Last time covered the "technical divergences" evident in the current market from a big-picture standpoint.

The Dow, S&P, NASDAQ, Russell 2000 and S&P 400 Midcap were compared in order to see if the major indices were all singing the same song. Note that in a strong market, "the generals" tend to lead the market and "the troops" follow along.

In the review of the charts, it was found that the Dow is in good shape and that the S&P 500 has largely confirmed the Dow's move to new highs. Note that the NASDAQ appears to be diverging from a near-term perspective.

It was then found that the mid-caps were also diverging, but not nearly to the same degree as the small-caps. And finally, it was discovered that the most glaring divergence can be seen in the Russell 2000, which is still suffering from this Spring's "momentum meltdown" (see below).

Russell 2000 Small-Cap - Daily

What Do The Sectors Say?

Since there are obviously divergences in the major indices, next up is a review of the charts of the important S&P sectors.

Dow Jones Transports Index - Daily

The chart of the Transports index suggests three things. First, that the economy must be doing okay as it appears that the companies moving "stuff" around the country are doing well.

Second, the new high in the Transports index confirms the move seen in the DJIA.

Third, the confirmation of new highs between the DJ Industrials and Transport indices means the venerable Dow Theory remains on a buy signal. This is considered the granddaddy of confirmation indicators and therefore, the analysts using this approach see the market in a healthy advance at this time.

Technology Select SPDR XLK - Daily

From a longer-term perspective, the chart of the technology sector appears to be fairly strong. It is true that the sector SPDR for technology is one day removed from a high. However, the momentum of the sector appears to have stalled out over the last month. Since tech is generally a key leader in the market, this is definitely something to watch.

Financial Select SPDR XLF - Daily

The chart of the financial sector, while also just off its recent high, is not as strong as the chart of the tech sector. Put simply, the action in the financial sector has been much choppier this year. It has been the recent strength in companies such as Goldman Sachs GS that has pushed this sector higher.

Until just recently, the financials had looked like a laggard.

From the "it is what it is" point of view, this sector appears to confirm the recent highs by the "Generals."

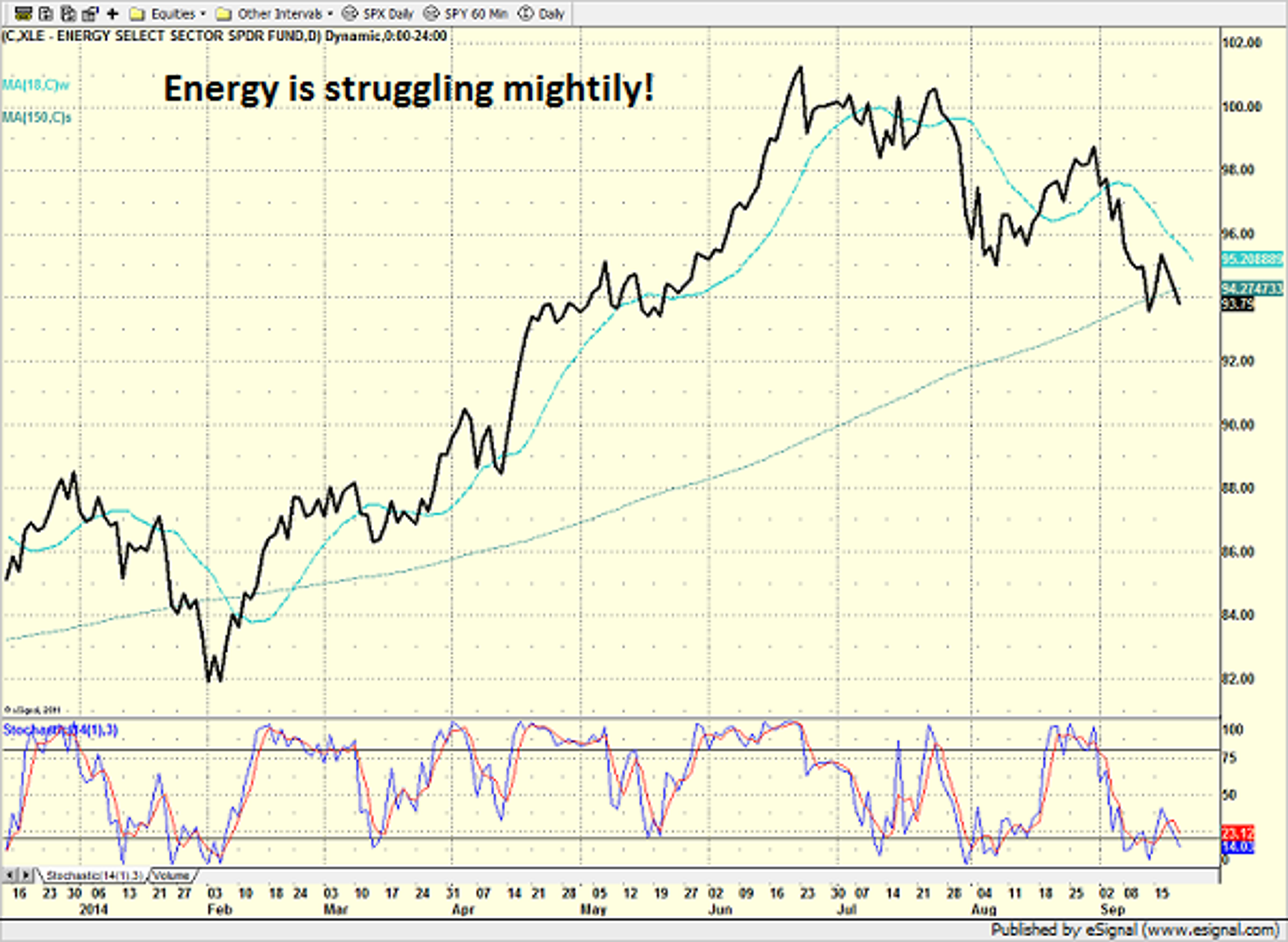

Energy Select SPDR XLE - Daily

The energy sector is another prime example of a technical divergence. The bottom line here is that energy has been moving lower since June, while the major indices have been moving up.

To be sure, the move lower in energy can be attributed largely to the recent rally in the dollar. However, in this exercise, a divergence is a divergence.

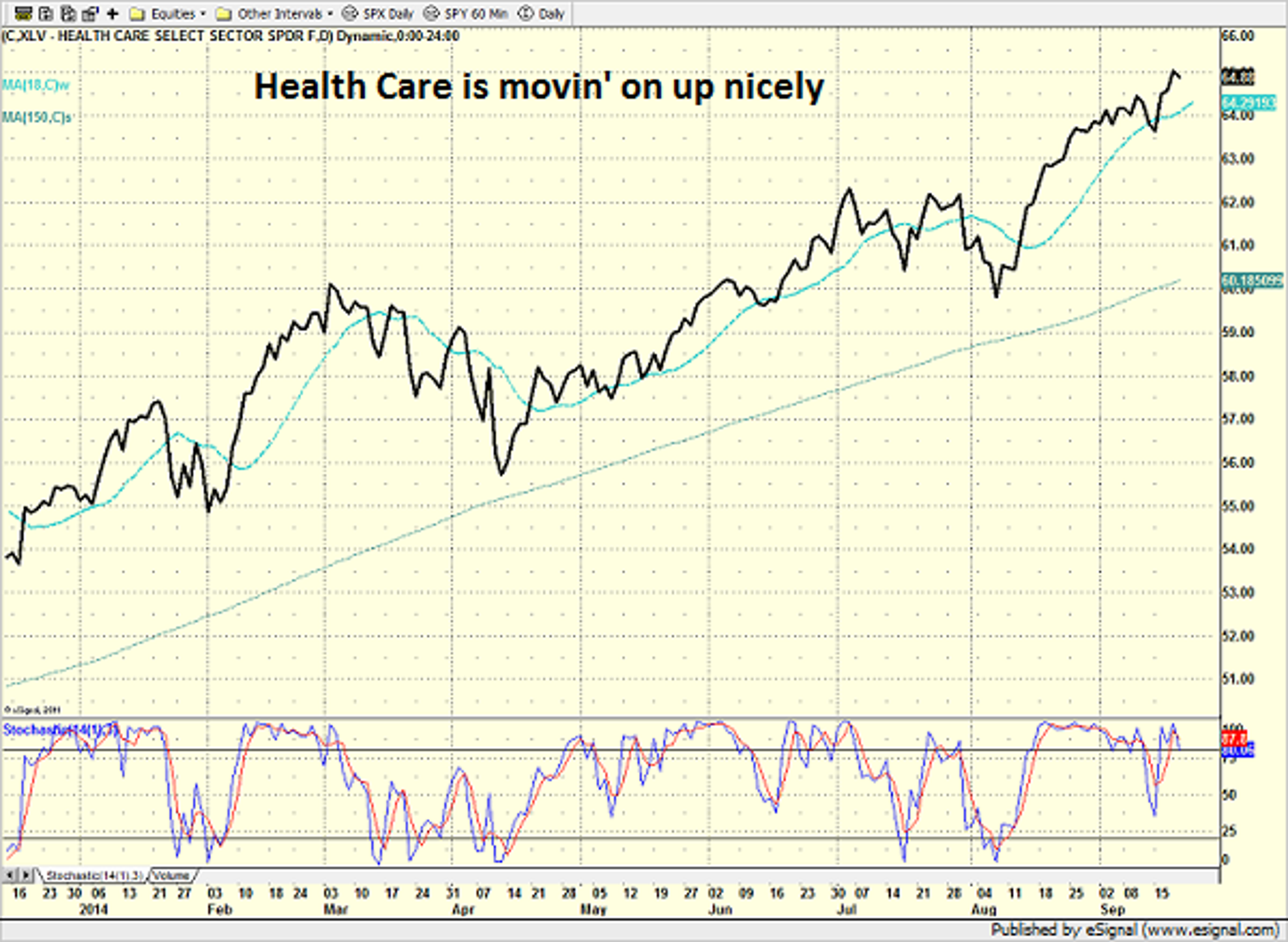

Health Care Select SPDR XLV - Daily

Next up is health care, and there is nothing at all to complain about here. The sector has benefited handsomely from the runs in pharmaceuticals and biotechnology, and the XLV is currently almost double the levels seen in 2007 and 2008. This one clearly goes in the "confirmation" category.

Now let's turn attention to the consumer.

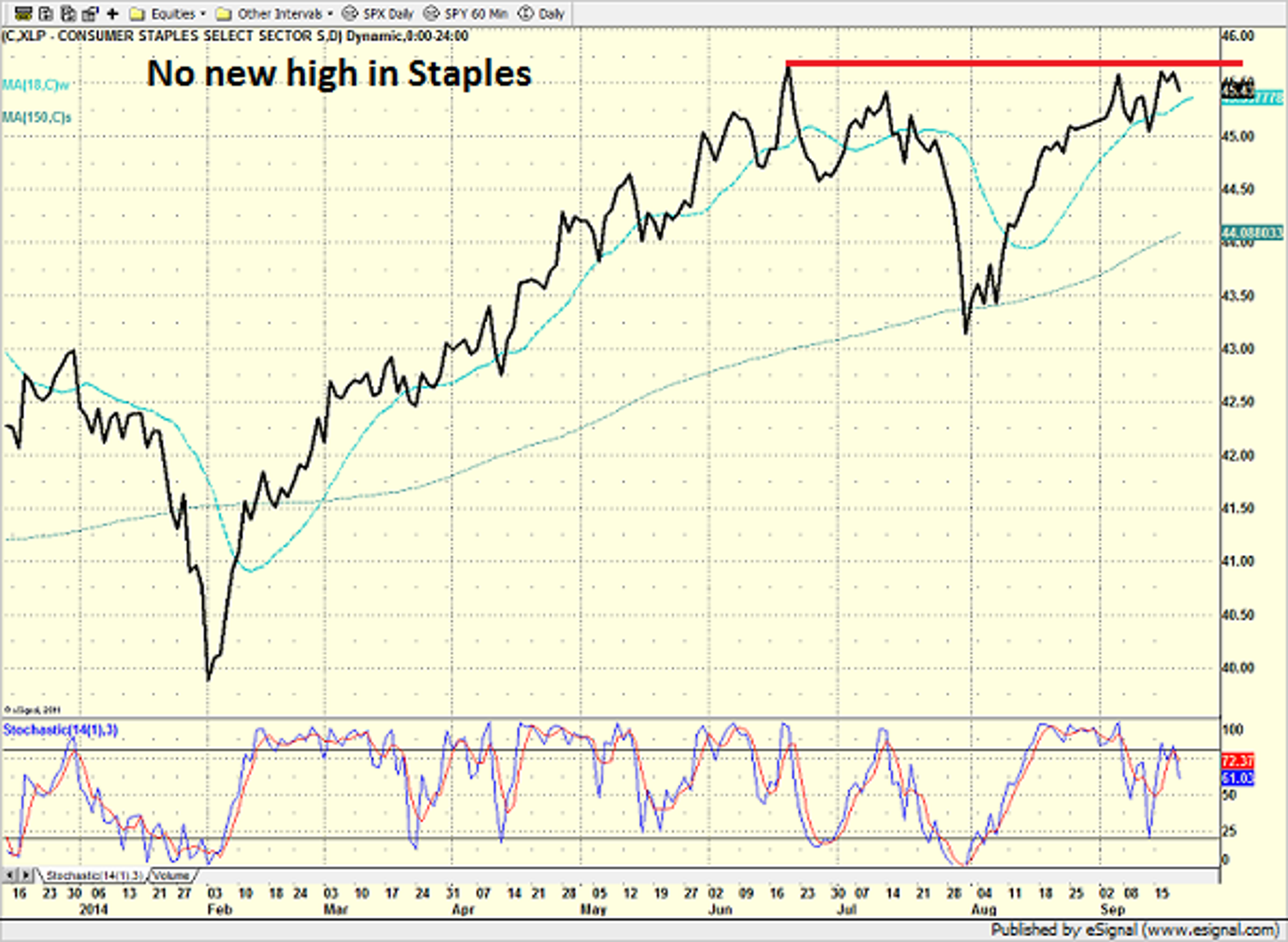

Consumer Staples Select SPDR XLP - Daily

While the consumer staples sector isn't generally viewed as an exciting play, the XLP is more than 50 percent higher than the prior long-term peaks seen in 2007 and 2008. This has clearly been a "fan favorite" among fund managers since the end of the crisis.

However, from a shorter-term perspective, staples also sports a bit of a divergence. Based on the fact that the XLP is a stone's throw from its recent high, this could be considered more of a non-confirmation than a divergence. Thus, analysts will be watching this sector to see if it can manage to break out in the near-term.

Consumer Discretionary Select SPDR XLY - Daily

Finally, there is the consumer discretionary sector.

This had also been a favorite among managers until recently as the XLV is more than 70 percent higher than the 2007/08 peak. Like technology, momentum has lagged of late, and like the staples, there has been no new high.

Although there are excuses for the recent underperformance, the key is that a divergence is indeed a divergence for our purposes.

To Sum Up

So let's review. There are reasons to be nervous about technical divergences among the major indices at this stage. Then in reviewing seven major sector charts, four appear to confirm the new highs seen in the "Generals" and three have diverged -- to varying degrees.

The bottom line: There are indeed divergences evident in the market, but again, the key question is whether they can be placed in the "bull killer" category.

It is important to note that many of the divergences are shorter-term in nature. As such, the "message" here may be that another pullback may be in the offing instead of a bear market. However, this is merely conjecture.

The key takeaway from this exercise is that since there are divergences present, it might be a good idea to exhibit some caution at this stage of the game from a longer-term perspective.

Related Links:

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.