The U.S. corporate tax reform chatter grows louder, with President Donald Trump himself promising last Friday that he would soon announce the most ambitious tax reform since the Reagan Era. Despite the teasers at several occasions, neither Trump or his team has shed light on specifics of the reform.

Why Trump Harps On Tax Reforms?

The contention is the U.S. corporate tax system has become out-of-sync and noncompetitive with the rest of the world. In fact, the prevailing corporate tax rate of 35 percent in the United States is among the highest in the world. Ever since Trump sounded out his intention to reform the tax system, analysts have scrambled to make provisions for the likely impact in their models.

Then there is something called the lock-of-effect, which discourages U.S. companies to repatriate their overseas profits. Estimates by a joint committee values the overseas cash horde waiting to be brought home sits at a massive $2.6 trillion at the end of 2015.

See Also: How Fed Governor Tarullo Stepping Down Changes The Balance Of Hawks And Doves On The FOMC

Tax Reform Proposed By Republicans

The House is proposing to replace the existing corporate tax with a destination-based cash flow tax, or DBCFT. Apart from lowering the tax rate to 20 percent from the current 35 percent, the DBCFT also seeks to remove the deductibility of interest payments, excludes investment from the tax base and impose a border adjustment tax, which is taxing imports at a full rate and exempting exports.

Even as a lot of uncertainty exist as to how the corporate tax system would be reformed, Benzinga examined the off shoots of the previous major corporate tax reform, which happened in 1986 under the then Republican President Ronald Reagan.

The Tax Reform Act Of 1986

The Tax Reform Act of 1986, or TRA was enacted on October 22, 1986, with the support of both Democrats and Republican, and sought a reduction of the tax rate and broaden the base. The Reagan administration insisted on the reforms being revenue and distribution neutral, with revenue neutrality referring to a situation when any revenue losses would be offset by revenue gains. The changes enunciated by the TRA'1986 with respect to corporate taxation were as follows:

- The top marginal rate was lowered to 34 percent from 46 percent, though rates of 15 percent and 25 percent existed for taxable income less than $100,000.

- The definition of business taxable income was broadened, with provisions that postponed the recognition of expenses (e.g., bad debt charge-off, uniform capitalization for inventories, lengthened depreciable lives for business assets, repeal of investment tax credit).

- The corporate alternative minimum tax was expanded by subjecting to immediate taxation a portion of economic income that was not otherwise included in the regular taxable income.

- The repeal of the General Utilities doctrine, which had allowed, in certain circumstances, a tax-free distribution of corporate assets in a liquidation.

- The Act repealed the General Utilities doctrine, which meant corporations were no longer able to avoid the recognition of gain on certain qualifying dividend distributions or on distributions or sales of appreciated property in connection with a complete liquidation.

See Also: What Happened To All The 'Shovel-Ready' Infrastructure Projects From The 2009 Stimulus Bill?

No Massive Economic Effects Despite The Hype

According to taxhistory.org, the 1986 reforms, though reducing the wide disparities in the tax burdens of companies in different industries and improving allocation of resources and the efficiency of the use of capital, didn't bring about massive economic effects. Even a marked reduction in the maximum individual tax rate to 28 percent did not produce major economic significance.

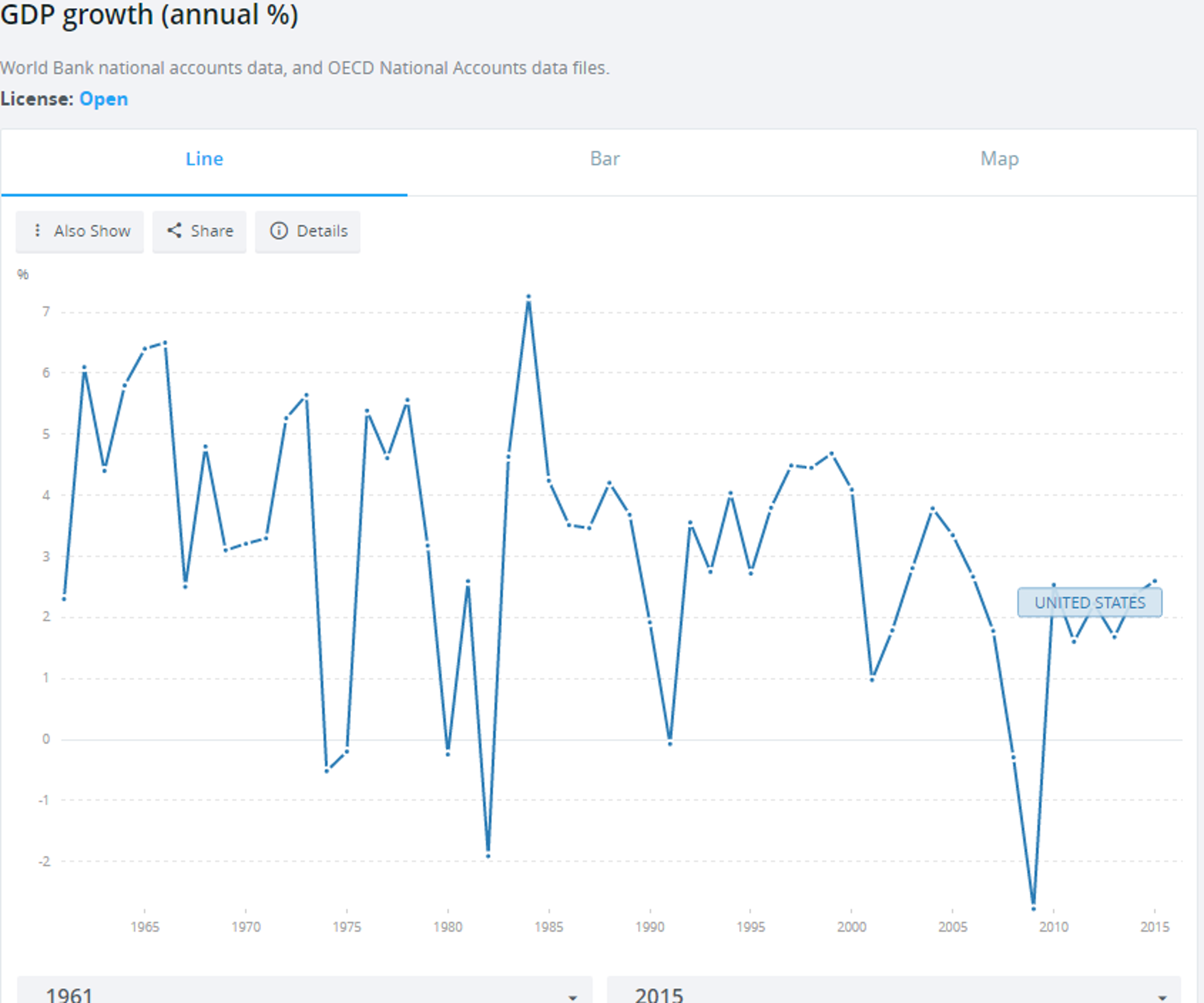

World Bank estimates show that the U.S. GDP economy, though seeing a short spike in growth in 1988 following the implementation of the 1986 tax reforms, slipped into a recession in 1990–1991. In fact, the recession was blamed in part to the 1986 tax reforms, which busted the real estate boom, resulting in sinking property prices, lower investment incentives and job losses. The economic weakness in the run up to the recession was also due to the restrictive monetary policy of the Federal Reserve, which was at that time obsessed with inflation fighting.

A research paper published by the National Bureau of Economic Research noted corporate tax receipts had increased only less than expected in the aftermath of the TRA'1986. The bureau attributed the softness to lower corporate profits, a higher share of corporate interest payments of the corporate operating income and the rapid growth in subchapter S corporations.

In the long run, the TRA'1986 could not hold its own and many of the reforms were reversed. Since then, the tax base has narrowed and income tax rates have risen.

Visit BZTeach for more awesome educational content!

Image Credit: By White House Photo Office - Direct link: here and here, Public Domain, via Wikimedia Commons

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.