Loading...

Loading...

Barclays initiated coverage on NGL Energy Partners LP

NGL Tuesday with an Equal Weight rating and $31 price target.

Analysts led by Brian J. Zarahn commented that the company was a diversified, mid-cap MLP that offered "a healthy 9.5 percent yield plus 6.0 percent distribution growth."

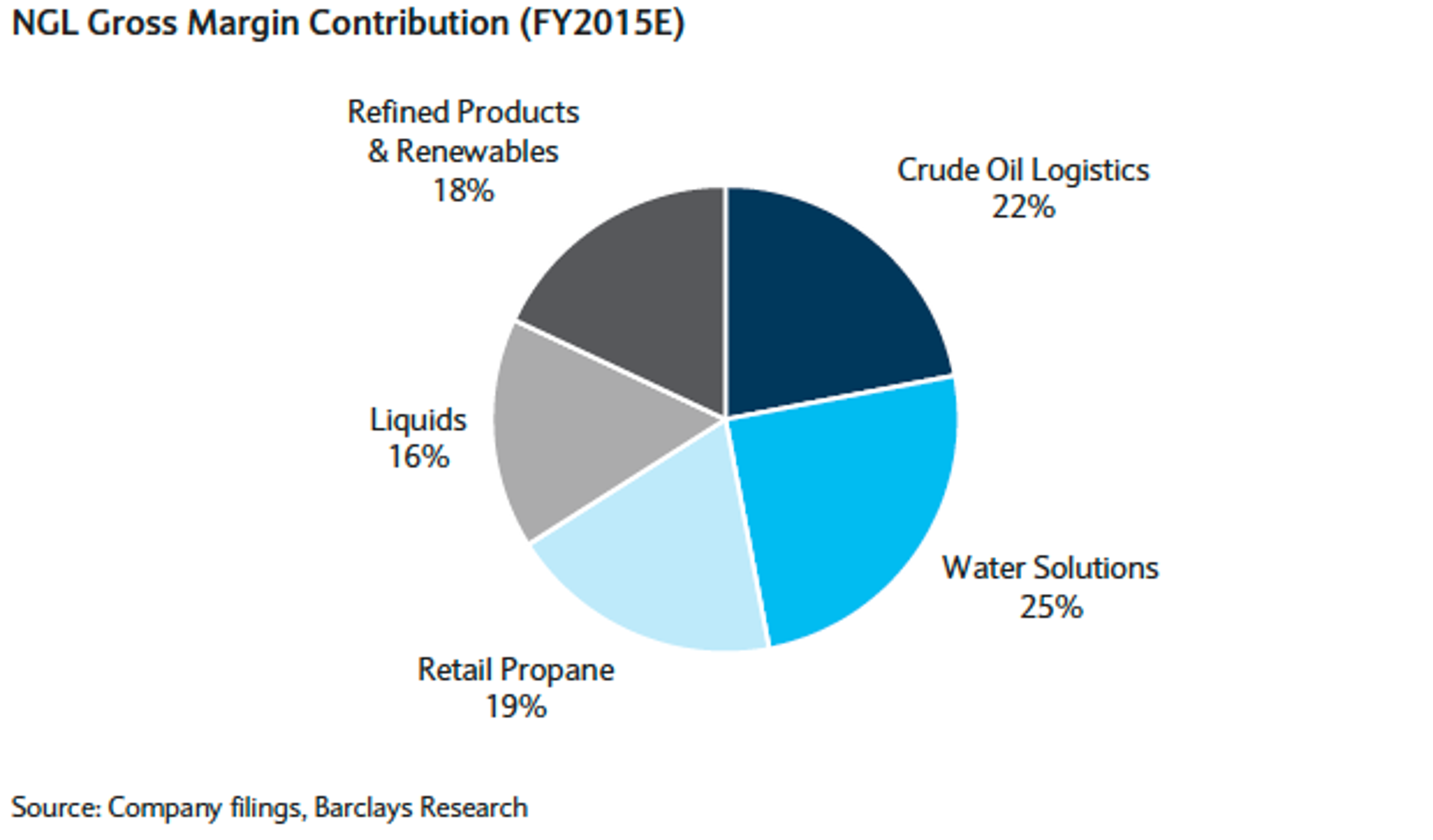

Following its IPO in May 2011, Zarahn said that NGL had "transformed from a pure play propane MLP to a diversified MLP with crude, refined products, NGL, propane and renewable assets."

Cash flow stability was "supported by a geographically and operationally diverse set of midstream assets and majority fee-based/fixed-margin mix reducing commodity exposure," according to Zarahn.

The analysts felt that headwinds for NGL's water solutions business from low oil prices would be offset by other areas of business, in particular the crude logistics business.

NGL's growth has come largely through its 40+ acquisitions over the past 4 years. The Magnum NGL in Utah salt cavern storage was the largest acquisition YTD at $280 million.

The company's largest organic project was the $965 million Grand Mesa crude pipeline that "will provide 200

mbpd of takeaway capacity from the DJ Basin to NGL's Cushing terminal in late 2016," according to the analysts.

The firm's 6 percent 2015-2018 CAGR forecast was based on contributions from acquisitions as well as

organic projects.

The $31 price target was based on a forward 12-month distribution run rate of $2.59 per unit and 8.4 percent target yield.

NGL Energy Partners LP recently traded at $26.41, up 1.27 percent.

Loading...

Loading...

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in