The International Monetary Fund (IMF) stress tested 53 large banking holding companies and published its findings last month. The report concluded that despite restoration of some stability, there remain certain important risks to the U.S. financial system and economy mainly coming from the real estate sectors:

- Further increases in nonperforming loans due to high unemployment rate and significant weakness in the real estate sectors

- Credit quality in the commercial real estate (CRE) sector - About $1.4 trillion of CRE loans will mature in 2010–14, nearly half of which are 90 days or more past due or “underwater.”

- Housing prices - The very high level of underwater mortgages increases the risk of strategic defaults and further losses to banks and mortgage backed security (MBS) investors.

IMF noted financial institutions will face rollover risks with large loan maturities in 2011–13, which could bring rapidly rising foreclosures and bank losses. The small and medium-sized banks, which are most heavily exposed to the commercial real estate sector, are causing the most concern.

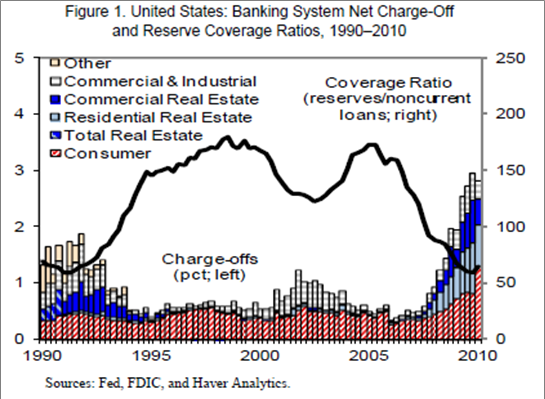

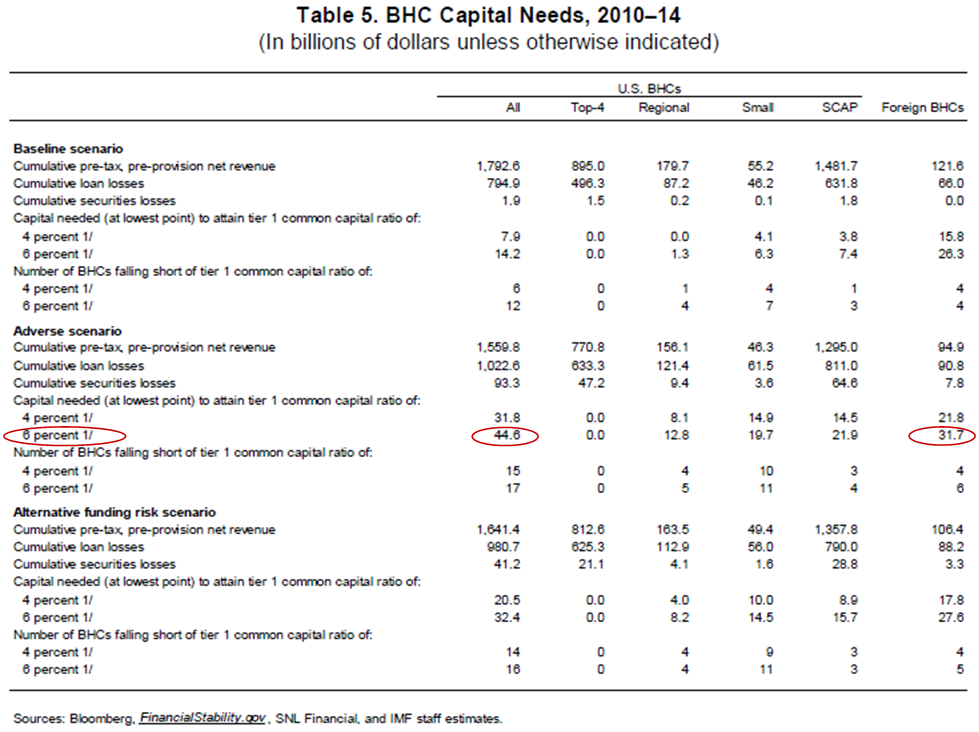

Since bank balance sheets remain fragile and under-capitalized (Figure 1), under an “adverse scenario”, small and regional banks as well as subsidiaries of foreign banks would incur $1.113 trillion of cumulative loan losses from 2010 to 2015 and need as much as $76.3 billion (i.e. a TARP 2.0), additional capital to meet a tier one ratio of 6% .

Under the “baseline scenario”, cumulative loan losses would have been $860.9 billion, and need $40.5 billion additional capital. (See table)

IMF also noted the securitization market could become a drag on the economic recovery:

“Almost all of the recent issuance of U.S. private label MBSs has comprised re-securitizations of formerly “AAA” senior securities (so-called “re-remics”), with the Fed’s TALF responsible for much of the 2009 issuance of other asset backed securities (ABSs).”And to make things even more depressing, IMF warned that

“The economy and some key financial markets continue to depend heavily on fiscal, monetary, and financial policy support, and the output gap is expected to remain wide for many years.”Other research reports also paint an equally gloomy picture. According to an analysis by Realpoint, reported by HousingWire, delinquencies in commercial mortgage -backed securities (CMBS) in the US increased to 7.2%, and more than triple the rate a year ago. In May, the total delinquent unpaid balance for these loans reached $57.3 billion.

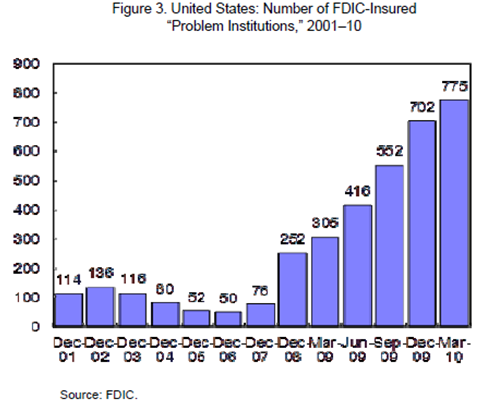

Realpoint forecasts by the end of 2010, the total amount of unpaid principal balance could grow between $80 billion and $90 billion, and the delinquency rate could reach as high as 12%. Earlier in the year, Trepp reported that these spiking delinquencies could cause bank failures to increase as much as 30% in 2010 (You think we don’t have enough problem banks bankrupting FDIC already? see Figure 3)

With the easy year-over-year earnings beat coming to an end, the best of the earnings may have already come to pass. As such, now would be a good time to take some profit off the table for another day, another entry point.

(Note: The full IMF report is available here.)

Dian L. Chu, Aug. 4, 2010

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Posted In:

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in