Although the intraday direction in the stock market is driven largely by algorithmic trading these days and can change at the drop of a hat (which is actually an eternity when measured in milliseconds), the recent price action would seem to suggest that the worries in the market are becoming more predominant.

The primary sources of worry at this time include the impact of the rising dollar on earnings, the crash in oil, the dive in bond yields (do bonds know something stocks don't?), Europe's economy, Greece, China and finally the U.S. economic data here at home.

On Monday morning, traders have received additional inputs on a couple of these fronts. First off, China's official PMI sank below the all-important 50-level, which means the manufacturing sector in the world's second biggest economy is now officially in contraction mode.

Stocks in Shanghai suffered as a result, dropping by -2.57 percent overnight - and there are already more calls on Chinese officials for additional stimulus.

In Europe, the PMI releases were less harsh, with the Eurozone Manufacturing PMI actually inching up on a monthly basis. However, the message from the results was that the economies of the EU continue to stagnate.

The good news from across the pond is that new Greek PM Tsipras appeared to a bit more conciliatory over the weekend, saying that Greece will repay its debts and reach out to creditors. As such, the worry over a potential "Grexit" have been moved to the back burner this morning.

There is also a wee bit less worry on the oil front today.

Crude futures are continued to move higher again this morning, after surging up 8 percent on Friday afternoon. While the move is viewed largely as short-covering, it should be noted that this is the first real attempt at stabilization in the commodities space in over four months. As such, there is some hope (albeit slim at this stage) that the crash in oil is ending.

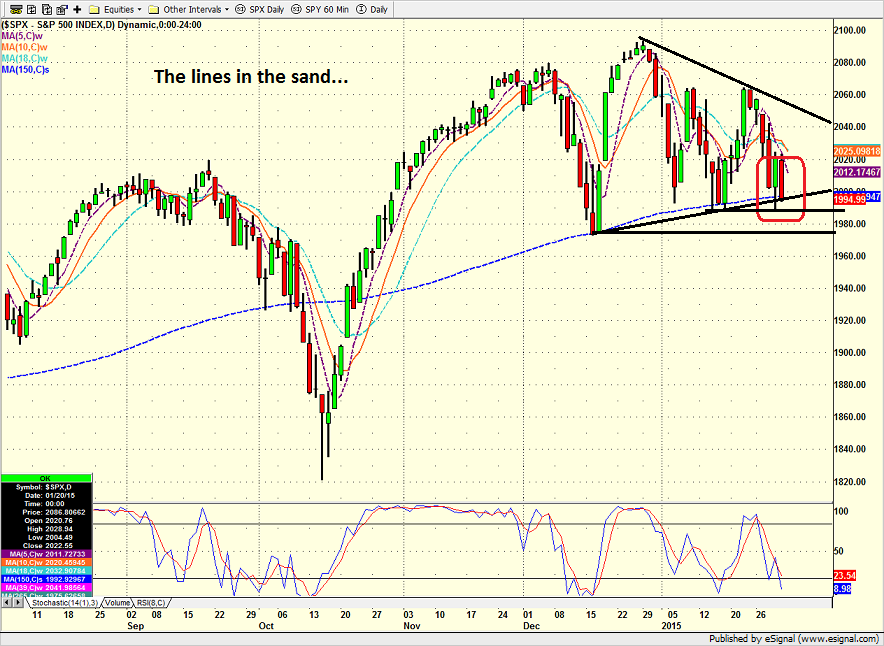

So, with nothing new to really worry about so far this morning and prices of the major blue chip indices here in the U.S. sitting right at important lines in the sand, it appears that stock prices will open slightly higher at the open on Wall Street today.

However, we note that if the S&P 500 were to move lower by about 25 points, there is little doubt that technical selling could take over. As such a bounce would be logical at this stage.

Current Market Environment

While many of Wall Street's old-time technical rules are more art than science, one of the oldest adages in the book is that when volatility rises to a meaningful degree, the major trend is about to change. And to be sure, volatility has increased thus far in 2015.

So, with the Dow and S&P 500 perched right at several important lines in the sand, the bears can be heard reminding anyone and everyone of this ago-old adage.

However, we prefer to listen to the message from our disciplined market models, which remain neutral at this stage and suggest that some caution may be warranted.

Technical Take

The key takeaway from the charts of the Dow and S&P right now is that the bears on the brink of what could be an important move and the bulls have their backs up against the wall. In short, everyone under the sun sees where the 150-day moving average on the S&P 500 is.

Everyone also sees that the blue chip indices are flirting with important near-term support and that that both the December lows as well as the 200-day moving averages are just below current levels. So, the bottom line is that the near-term price action could be very important.

S&P 500 SPY - Daily

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.