American Express Co AXP reported better-than-expected sales for its fourth quarter on Friday.

The company posted fourth-quarter revenue (net of interest expense) growth of 9% year-on-year to $17.18 billion, topping the analyst consensus estimate of $17.16 billion. The increase was primarily driven by strong Card Member spending, higher net interest income supported by growth in revolving loan balances, and accelerated card fee growth.

GAAP EPS of $3.04 was in line with the analyst consensus estimate.

Chair and CEO Stephen J. Squeri flagged record levels of annual Card Member spending, record net card fee revenues, and a record 13 million new card acquisitions in 2024 and continued to add millions of merchant locations to its network globally.

Amex said it expects FY25 revenue of $71.22 billion-$72.54 billion (up by 8%-10% Y/Y) versus a consensus of $71.28 billion. It expects EPS of $15.00–$15.50 versus the consensus of $15.23.

Amex shares fell 1.4% to close at $321.34 on Friday.

These analysts made changes to their price targets on Amex following earnings announcement.

- Morgan Stanley analyst Betsy Graseck maintained American Express with an Equal-Weight and raised the price target from $305 to $310.

- Keefe, Bruyette & Woods analyst Sanjay Sakhrani maintained American Express with an Outperform and raised the price target from $350 to $360.

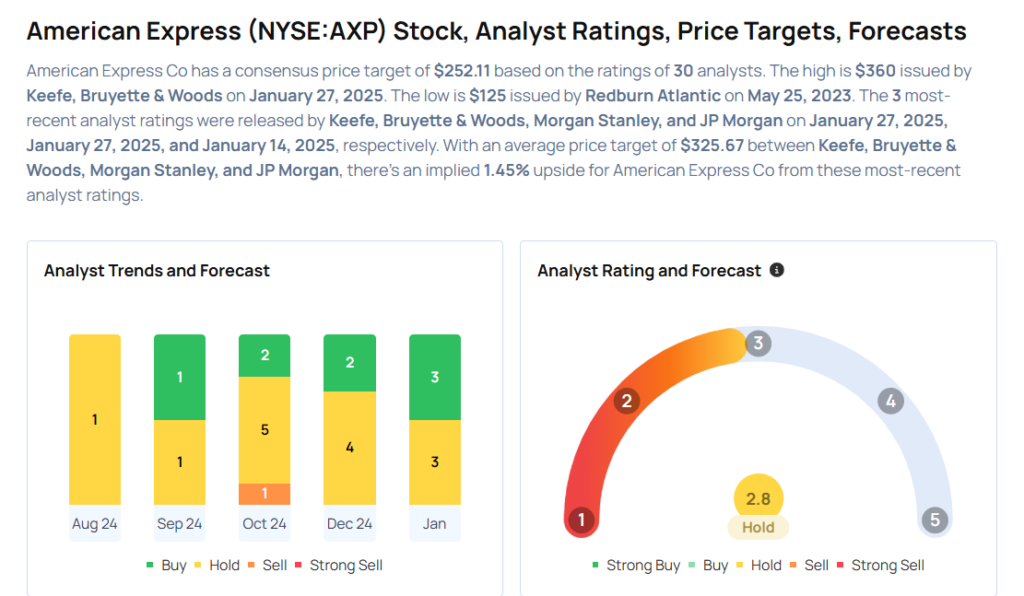

Considering buying AXP stock? Here’s what analysts think:

Read This Next:

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.