Over the past five trading sessions, crude oil has gained significant attention from traders and investors. Crude oil prices have plummeted over 12% since briefly touching the $95.03 mark. I've delved into the fundamental landscape for this pullback: Producers are lessening their short positions, signaling decelerating demand in the marketplace. Managed money inflows are causing heightened volatility and instability in pricing. There are also refining challenges for certain byproducts like diesel and heating oil, among others. However, this sharp price decline has also fostered a historically significant dynamic within economic cycles, potentially hinting at future shifts in rates.

Crude/RBOB gas spreads have collapsed, compelling refiners to make pivotal decisions in the coming weeks. They might either pivot to distillates such as diesel or heating oil while the spreads remain favorable, although possibly incurring higher operational costs due to a limited supply of sour crude. Otherwise, they could continue slashing refinery utilization rates, a move that might prove costly to recover from once a balance is established. Regardless, we might be witnessing demand destruction in real-time — a primary goal of the Federal Reserve.

Broadly speaking, refiners profit by purchasing oil and transforming it into other byproducts like gasoline, diesel, heating oil, jet fuel, and numerous petrochemicals. The gap between the obtaining cost of the oil and the sale price of these byproducts — commonly referred to as the spread or margin — is the cornerstone of profitability for energy corporations. As this margin shrinks for specific products, major energy entities like ExxonMobil XOM and Valero VLO recalibrate their refining processes to cater to market demands for other profitable byproducts.

Unfortunately, recent editions of the U.S. Energy Information Administration’s Weekly Petroleum Status Report have reflected a decrease in refinery capacity utilization rates. Additionally, there's been an unexpected surge in motor gasoline inventories, currently surpassing the five-year average for this period by 1%.

Typically, refinery utilization rates dip as refineries switch to winter-blend gasoline, and demand generally weakens. But currently, certain market segments, like distillates, aren't experiencing the anticipated supply boost, partly attributable to the scarcity of heavier or sour crude, vital for refining distillate. The report from September 29th highlights that distillate fuel stockpiles are roughly 13% below the five-year average for this season.

The Gulf Coast PAD District's persistent unseasonal reductions in percentage utilization rates have affected the production of Distillate fuel oil. The market witnessed an 8.75% week-over-week production slump and a 13% year-over-year production decrease.

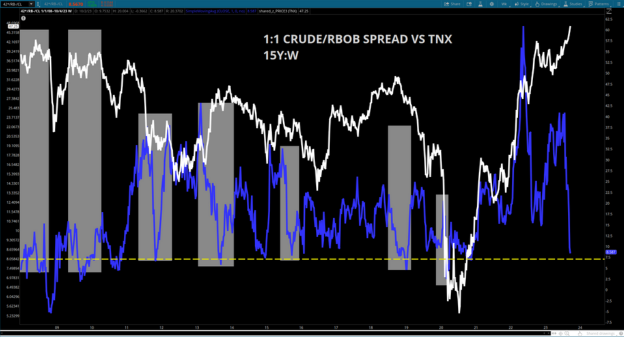

The chart below illustrates the 1:1 spread between one barrel of crude oil and the 42 gallons of gasoline that can be derived from it. While this isn't the typical crack spread that traders frequently discuss, it mirrors a similar principle that energy companies prioritize. Over the past two months, there's been a marked contraction in this spread, indicating dwindling profitability for refiners looking to ramp up gasoline production. Interestingly, this dip also correlates with the 10-year treasury yield, a pressing matter in the present market. Historically, a substantial spread decline between crude oil and gasoline has signified notable demand destruction, typically followed by a decrease in treasury rates after 3-6 months. This setup might be crucial for the Fed, which has been grappling with inflation concerns. It could be a reprieve for those affected by the swift surge in yield markets. In fact, the current spread correction is one of the most pronounced since 2008.

Now, the supply dynamics are distinct from past scenarios. Geopolitical tensions have profoundly reshaped energy supply chains, and energy companies are now prioritizing shareholder returns over capital expenditure. Yet, this situation still warrants attention.

Factors To Consider

Saudi Arabia has unveiled plans to maintain their 1 million barrels per day (bpd) supply cut for the rest of the year, a move that the market might have already factored in. This could hint that we might be witnessing real-time demand erosion, with concerns about further reductions potentially plunging the global economy into a recession-like state. A potential counter to this trend could be Russia lifting its diesel exports ban, thereby adding supply to countries such as China and India and alleviating global market pressure. Russia imposed this ban in response to domestic supply shortages amid the ongoing Russia/Ukraine conflict.

All in all, producers stand at a juncture. They can either modify their refining strategy to capture the lucrative spreads in the distillate market or maintain their current supply-limited stance, hoping to uphold operational margins. Either path poses risks of price declines due to either additional supply entering the market or plummeting demand. Something to keep your eye on.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.