On one hand I want to applaud this analyst for taking a contrary position in an industry where pack behavior dominates. On the other hand, this is the difference between a portfolio manager and an analyst... you can be wrong for 572% and still keep your job. (or in his case, he was promoted by jumping to a much more visible firm) In the words of one of the pre eminent crime fighters of the past generation - Mr. Wible missed the stock "by that much."

Let me be clear, I had (have) some of the same concerns Mr. Wible had in terms of the business of Netflix (NFLX) but at worst it kept me out of the stock - standing in front of a freight train is not something you can afford to do in the non analyst world. So instead of fighting the herd, I've from time to time joined it - even if I have long term concerns. Who knows how it ends up in a decade, but for now not being long has been wrong.

Via Bloomberg:

Sold my Netflix two weeks ago

Market News and Data brought to you by Benzinga APIs

Let me be clear, I had (have) some of the same concerns Mr. Wible had in terms of the business of Netflix (NFLX) but at worst it kept me out of the stock - standing in front of a freight train is not something you can afford to do in the non analyst world. So instead of fighting the herd, I've from time to time joined it - even if I have long term concerns. Who knows how it ends up in a decade, but for now not being long has been wrong.

Via Bloomberg:

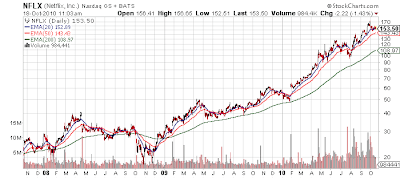

- Tony Wible loves streaming movies from Netflix Inc. Ask the Janney Montgomery Scott analyst what he thinks of the company's stock, and the affection ends there. Since April 2007, first at Citigroup Inc. and now at Janney, Wible has argued shares of the mail-order and online movie service are too costly or too risky. He has had a “sell” rating most of that time, with a couple of “hold” breaks.

- Clients who listened have missed out on the best stock in the Russell 1000 over the past 3 1/2 years and a gain of 572 percent. A $100,000 investment then in Los Gatos, California- based Netflix would be worth almost $672,000 today. A similar bet on the S&P 500 Media Index, which includes Time Warner Inc. and Walt Disney Co., would have fallen to $83,000.

- “There's no doubt we've been wrong on the stock,” the Philadelphia-based analyst said in an interview. “It's been a bad call. What's been phenomenal with Netflix is the Street's propensity to ignore future risk.”

- Wible, 34, who holds a degree in economics and finance from York College of Pennsylvania, argues Netflix faces threats from Amazon.com Inc., Apple Inc., Time Warner's HBO and cable companies that plan to offer fare online.

- The company's $8.99-a- month Web-and-one-DVD service may cannibalize its higher-priced subscriptions at the same time that costs for film rights are rising. The pressure will build in the next year, he said. “Netflix is a great product, it's a great platform,” Wible said. “It's just that its market potential is limited. This is a story about growth and momentum and those stories can break at any time.”

- Netflix has almost tripled this year and has a market value of $8.15 billion. The company went public in May 2002 at $7.50 a share, adjusted for splits. Gains in Netflix have been driven by rising sales and profit, as the company has taken customers from brick-and-mortar rivals such as Movie Gallery Inc., which is going out of business, and Blockbuster Inc., now in bankruptcy.

- This year, sales are forecast to grow 29 percent to $2.16 billion, the average of 26 estimatescompiled by Bloomberg, from $1.67 billion in 2009. Net income is projected to increase 32 percent to $152.7 million.

- On Oct. 6, Wible boosted his fair value estimate on Netflix to $110 from $61, based on 20 times projected 2012 earnings per share of $5.52. “I look at Netflix as being like a cable network and I assign a value based on what I think is a really good cable network,” Wible said, citing Discovery Communications Inc. “While the growth profile on Netflix is higher, the risk profile is also higher.”

- Netflix must win new customers at a faster clip to offset falling average spending by subscribers, Wible said. He predicts more users will drop mail-order plans, priced as high as $16.99 a month according to the website, for the $8.99 service. (but costs will also be lower without having to pay for mailing)

- In August, Netflix agreed to pay almost $1 billion for rights to movies from Viacom Inc.'s Paramount Pictures, Lions Gate Entertainment Corp. and Metro-Goldwyn-Mayer Inc.

- Wible says competition will lead to content bidding wars that could force Netflix to raise fees on the 18.5 million customers it expects by year-end. That would slow subscriber growth even if Netflix succeeds in duplicating its service in other countries. (important to watch how Hulu - which should IPO in the next year - does in this space)

- “It's a battle of philosophies,” Wible said. “There's the Internet philosophy. It applies the ideology that big brands win with a first-mover advantage. Then there's the media philosophy that content is king.”

On the other side of the ledger is the "first mover" advantage.

- “The only thing better than Netflix at $9 is McDonald's $1 menu,” said David Eiswert, manager of the Baltimore-based T. Rowe Price Global Technology Fund, which held 12,400 Netflix shares as of June 30. The company's biggest asset is its growing subscriber base, Eiswert said in an interview. A new entrant would spend $500 million to $1 billion for similar film and TV rights, and then have to win subscribers as Netflix becomes ubiquitous on Internet TVs, Blu-ray players and mobile devices. “Sure, the risk is that a large competitor is going to be willing to step up and take a $1 billion hit to operating expenses for two years,” Eiswert said. “But that's an awful lot of pain and what do you get?”

Sold my Netflix two weeks ago

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In: Consumer DiscretionaryInternet Retail

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in