Eye Of The Storm

(BN) Republicans Will Lose Spin War Over Shutdown: Jonathan Bernstein

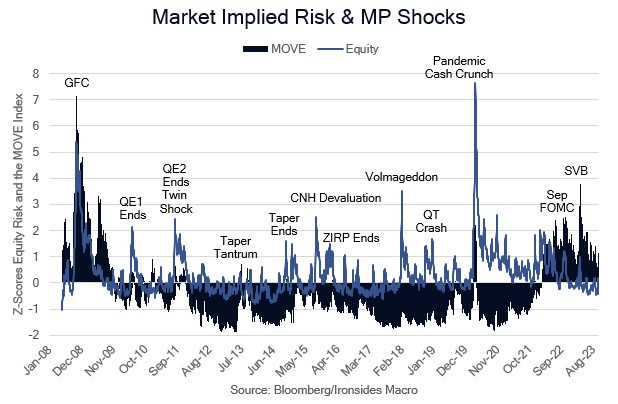

Figure 1: This is an aggregate of several measures of equity volatility, there are no signs of defensive positioning.

© 2026 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

To add Benzinga News as your preferred source on Google, click here.