It's like a soap opera around here. After the weekend 'exchange of ideas' (for the sordid explicit details feel free to head over to the BusinessInsider) on Weibo, Morgan Stanley (MS) has not issued the traditional "buy buy buy" coverage this morning now that the quiet period is over. You can bet their analyst was told to sit on the report by higher ups based on the embaressment this weekend. (again it appears that no actual Morgan Stanley employee was part of this web altercation, just someone posing as a Morgan Stanley employee - but DANG's CEO comments surely pissed off one of America's most powerful oligarchs all the same) As interesting, the other lead underwriter, CS also did not initiate coverage this morning - very strange to see the leads not waving the green flag on their product.

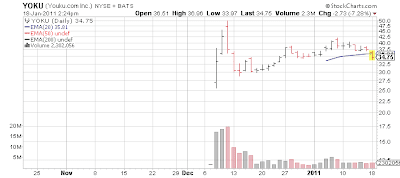

Both Youku.com (YOKU) and E-Commerce China Dangdang (DANG) are down 7%ish today as other analysts have chimed in with a host of 'neutrals'.... in Wall Street language "Sell". For an analyst to put a 'neutral' on companies like this, it means things are truly egregious in valuation (which they are) - after all the main job of analysts from the sell side areto say nice things so the investment banking arms of their banks can win future business help investors.

Via Herb Greenberg over at CNBC

Much like Gene at Piper I said back in December at today's insane valuations, a company like Youku.com could grow 100% a year for 4-5 years and only then maybe make some sense (maybe!) - but this is already priced in today as if there will be no competitors and a $50M revenue company will be $400M one in 4 years with no roadblocks. [Dec 13, 2010: Careful of that Youku on your Shoe] This is the same logic we were using in 1999 to justify Alan Greenspan pumping the market full of steroids, and valuations that no one could really defend.

No position

Market News and Data brought to you by Benzinga APIsBoth Youku.com (YOKU) and E-Commerce China Dangdang (DANG) are down 7%ish today as other analysts have chimed in with a host of 'neutrals'.... in Wall Street language "Sell". For an analyst to put a 'neutral' on companies like this, it means things are truly egregious in valuation (which they are) - after all the main job of analysts from the sell side are

Via Herb Greenberg over at CNBC

- With the post-IPO quiet period now over for Youku and E-commerce China Dangdang, two of the hottest Chinese deals in years, analysts from the firms' investment banks are out with a dash of reality: Unless you're a long-term investor, these things are expensive. And even then, it may pay to read the fine print as it relates to risks.

- On Dangdang Piper Jaffray's Gene Munster says the stock is fully-valued. His 12-month target: $30. (It is currently around $31.) At current levels, he says, investors “are investing for the five-plus year opportunity.” (Gene is being generous in his language by saying "are investing for the five plus year opportunity" - essentially this means the only way the valuation makes any sense is hyper growth for 5 years and investors TODAY are already pricing that in at current prices)

- Cowan analyst Jim Friedland, noting Dangdang's 112 percent rise since its IPO, “already reflects a strong growth scenario in an environment that remains highly competitive.” Competitors include Amazon's Joyo.com, 360buy.com (China's largest online merchant of consumer electronics), and Taobao, which operates China's largest online marketplace.

- Co-Lead bankers Credit-Suisse and Morgan Stanley have not yet chimed in. Morgan Stanley says it's not unusual to be a banker on the deal and not issue a report on the company for some time.

- On Youku,China's YouTube/Netflix: Munster of Piper is equally neutral, with a target of 40, or higher than the current price. “We expect Youku to be a significant beneficiary of the growth in online video ad dollars in China,” he says. “However, we note that current market valuations appear to price in similar expectations."

- James Mitchell of lead banker Goldman Sachs, also weighed in with a neutral rating and a target of $37. He said the company could get profitable quickly—perhaps as soon as late this year or early next year. He also noted the cost of content is rising rapidly.

Much like Gene at Piper I said back in December at today's insane valuations, a company like Youku.com could grow 100% a year for 4-5 years and only then maybe make some sense (maybe!) - but this is already priced in today as if there will be no competitors and a $50M revenue company will be $400M one in 4 years with no roadblocks. [Dec 13, 2010: Careful of that Youku on your Shoe] This is the same logic we were using in 1999 to justify Alan Greenspan pumping the market full of steroids, and valuations that no one could really defend.

No position

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Comments

Loading...

Posted In:

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in