Earnings season is approaching fast.

Alcoa AA unofficially kicks off the Q2 reporting period when the aluminum maker—a barometer of global industrial demand and the sting of a too-strong dollar—reports Wednesday afternoon. It’ll be interesting to see if company-specific news can crawl out from Greece’s news shadow and bring a new focus to a Wall Street that limped out of Q2. What is clear, stock market volatility is percolating.

U.S. stocks were positioned to open sharply lower Monday, following Asia and Europe’s stock declines. Stock retreats follow the Greeks’ decisive rejection of a bailout deal proposed by the country’s international creditors.

The new deal demanded tighter austerity measures than those in place since 2010 in return for emergency funds. Greece dug in out of pride and what they hope is negotiating power. But guess who’s likely to dig in, too? The rest of powerful Europe—those holding the cards and the lighter balance sheets.

Early news reports say Germany has little interest in returning to the bargaining table. At the least tough, drawn-out talks lie ahead and there is little guarantee that a bailout deal can be reached in time to save the banking system from insolvency within weeks, the Wall Street Journal reports.

For U.S. markets, the most important factor right now may be the prolonged timeline to reach any kind of Greek certainty. And, of course, Greece’s fate may determine the course for debt-strapped Italy and Portugal.

Volatility Stirs

Even with Greece’s fiscal future and the makeup of the eurozone on the line, U.S. stock markets have proved to be tough-skinned—so far. The S&P 500 (SPX) logged sharp spikes as Q2 wrapped, but ultimately ended with little changed for the three-month period.

The CBOE Volatility Index (VIX) jumped to multi-month highs of 19.8 when Greece and its creditors twisted in tough negotiations. Trading has been somewhat choppy since. VIX, the market’s “fear gauge,” eased back to 16.79 on Friday.

Figure 1: VIX Itself Is Volatile. The CBOE Volatility Index (VIX) jumped to multi-month highs of 19.8 in late June when intensifying Greece uncertainty stole market focus. VIX, the market’s “fear gauge,” eased back to 16.79 on Friday but remains well above the sub-12 reading hit earlier in Q2. Data source: CBOE. Chart source: TD Ameritrade’s thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results.

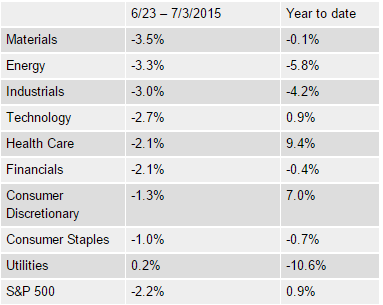

Still, VIX is well above the levels seen less than two weeks ago, when the index dipped back below 12 and to the lower end of the 2015 range. Since that time, while VIX is up nearly 40%, the S&P 500 has shed 2.2% and nearly every sector of the market has participated in the pullback.

Which groups fared the worst? The table below breaks down sector performance since June 23, when the S&P 500 was back within striking distance of its May 21 record closing high of 2130.82.

Economically sensitive groups, including basic materials, energy, and industrials, have paced the decline. Consumer stocks fared better, but have suffered their own losses. In fact, only the utility names were left unscathed.

Bracing For Earnings

Now, some market focus is likely to shift toward earnings that could show a few lumps.

According to Zacks Investment Research, total earnings for S&P 500 companies are expected to be down 7.3% from a year ago on a 6.1% drop in revenues. That follows Q1’s 2.4% year-over-year earnings growth on 3.2% lower revenues. The strong dollar’s crimp on multinational earnings is expected to be a factor.

As for Alcoa, analysts polled by FactSet expect the company to post a Q2 profit of 23 cents a share, down from 28 cents a share in the previous quarter but up from 18 cents a share a year earlier. The FactSet survey calls for $5.81 billion in Q2 sales, down slightly from the $5.82 billion Alcoa reported in Q1 and the $5.84 billion it reported a year ago.

Beyond Alcoa, PepsiCo PEP is likely the only report of broad market significance this week. The beverage company reports Thursday morning. The floodgates then open wide beginning in mid-July, and the market will get a barrage of reports in the month that follows.

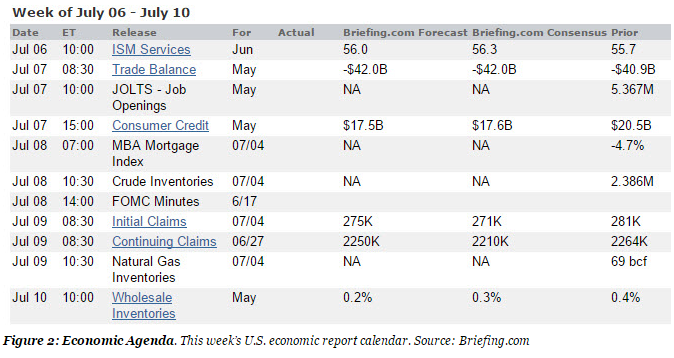

Other events this week include a meeting of Group of Eight economic leaders on Tuesday. The release of Federal Open Market Committee (FOMC) minutes Wednesday afternoon could potentially stir up action in the bond pits if the text hints at future interest rate policy (see the full economic schedule in figure 2). And some of the agricultural-related names might come into focus before the weekend as the government releases its crop report Friday afternoon.

Good trading,

JJ

This piece was originally posted here by JJ Kinahan on July 6, 2015.

TD Ameritrade, Inc., member FINRA/SIPC. Commentary provided for educational purposes only. Past performance of a security, strategy, or index is no guarantee of future results or investment success. Inclusion of specific security names in this commentary does not constitute a recommendation from TD Ameritrade to buy, sell, or hold.

Options involve risks and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before investing. Supporting documentation for any claims, comparison, statistics, or other technical data will be supplied upon request.

The information is not intended to be investment advice and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade. Clients must consider all relevant risk factors, including their own personal financial situations, before trading.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.