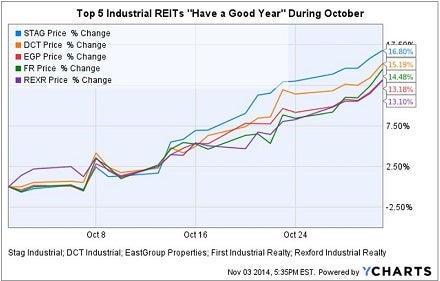

Top performer Stag Industrial Inc STAG was joined by DCT Industrial Trust Inc, Eastgroup Properties Inc, First Industrial Realty Trust, Inc. and Rexford Industrial Realty Inc, rounding out October's five most impressive gainers in the industrial REIT sector.

Three Charts Reflect A Bullish Story

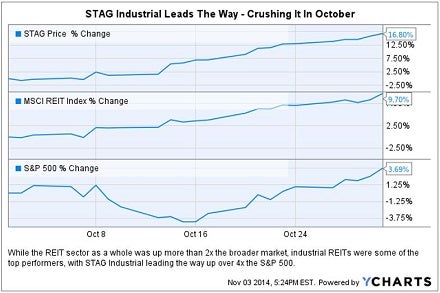

While the broader market had a shaky first half of October, REITs held firm before beginning a steady rise heading into Q3 earnings season.

The remaining four industrial REITs were also excellent performers compared to the S&P 500 during October 2014. Their impressive monthly gains ranged from Terreno Realty (11.2 percent) and Prologis Inc (10.9 percent), to Duke Realty (10.1 percent) and Monmouth Real Estate (9.7 percent).

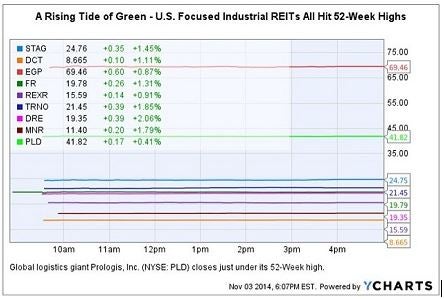

During the first day of trading in November, the industrial REIT sector hit 52-week highs almost across the board.

The entire space, as represented by the MSCI REIT Index, was up 9.7 percent in October.

STAG Industrial - Dividend Focus

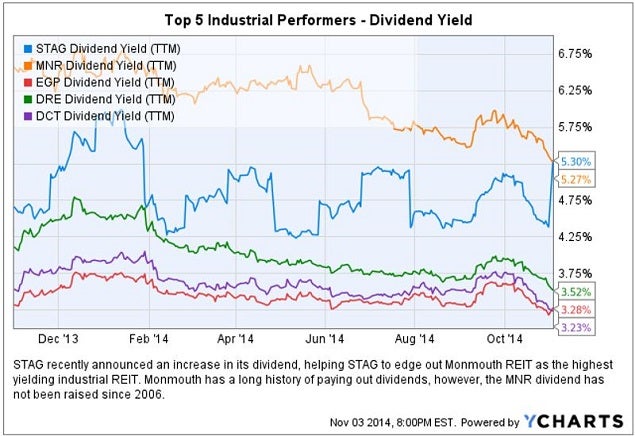

On October 30, STAG announced a 2.3 percent dividend increase from $1.32 to $1.35 per year.

It pays investors monthly dividends and has consistently raised payments since its IPO in April 2011. The new dividend equates to $0.1125 per share paid each month, good for a sector-leading 5.3 percent yield.

It is rare to find a REIT that is a sector-leader in both share price and dividend yield, since these are inverse relationships. The only way to both is by consistently growing AFFO (cash available for distribution), which funds dividend growth.

STAG Income Plus Growth Strategy

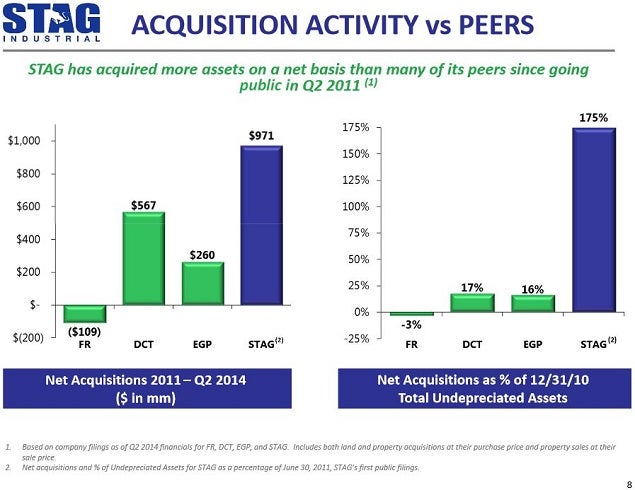

STAG is able to accomplish sector-leading performance by executing on its unique business model of acquiring Class-B buildings in secondary markets. By venturing into these markets, STAG avoids competing with its publicly-traded REIT peers for acquisitions.

This has driven STAG to acquire properties at cap rates in the 9 percent range -- considerably higher than its peers focused on Class-A buildings in coastal and metro-markets.

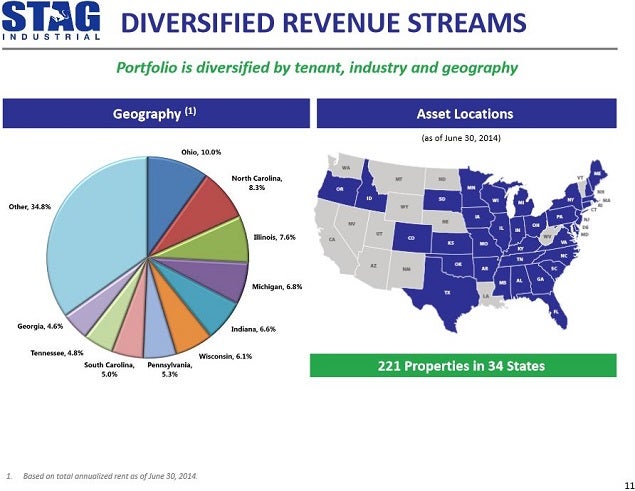

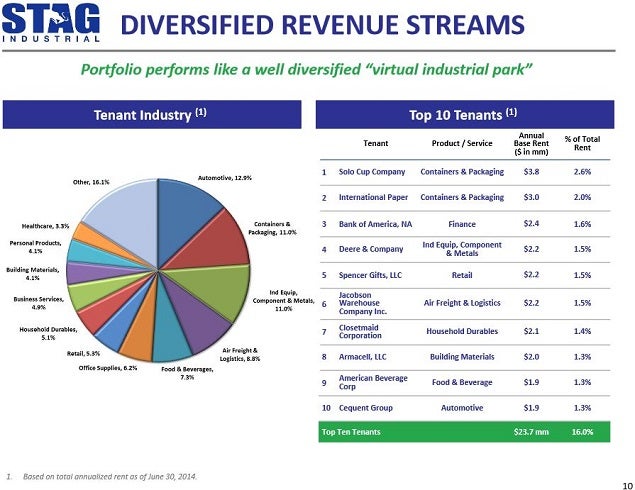

STAG owns many buildings that are located in the industrial heartland and smaller markets, however, the Top 10 tenant list reflects a focus on credit tenants and mission-critical facilities.

Can STAG Continue To Grow Profitably?

Based on the statement made by CFO Geoff Jervis during the STAG Q3 earnings call on October 30, it appears there is a clear runway for future growth.

"As we look forward," he said, "we feel confident that given our $1.4 billion pipeline, we will be able to acquire at a pace to meet our 25% acquisition target in 2015, equating to $450 million to $475 million of calendar year acquisitions."

How About STAG's Balance Sheet?

At the margin, all REITs generate income by maintaining a weighted average cost of capital below the cap rate of their real estate portfolio. Because REITs pay out at least 90 percent of taxable income as dividends to investors, in order to grow, REITs constantly have to access debt and equity capital markets.

As of September 30, STAG had a total enterprise value of $2.1 billion, comprised of $1.2 billion in equity market cap, $139 million of preferred equity and total debt of $678.2 million. STAG carries a Fitch Rating of BBB- on its debt and a BB mark on its preferred equity.

The company's weighted average cost of debt was 3.62 percent, down from 3.98 percent year-over-year. One caveat: STAG's debt duration now averages only 4.5 years. This, however, matches up well with STAG's lease maturities signed in 2014, which average 4.6 years.

Final Thoughts

STAG has been operating as a publicly-traded company for a relatively short time period. This has been a period of low interest rates, relatively little new industrial construction in the majority of STAG's markets, and a growing U.S. economy.

The recent outperformance by the entire industrial REIT sector is a vote of confidence for the U.S. economy moving forward.

It remains to be seen how the STAG strategy of owning older facilities in secondary markets will hold up in a rising interest rate environment. However, for the time being, it appears it is well-positioned to continue its accretive growth through 2015.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.