Leading U.S. stock averages point higher Friday after a rebound from a two-day drop landed the indexes back at key chart levels. Chinese stocks closed the books on their best two-week stint in some time, setting off global stock gains. And, gold futures slid from a four-month high as the U.S. dollar firmed.

Selling pressure could emerge if this Friday brings some typical pre-weekend jitters, aggravated with the extra volatility that may come with options expiration.

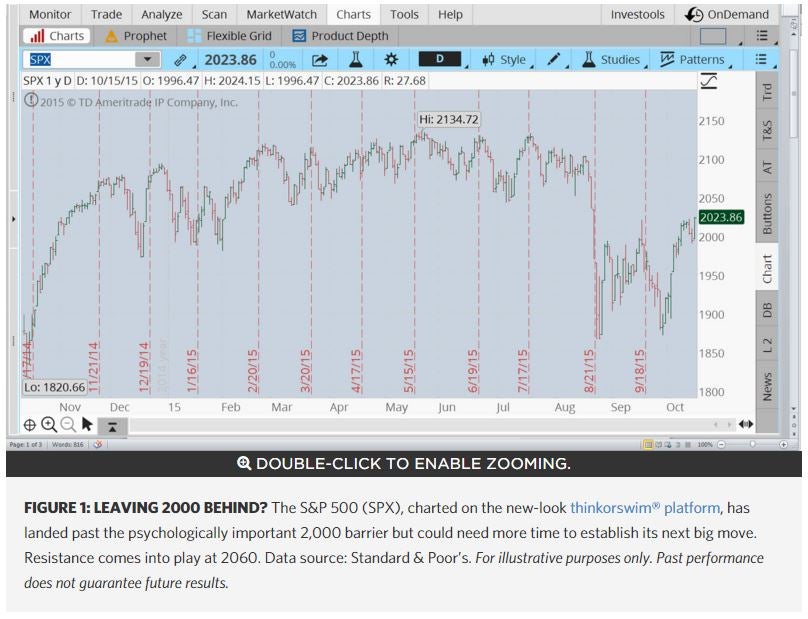

Thursday’s broad-market advance pushed the S&P 500 (SPX) up 1.5% to close at 2,023.86 and solidly above the psychologically important 2,000 level (figure 1). All 10 sectors were gainers, led by over 2% gains for financials and health care. SPX is now back at levels seen in the third week of August, before a massive selloff across the board eroded year-to-date gains. Resistance may come in at 2,060, which marks the 200-day moving average. SPX remains off 1.7% year to date.

As for the Dow Jones Industrial Average ($DJI), it logged a 1.3% gain Thursday to 17,141.75 for its highest level since August 19. Goldman Sachs Group Inc GS, higher after well-received earnings news, was a big driver for the Dow in the session. The NASDAQ Composite (COMP) gained 1.8% Thursday as buyers reemerged for the tattered biotech sector.

GE Sheds Light on Broader Market. General Electric GE reported a profit of $2.51 billion, or $0.25 per share in Q3, compared with a profit of $3.54 billion, or $0.35, a year earlier. Excluding special charges, adjusted operating earnings came in at $0.29 a share. Revenue ticked down 1% to $31.68 billion. Analysts polled by Thomson Reuters had forecast per-share operating earnings of $0.26 and revenue of $28.57 billion. GE beat the Street view, yes, but their deeper story may not be as shiny. Machine orders were down sharply as the commodities slowdown likely hit the conglomerate. As industry analysts like to remind us, there’s hardly a business that GE doesn’t touch in some way.

Tougher Than You Think. The U.S. economy "can handle" an increase in interest rates despite the risks around the economic outlook, Cleveland Fed President Loretta Mester said in a late Thursday speech. "It is appropriate for monetary policy to take a step back from the emergency measure of zero interest rates," Mester said, according to several financial press reports. Mester, who will earn a policy voting spot in 2016, said conditions warrant gradual increases for interest rates. The Fed meets later this month and again in December and its decision to raise rates for the first time since 2006 is neither easy nor a foregone conclusion. One measure of market expectations for Fed policy, the Fed funds futures market tracked by CME FedWatch, shows that select traders have pushed back expectations for the first hike until March.

Oil Back Below $50. Crude oil’s push above $50 earlier this month has faded. U.S.-traded crude futures were at $46.83 early Friday, up slightly after a heavy drop the day before. Brent crude futures remained in the red at some points on Friday. Supply continues to be the big issue even after published reports in recent sessions implied that persistently weak prices were starting to dent production plans. Still, the U.S. Energy Information Administration this week showed crude stocks grew by 7.6 million barrels last week, the highest increase in six months. Oil supplies are holding near record levels and so-so demand has worsened its price outlook. Earlier this week, the International Energy Agency, in its closely-watched monthly oil market report, cut its forecast for oil demand growth for next year by about 200,000 barrels a day compared to its previous outlook issued in September. IEA now sees world oil consumption rising by 1.2 million barrels a day in 2016, compared to a five-year-high growth of 1.8 million barrels a day in 2015.

Inclusion of specific security names in this commentary does not constitute a recommendation from TD Ameritrade to buy, sell, or hold. Market volatility, volume, and system availability may delay account access and trade executions.

Past performance of a security or strategy does not guarantee future results or success. Options are not suitable for all investors as the special risks inherent to options trading may expose investors to potentially rapid and substantial losses. Options trading subject to TD Ameritrade review and approval. Please read Characteristics and Risks of Standardized Options before investing in options.

Supporting documentation for any claims, comparisons, statistics, or other technical data will be supplied upon request. The information is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade.

Clients must consider all relevant risk factors, including their own personal financial situations, before trading. TD Ameritrade, Inc., member FINRA/SIPC. TD Ameritrade is a trademark jointly owned by TD Ameritrade IP Company, Inc. and The Toronto-Dominion Bank. © 2015 TD Ameritrade IP Company, Inc. All rights reserved. Used with permission.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.