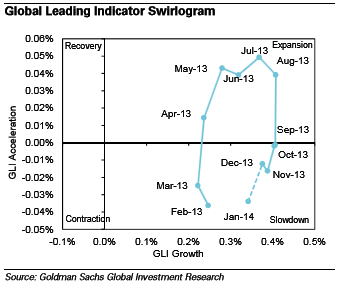

George Cole and his team at Goldman Sachs GS release monthly research notes regarding the firm's Global Leading Indicator. April's note showcased the expectation for further economic expansion based off data compiled from May.

Shortly thereafter, Goldman's trade desk issued a price target on the S&P 500 for 2014 of $2,000 in a separate note, which seemed interesting given the timing of the change alongside the choice of words used in the GLI notes.

With the S&P 500 pushing all-time highs and continuing to approach the target established by Goldman's sales and trading desk, a look back at the headline commentary in the firm's notes will show George Cole's original worry has slowly been replaced with more positive talk.

Related Link: S&P 500 Constituent Earnings Update

January:

"More signs of a mild slowdown"

February:

"A modest but broad-based Slowdown"

March:

"On the cusp of Expansion"

April:

"Another month on the cusp of Expansion"

Since weather appears to be the consensus excuse for weak economic data coming out of the winter season, there appears to be limited reason for the momentum from the Fed's actions to wear off anytime soon, especially as one of Wall Street's oldest banks has changed its opinion. Note that in the charts the percent changes; Goldman has changed its view drastically as the Momentum Indicator fell 50 basis points and the Acceleration Indicator swung 10 basis points.

Regardless of how high the markets go, once the Fed is removed as the dominant force in the market through FRBNY's POMO, it is unlikely that the buying power being unleashed to keep rates low (which is driving the housing market rebound) will be replaced.

The euphoria of the past five-year bull market has also manifest itself in the ETF market. There are now ETFs that have cleared regulatory hurdles that will consist of baskets of CDSs (credit-default swap), the same assets that have been blamed for the wide-spread collapse in global asset prices in 2008. Along with this, there is also a red hot M&A market fed by Covenant-Lite loans (meaning loans with lesser restrictions regarding investor accreditation).

This leads one to question the quality of the post-2008 economic turnaround. Looking at the quality of the headline data, the relaxation of standards for issuing leveraged loans and the flood of money into alternative assets (away from traditional equity and bond markets) paints a picture similar to that of 2006.

There seems to be a national view that things are great because home prices are up, stock markets are up, borrowing is easy and unemployment is down. This brings to question the resilience of the markets once the Fed removes itself.

All it may take for Goldman to turn bearish on the GLI is a few basis point fall in Acceleration and Momentum. This speaks volumes to the investment bank's belief in this market's quality of health as the end of the quantitative easing approaches.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.