I may be a bit biased because I never thought of the Coinstar (CSTR) story as something that was sustainable as 'high growth' in the long run (DVD kiosks? cmon), but the action today to adverse guidance is part of the worry I have with many names people are chasing in day after day, without regard to risk control. Many stocks are now up 40, 50, 60%+ since the last earnings period (CSTR was up over 40%) and in many cases at these valuations even guiding to 'in line' results or guidance is going to disappoint. Now, I would not hold Coinstar itself up to the standard of a lot of stocks I target in terms of secular growth stories, but it showcases the danger lurking in the earnings season ahead, even for superior companies.

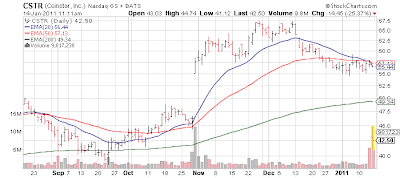

Chart wise - this is classic 'filling the gap' action. Ouch.

Via Bloomberg:

No position

Market News and Data brought to you by Benzinga APIsChart wise - this is classic 'filling the gap' action. Ouch.

Via Bloomberg:

- Coinstar Inc, operator of Redbox DVD vending machines, fell the most since July 2003 after preliminary fourth-quarter sales and profit missed projections because of delayed access to Hollywood's newest movies.

- The company has agreed to a 28-day delay in receiving the latest DVD releases from Hollywood, giving studios a four-week window to sell their latest movies before offering them for rental in Redbox kiosks.

- The delay requires management to do a better job of selecting titles to keep customers renting while they wait for newer releases, said Eric Wold, an analyst at Merriman Curhan Ford & Co. in New York. “They made the wrong decisions on what titles to stock,” said Wold, who rates the shares “buy” and doesn't own them. “There's a learning process.”

- The company, which has taken sales from traditional retailers such as Blockbuster, previously exceeded analysts' net-income estimates for eight straight quarters.

- “We underestimated the impact that the delay would have on demand during the fourth quarter,” Chief Executive Officer Paul Davis said in the statement. “We also expected much better performance from Blu-ray.”

- Fourth-quarter profit was 65 cents to 69 cents a share, excluding some items, compared with previous company projections of 79 cents to 85 cents, according to the statement. Sales rose 31 percent to $391 million, missing forecasts of $415 million to $440 million.

- Analysts had predicted profit of 86 cents a share, the average of seven estimates. They projected sales of $426.1 million, the average of 14 estimates.

No position

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in