Year 4, Week 13 Major Position Changes

To see historic weekly fund changes click here OR the label at the bottom of this entry entitled 'fund positions'.

Cash: 69.0% (v 69.2% last week)

20 long bias: 27.6% (v 26.3% last week)

4 short bias: 3.4% (v 4.5% last week) [Note: Long dollar positions considered 'short']

24 positions (vs 22 last week)

Weekly thoughts

Last week marked much of the same from the previous 2 months - the market sold off one of its non POMO days but generally drifted up or sideways on POMO days, as market participants feel "risk free" as the Bernanke put sits below the market. Action turned very quiet Thursday and Friday as traders sat on hands ahead of one of the busiest weeks of the year, if not *the* busiest in terms of news events. Economic data last week (home sales, durable goods, GDP) continued to essentially be ignored... the only selloff occurred on a WSJ leak of a QE program that might be smaller (on the front end) than speculators anticipated... but that was forgotten by the next day. The market has made it through 2 of the most tricky months - September which is historically the worst, and October which is the month of crashes. Now it enters the best time of year (November - May)...

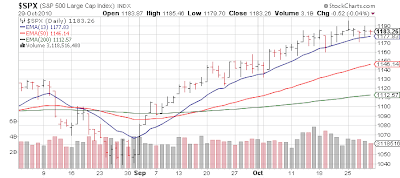

The S&P 500 continues to run along the 13 day moving average and bounce repeatedly. Until this pattern changes, traders will play it. It will eventually blow up, most likely in spectacular fashion, but like a squirrel storing nuts ahead of winter - a trader can store up profits in anticipation of taking an invariable loss playing this "no brainer" trade.

While the trend is still up the 45 degree angle enjoyed in September and early October has slowed, and the market has become range bound since mid October in the S&P 1170 to 1190 range. This could either be a topping process or a new base being built for a new leg up. Until proven otherwise, as the index is above all key moving averages, one has to give the benefit of the doubt to the latter. Sector rotation has been taking place to some degree as some of the groups (such as technology) that led the market up in the early stages of this run, took a rest, and are now being run into again. The one positive is stock picking has seemed to mattered more of late, rather than the "student body" left trading that has come to characterize markets since mid 2007. How long this lasts is anyone's guess. (don't forget the gaps at S&P 1090, and 1110)

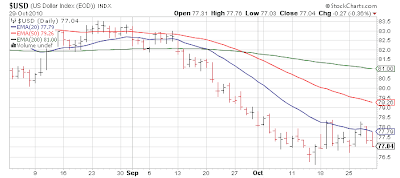

The U.S. dollar imploding was a catalyst for much of the first half of this run off the late August lows but was reaching extremes in sentiment three weeks ago. It staged a minor rally to work off some of that excess but truly only jumped to the 20 day moving average and now seems back in poor condition. The only saving grace for the dollar are potential moves by other countries central bankers to follow the Bernanke playbook and try to desperately weaken their currencies using similar 'printing' strategies. But no one is doing it in size and scale as the U.S. - hence hard to make a case for the U.S. dollar other than "shorting is a crowded trade". If the dollar falls to new (recent) lows - all bets off.

As the dollar 'stabilizes' in this range, the ramp in (some) commodity stocks has slowed - even though specific commodities themselves (i.e. cotton) continue to ramp. This is part of the rotation I spoke about above. Much of this money seems to have flowed right back into the new 'nifty 50' of the modern stock market - "the same old" names which trade at excess valuations, but speculators are willing to buy at any price.

---------------------------------

Economic news has not mattered in a long time as buyers step in under cover of QE2. This week would normally be dominated by the monthly jobs report Friday, but it is being overshadowed by the Fed meeting, and elections. Both events have been discounted to no end for months, but somehow we still seem to rally on the same story. Aside from these catalysts we also have the key ISM reports so it is an extremely heavy week in terms of data. The only question ahead is do we sell off on ANY news anymore; buy the rumor, sell the news now has been replaced by buy the rumor, and buy the news too.

Please note aside from the Fed meeting, the ECB and Bank of England also 'report' this week - it will be interesting to see if the Bank of England in particular does any 'retaliatory' printing to try to respond to the Fed. Also the Bank of Japan moved up its meeting specifically this week, in what seems like a sure sign they will announce something to combat the Ben helicopter drop.

Monday: Personal Income & Outlays (8:30 AM), ISM Manufacturing (10 AM) Construction Spending (10 AM) - the market keys on the ISM Manufacturing report, although Wednesday's non manufacturing is far more important in terms of economic impact. Consensus 54.5.

Tuesday: FOMC Meeting Day 1, Elections

Wednesday: FOMC Meeting Day 2 with announcement 2:15 PM. ADP Employment (8:15 AM), ISM Non Manufacturing (10 AM), Factory Orders (10 AM) - Consensus 54.0 on ISM.

Thursday: Weekly Claims (8:30 AM), Productivity & Costs (8:30 AM) - the first drop below 450,000 in a long time on weekly claims last week; while still a recessionary level in the 430,000 this report will be key to watch to see if the momentum can continue downward.

Friday: Monthly Employment Data (8:30 AM) - consensus +60,000 jobs and 9.6% rate

POMO days - the Fed is taking a break off POMO during its meeting (Tue/Wed) but primary dealers will be taking Fed cash to "buy stuff" Monday the 1st and Thursday the 4th. I think a big psychological change will happen when the market actually breaks down on a POMO day. It has now become accepted the market cannot selloff on a POMO morning, and everyone is now front running this. Again I will repeat what I say over and over (and over) - when EVERYONE knows something in the market it traditionally stops working. But not in this market.

POMO days is a new feature on the calendar - essentially the Fed has been pumping $20B a month into the market. With QE2 we should expect a figure of $100B additional each month at least on the front end, with a goal of perhaps half a trillion in the next 3-6 months. Then from there the Fed can exact language such as "we'll monitor it from there and continue to adjust to the market as we see fit" holding an anvil over the heads of bears from here to infinity.

----------------------------------

Portfolio

The market did little last week - key move was a selloff Tuesday on a WSJ leak about some smaller front end QE - but extending the duration. Market participants whined .... for a day. Then back to the regularly scheduled melt up as the S&P 500 hit the 13 day moving average and bounced. Precious metals caught a bid late in the week, after Bank of Japan QE details.

This market remains 'unshortable' and will .... until it is not. Until the 13 day moving average can be broken, and then the 20 day moving average - all shorts on the indexes are more of the 'overextended to the upside' variety which offer a short window to try to execute in. As I take profits in some names, I am forcing myself to find new names to replace the long exposure with, although I am increasingly uncomfortable chasing an incredibly complacent market which has essentially become 'faith based' investing: "POMO will make us go higher" "QE2 will make us go higher" "Elections will make us go higher" "Ben Bernanke is my master" et al. We have had some nice earnings winners such as Las Vegas Sands (LVS), and when these jump I am taking profits and rolling into new names or other stocks such as BorgWarner (BWA) which continue to show excellent relative strength. Finding new entries in non extended stocks remains a challenge. I eagerly await the day to make money on the short side again...

On the long side:

On the short side:

Market News and Data brought to you by Benzinga APIsTo see historic weekly fund changes click here OR the label at the bottom of this entry entitled 'fund positions'.

Cash: 69.0% (v 69.2% last week)

20 long bias: 27.6% (v 26.3% last week)

4 short bias: 3.4% (v 4.5% last week) [Note: Long dollar positions considered 'short']

24 positions (vs 22 last week)

Weekly thoughts

Last week marked much of the same from the previous 2 months - the market sold off one of its non POMO days but generally drifted up or sideways on POMO days, as market participants feel "risk free" as the Bernanke put sits below the market. Action turned very quiet Thursday and Friday as traders sat on hands ahead of one of the busiest weeks of the year, if not *the* busiest in terms of news events. Economic data last week (home sales, durable goods, GDP) continued to essentially be ignored... the only selloff occurred on a WSJ leak of a QE program that might be smaller (on the front end) than speculators anticipated... but that was forgotten by the next day. The market has made it through 2 of the most tricky months - September which is historically the worst, and October which is the month of crashes. Now it enters the best time of year (November - May)...

The S&P 500 continues to run along the 13 day moving average and bounce repeatedly. Until this pattern changes, traders will play it. It will eventually blow up, most likely in spectacular fashion, but like a squirrel storing nuts ahead of winter - a trader can store up profits in anticipation of taking an invariable loss playing this "no brainer" trade.

While the trend is still up the 45 degree angle enjoyed in September and early October has slowed, and the market has become range bound since mid October in the S&P 1170 to 1190 range. This could either be a topping process or a new base being built for a new leg up. Until proven otherwise, as the index is above all key moving averages, one has to give the benefit of the doubt to the latter. Sector rotation has been taking place to some degree as some of the groups (such as technology) that led the market up in the early stages of this run, took a rest, and are now being run into again. The one positive is stock picking has seemed to mattered more of late, rather than the "student body" left trading that has come to characterize markets since mid 2007. How long this lasts is anyone's guess. (don't forget the gaps at S&P 1090, and 1110)

The U.S. dollar imploding was a catalyst for much of the first half of this run off the late August lows but was reaching extremes in sentiment three weeks ago. It staged a minor rally to work off some of that excess but truly only jumped to the 20 day moving average and now seems back in poor condition. The only saving grace for the dollar are potential moves by other countries central bankers to follow the Bernanke playbook and try to desperately weaken their currencies using similar 'printing' strategies. But no one is doing it in size and scale as the U.S. - hence hard to make a case for the U.S. dollar other than "shorting is a crowded trade". If the dollar falls to new (recent) lows - all bets off.

As the dollar 'stabilizes' in this range, the ramp in (some) commodity stocks has slowed - even though specific commodities themselves (i.e. cotton) continue to ramp. This is part of the rotation I spoke about above. Much of this money seems to have flowed right back into the new 'nifty 50' of the modern stock market - "the same old" names which trade at excess valuations, but speculators are willing to buy at any price.

---------------------------------

Economic news has not mattered in a long time as buyers step in under cover of QE2. This week would normally be dominated by the monthly jobs report Friday, but it is being overshadowed by the Fed meeting, and elections. Both events have been discounted to no end for months, but somehow we still seem to rally on the same story. Aside from these catalysts we also have the key ISM reports so it is an extremely heavy week in terms of data. The only question ahead is do we sell off on ANY news anymore; buy the rumor, sell the news now has been replaced by buy the rumor, and buy the news too.

Please note aside from the Fed meeting, the ECB and Bank of England also 'report' this week - it will be interesting to see if the Bank of England in particular does any 'retaliatory' printing to try to respond to the Fed. Also the Bank of Japan moved up its meeting specifically this week, in what seems like a sure sign they will announce something to combat the Ben helicopter drop.

Monday: Personal Income & Outlays (8:30 AM), ISM Manufacturing (10 AM) Construction Spending (10 AM) - the market keys on the ISM Manufacturing report, although Wednesday's non manufacturing is far more important in terms of economic impact. Consensus 54.5.

Tuesday: FOMC Meeting Day 1, Elections

Wednesday: FOMC Meeting Day 2 with announcement 2:15 PM. ADP Employment (8:15 AM), ISM Non Manufacturing (10 AM), Factory Orders (10 AM) - Consensus 54.0 on ISM.

Thursday: Weekly Claims (8:30 AM), Productivity & Costs (8:30 AM) - the first drop below 450,000 in a long time on weekly claims last week; while still a recessionary level in the 430,000 this report will be key to watch to see if the momentum can continue downward.

Friday: Monthly Employment Data (8:30 AM) - consensus +60,000 jobs and 9.6% rate

POMO days - the Fed is taking a break off POMO during its meeting (Tue/Wed) but primary dealers will be taking Fed cash to "buy stuff" Monday the 1st and Thursday the 4th. I think a big psychological change will happen when the market actually breaks down on a POMO day. It has now become accepted the market cannot selloff on a POMO morning, and everyone is now front running this. Again I will repeat what I say over and over (and over) - when EVERYONE knows something in the market it traditionally stops working. But not in this market.

POMO days is a new feature on the calendar - essentially the Fed has been pumping $20B a month into the market. With QE2 we should expect a figure of $100B additional each month at least on the front end, with a goal of perhaps half a trillion in the next 3-6 months. Then from there the Fed can exact language such as "we'll monitor it from there and continue to adjust to the market as we see fit" holding an anvil over the heads of bears from here to infinity.

----------------------------------

Portfolio

The market did little last week - key move was a selloff Tuesday on a WSJ leak about some smaller front end QE - but extending the duration. Market participants whined .... for a day. Then back to the regularly scheduled melt up as the S&P 500 hit the 13 day moving average and bounced. Precious metals caught a bid late in the week, after Bank of Japan QE details.

This market remains 'unshortable' and will .... until it is not. Until the 13 day moving average can be broken, and then the 20 day moving average - all shorts on the indexes are more of the 'overextended to the upside' variety which offer a short window to try to execute in. As I take profits in some names, I am forcing myself to find new names to replace the long exposure with, although I am increasingly uncomfortable chasing an incredibly complacent market which has essentially become 'faith based' investing: "POMO will make us go higher" "QE2 will make us go higher" "Elections will make us go higher" "Ben Bernanke is my master" et al. We have had some nice earnings winners such as Las Vegas Sands (LVS), and when these jump I am taking profits and rolling into new names or other stocks such as BorgWarner (BWA) which continue to show excellent relative strength. Finding new entries in non extended stocks remains a challenge. I eagerly await the day to make money on the short side again...

On the long side:

- Monday, I started a modest 1% position in Ford (F) after a very good earnings report - the stock was very extended so I did not want to chase with large exposure, until (if) it pulled back.

- Tuesday, a small stop loss in Bucryus (BUCY) was executed as the WSJ leak on QE, put pressure on the market in the opening minutes. After my stop loss was collected the stock immediately bounced well over 2%.

- A new position of 2.2% exposure was started in Citrix Systems (CTXS) after an excellent earnings report, and the stock breaking over some resistance.

- Wednesday, Whirlpool (WHR) was closed after an adverse reaction to earnings; took a 5% loss.

- Wednesday afternoon, I bought a 4.5% exposure in SPY calls for no reason other than "POMO" on Thursday morning. They were sold the next morning for a 20% gain...

- I sold almost all Las Vegas Sands (LVS) this week - as this is one of the new "nifty 50". Half the remaining position was sold just ahead of earnings for a 25% gain, and the remainder the next morning for a 36% gain. This was about a 6 week trade from where I bought most of the exposure.

- Thursday, sold 2/3rds of Rovi (ROVI) going into earnings for 'flat'.

- Closed Kinder Morgan Partners (KMP), mostly out of boredom, taking a 2% loss.

- Added some exposure to BorgWarner (BWA) after another excellent earnings report.

- Friday, started a position in a new name - Eastman Chemical (EMN) - which is about as cyclical as you can ask for.

- Acme Packet (APKT) had a nice report but did not react 'great', since I wanted to keep some long exposure going after sales earlier in the week I added some to this position, mostly out of default.

- Precious metals looked poised for a new run after resting for a few weeks - I restarted a position in Silver Wheaton (SLW).

On the short side:

- Friday, I took a little off the Powershares US Dollar Bullish (UUP) position (our main hedge) as the dollar was rejected at the 20 day moving average and now sits in limbo.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In: Application SoftwareAuto Parts & EquipmentAutomobile ManufacturersCasinos & GamingCommunications EquipmentConstruction & Farm Machinery & Heavy TrucksConsumer DiscretionaryDiversified ChemicalsEnergyHousehold AppliancesIndustrialsInformation TechnologyMaterialsOil & Gas Storage & TransportationPrecious Metals & Minerals

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in