In recent weeks, the energy sector has found itself squarely in the limelight, fueled by fluctuations in oil prices and a resurgent interest in heating oil. As we transition into the cooler seasons, liquefied natural gas (LNG) is poised to seize a substantial portion of this spotlight. Factors such as volatile inventory levels in the EU, labor disruptions in essential supply hubs, and simmering geopolitical tensions, gives credence to a pressured price landscape.

It is imperative to note the distinct difference between liquefied natural gas and its natural form counterpart. Although high demand in one may correlate momentum in the other's price, it is not a guaranteed event and that cannot be emphasized enough.

Liquefied natural gas emerges through the cooling of natural gas to a chilling -260 degrees Fahrenheit, a process which transforms the gas into a liquid, decreasing its volume over 600 times compared to its gaseous form. Primarily, LNG is shipped using specially designed vessels to nations reliant on this critical energy source, with a fair amount of supply also retained for power plants to leverage during periods of heightened electricity demand.

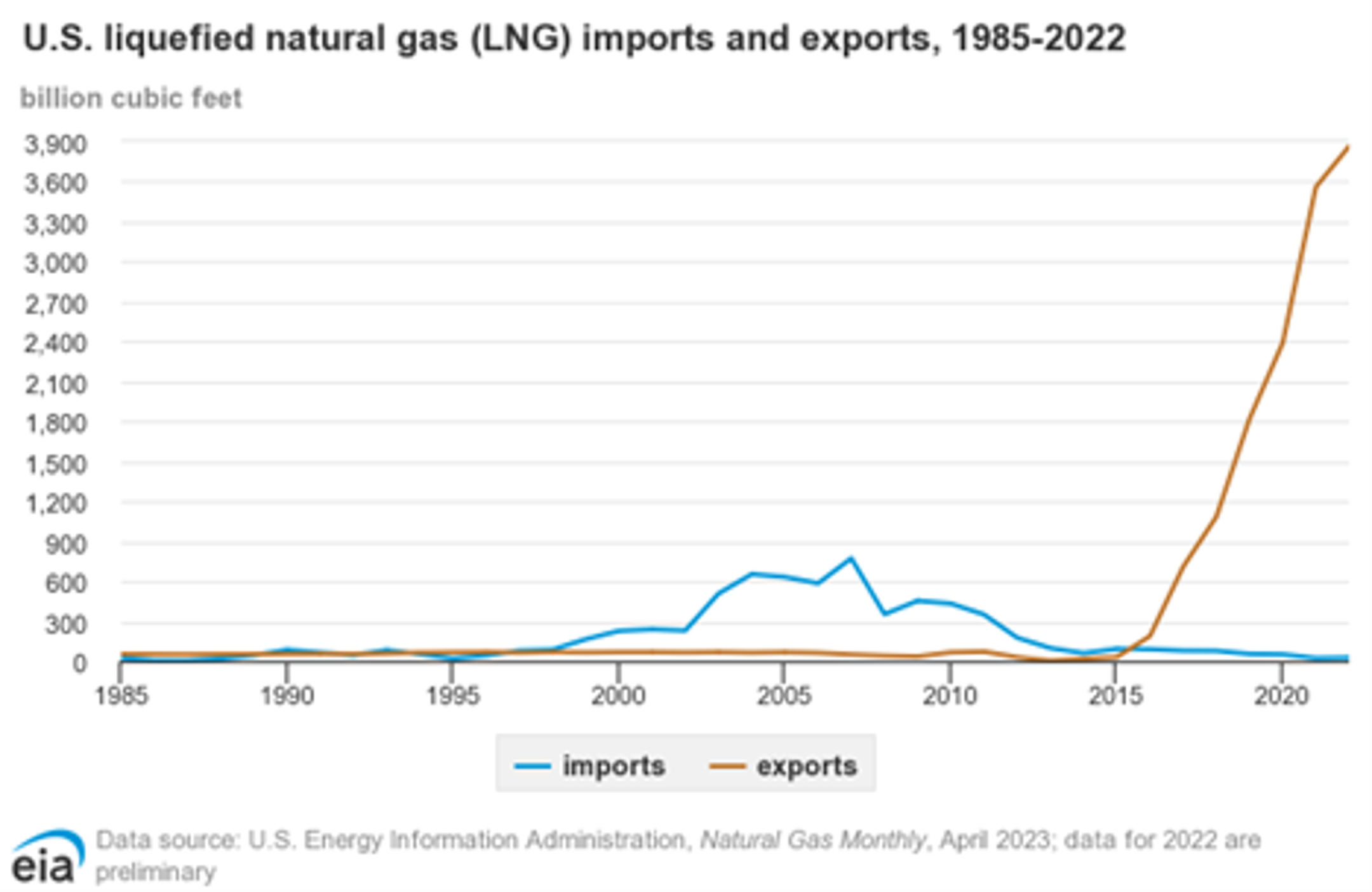

The U.S., a major player in the global LNG market, exported a remarkable 3.8 trillion cubic feet of LNG in 2022 according to the Energy Information Administration. Traditionally countries fill their reserves during warmer months when demand for the commodity is low, then draw on those inventories during the cooler months as demand increases.

Last week, the EU experienced a substantial dip in LNG inventories exceeding normal seasonality factors. This drawdown, coupled with Chevron Australia’s LNG strikes that began on September 8th, which may impact 5-10% of global supply, resulted in a spike in the price of UK Natural Gas by 13% and Henry Hub futures by 3.69%.

Wrap Up

Inventory levels can fluctuate due to production levels, weather, and geopolitical tensions, especially in relation to the European Union. Although Russia natural gas piped to the EU has been reduce due to Nord Stream being offline and voluntary reductions, it is still a key lever they may utilize to put pressure on the EU as the Russia/Ukraine conflict continues to show incremental gains for Ukraine.

Natural gas import volume from Russia in the European Union (EU) and the United Kingdom (UK) from 2021 to 2023 (Statista)

The unfolding scenario doesn’t automatically translate to gains for every energy company with natural gas exposure or even natural gas futures contracts for that matter. Giants like Chevron CVX and ExxonMobil XOM with their expansive portfolios might have limited exposure to LNG in relation to their total revenue mix. Specialized players such as Cheniere Energy LNG and Shell SHEL are positioned to capitalize on the benefits from a surge in demand in the coming months.

Just remember, natural gas is a difficult market to navigate and due diligence is paramount to capitalize on the opportunities. Just something to keep your eye on.

Follow Kevin Green on X (Formally Twitter)

Additional content on the Schwab Network

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.