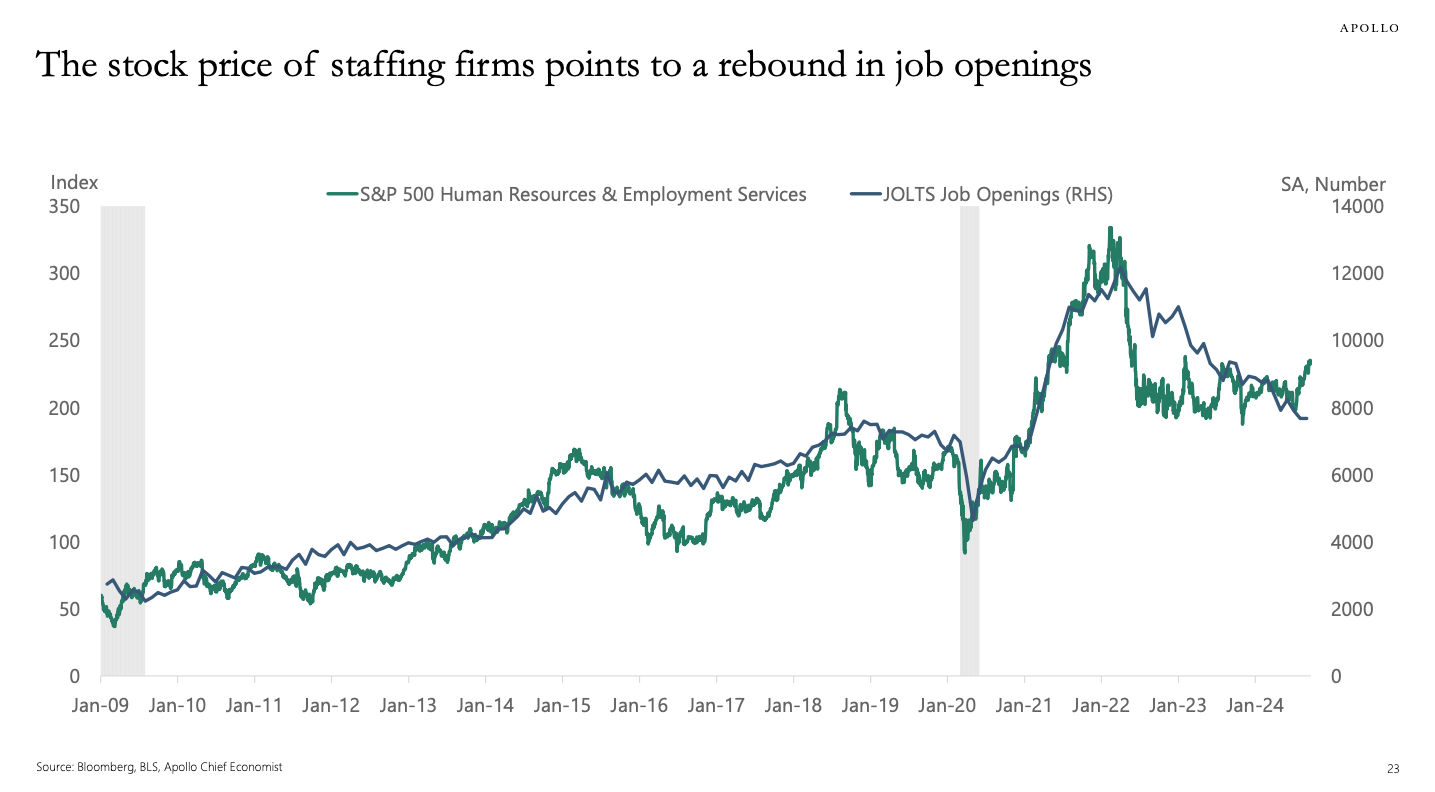

Are More Job Openings Coming?

The labor market has been cooling. Notably, the once massive tailwind of excess job openings has faded.

But are we about to get a rebound in job openings?

“The stock price of staffing firms points to a rebound in job openings,” Apollo’s Torsten Slok wrote in his chartbook shared on September 21.

HR industry stocks suggest job openings could rise. (Source: Apollo)

I can’t say this is the most compelling case for a recovery in job openings. After all, it’s just one metric, and it’s up against a lot of data that point to a labor market slowdown.

But who knows? Maybe this recent rate cut from the Fed will spark another labor market boom.

For more, read: A once massive economic tailwind has faded 💨 and The labor market is cooling 💼

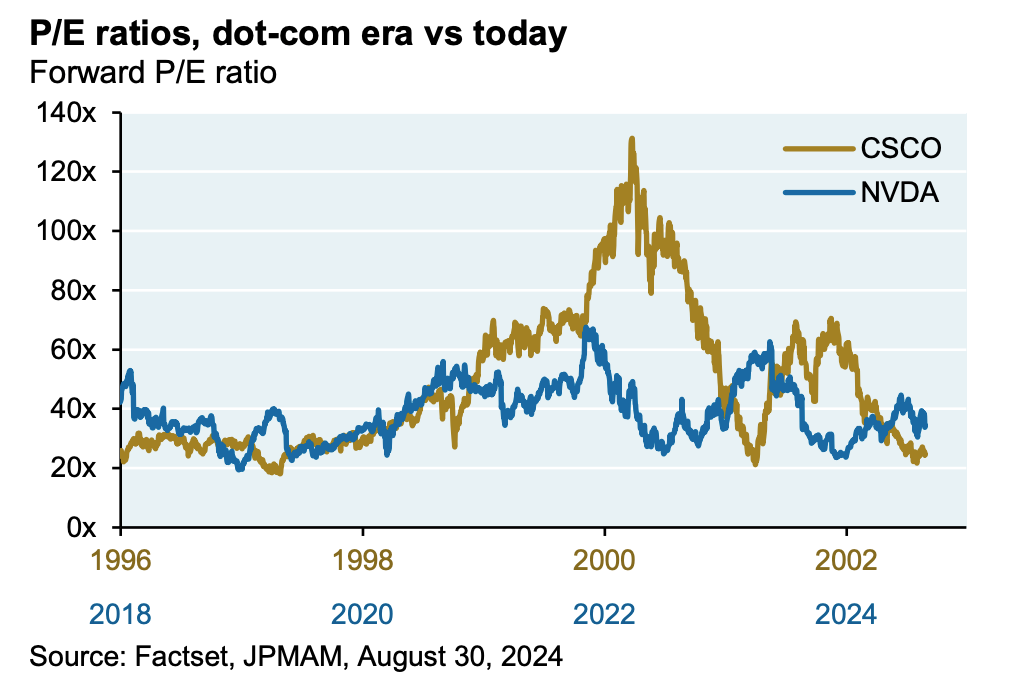

Nvidia Is No Cisco

Every once in a while, you’ll hear someone compare today’s AI boom to yesterday’s Dotcom bubble. And sometimes, people will argue this by comparing the current trajectory of Nvidia’s (NASDAQ:NVDA) stock price to that of Cisco (NASDAQ:CSCO) back in the day.

One thing to note about the AI boom is that there’s tangible demand for the technology. And that’s translating into meaningful earnings growth for companies like Nvidia. And those earnings have made for a more palatable valuation story.

“Nvidia bears no resemblance to dot-com market leaders like Cisco (see below) whose P/E multiple also soared but without earnings to go with it,” JPMorgan’s Michael Cembalest observed in his September 3 note.

Nvidia’s valuation doesn’t appear as stretched as Cisco’s during the dotcom bubble. (Source: JPMorgan)

Analysts across industry groups see AI technology boosting profit margins for the companies they cover. Unfortunately, we’ll only know in hindsight if AI delivers all that we hope for.

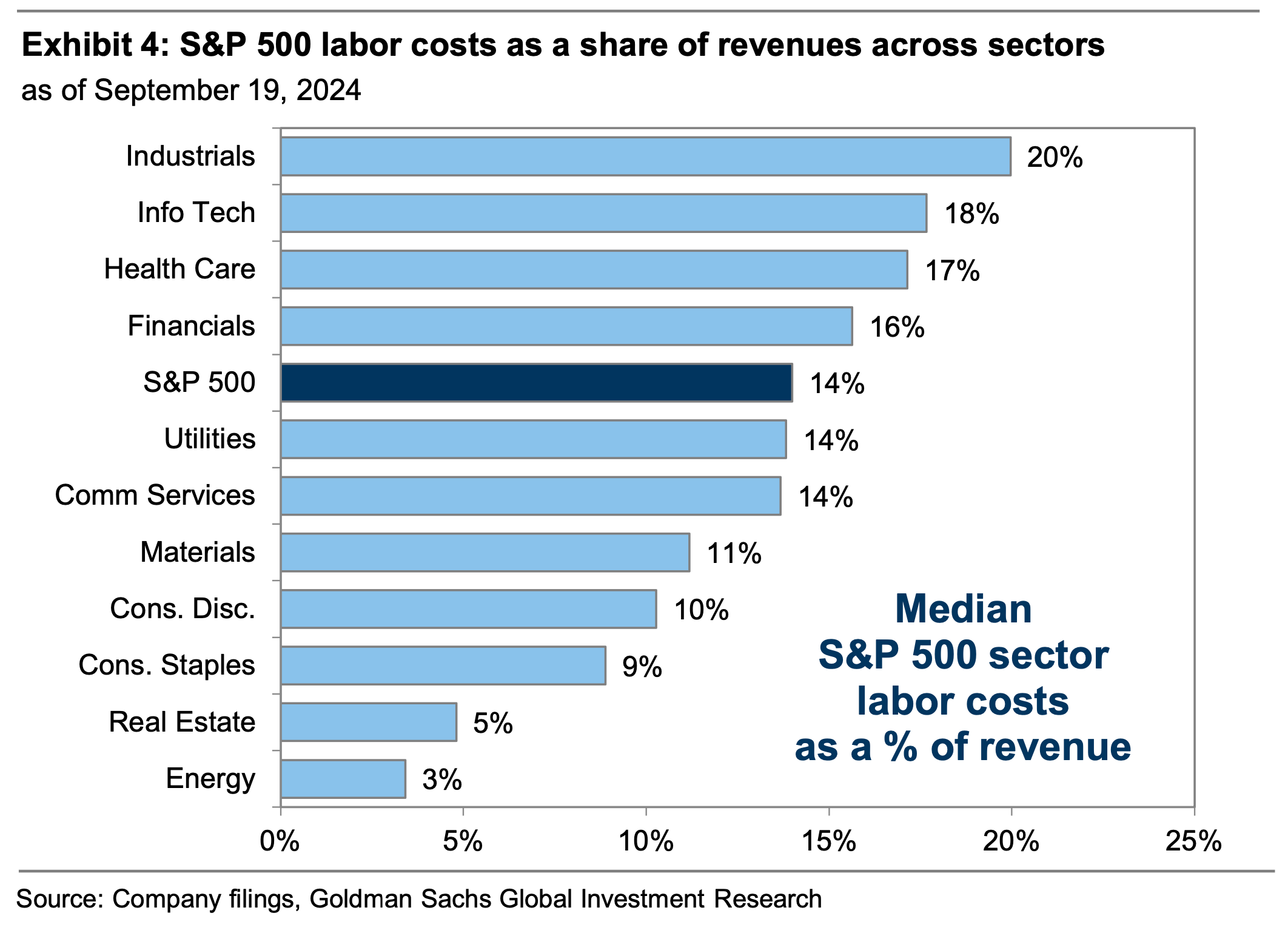

What Labor Costs Look Like Across Industries

Every industry is unique in terms of how much it costs to staff a company to keep operations running. This is important to understand when analyzing the impact of changes in wage costs.

“Our analysis of the latest company filings reveals that S&P 500 labor costs equal 12% of total revenues for the aggregate index and 14% of revenues for the median stock,” Goldman Sachs’ David Kostin wrote in his September 20 note. “Exposure to labor costs vary at the sector level, from 20% in Industrials to 3% in Energy.”

Exposure to labor costs vary across sectors. (Source: Goldman Sachs)

The Bottom Line

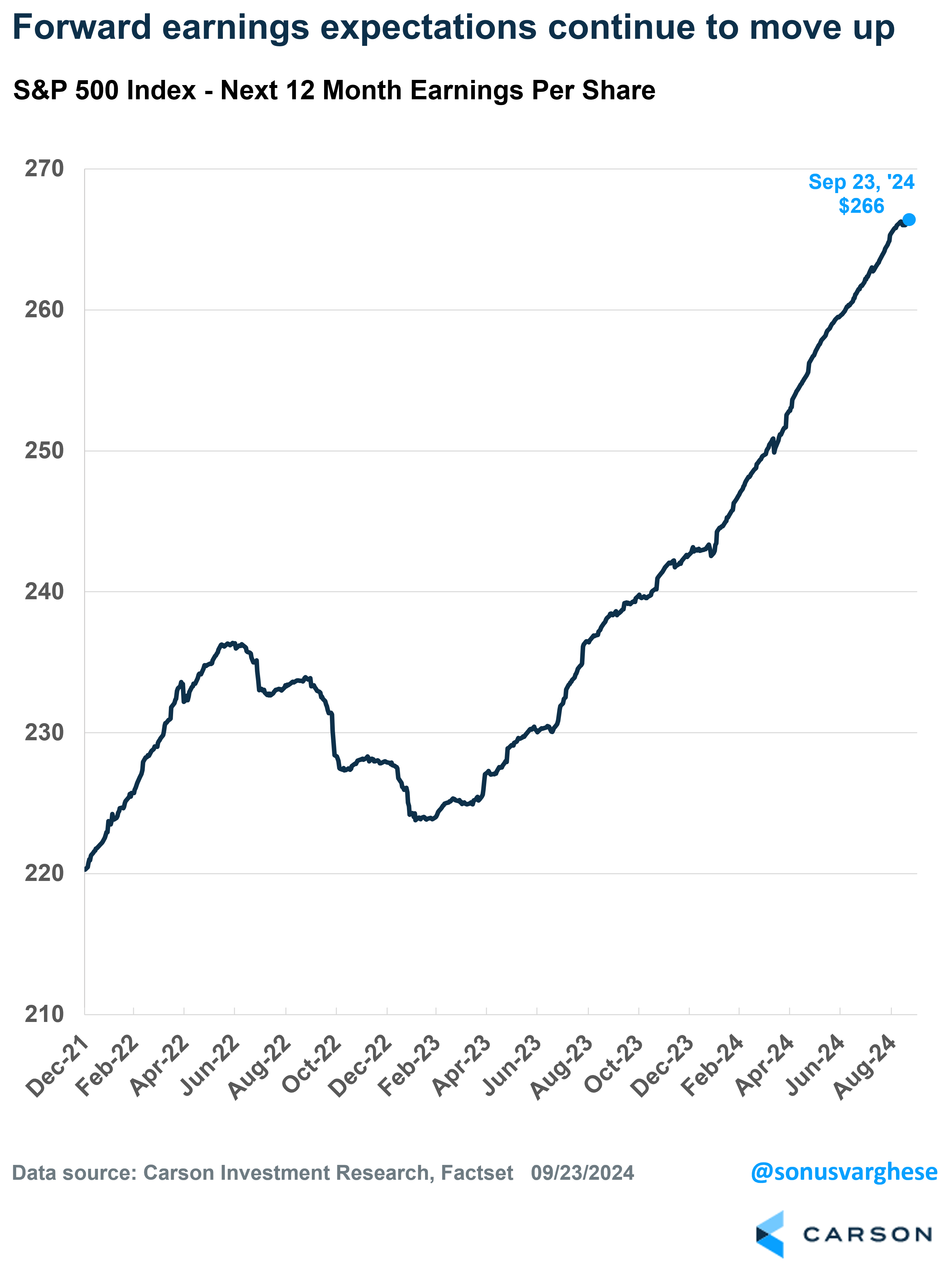

“The good news is that profit expectations continue to rise,” Carson Group’s Sonu Varghese wrote on Wednesday. “Expected earnings per share for the S&P 500 over the next 12 months is now at $266, about 10% higher than it was at the end of last year.”

The outlook for earnings is looking up. (Source: Carson Group)

“As our friend Sam Ro (who writes the TKer Substack), says, earnings are the most important driver of stock prices,” he added.

I couldn’t have said it better myself!

A version of this post was originally published on Tker.co.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.