Make no mistake, the FOMC pivoted last week from the September meeting’s ‘hawkish hold’ due to the second wave of the supply-driven bear steepening of the Treasury curve and associated damage to bank capital. Even the most hawkish FOMC participants (Bowman, Waller, Logan) softened their stance on additional hikes. The justification for the pivot was characterized as an increase in term premium with a few FOMC participants intimating the increasing risk of holding longer UST maturities was attributable to the increase in Treasury supply. The September FOMC summary of economic projections policy rate forecasts were the third miscalculation of the tightening process that led immediately to a disorderly tightening of financial conditions.

The first was in September ‘22, which saw a third 75bp hike combined with an 80bp increase in the terminal policy rate even as inflation had peaked. The risks were clear, China was still following its futile zero Covid policy and Europe was on the verge of a major energy crisis. The market response was swift, the Japanese were forced to intervene to stabilize the yen the morning after the meeting, the pound had a flash crash 4 days later and the mortgage market was virtually ‘bid-less’ the following Monday. Next up was an overreaction to the January ‘23 employment report and revisions to CPI at the semiannual monetary policy report, when Chair Powell threatened to reaccelerate the pace of tightening. Days later three banks were under FDIC supervision.

Ahead of the September ‘23 meeting we incorrectly assumed the Committee understood the risks of a bear steepening yield curve disinversion. It seemed obvious that the 30% of bank assets held in securities took a major hit during the August supply-driven bear steepening. The S&P Regional Bank Index declined 15% from the late July peak through the beginning of the meeting in lockstep with long maturity Treasury prices, and the fifth sentence of the staff’s summary of developments in financial markets noted the decline. We thought the FOMC wouldn’t risk another disorderly tightening, but once again the ghost of Arthur Burns appears to have led the FOMC into a communication error.

Despite the Fed’s pivot from their communication error, the Treasury auctions still went poorly this week. The first 60bp of the increase in 30-year real rates (TIPS) in August was primarily attributable to increased supply, the next 40bp was the Fed’s communication policy exacerbating the fiscal imbalance. Using the ACM term premium model, 10-year term premium increased 55bp in August and another 53bp following the FOMC meeting. Taking a hike in November off the table does not resolve the supply problem or reverse the damage to bank capital we are likely to learn more about next week during regional bank earnings. It is merely a decent first step that effectively acts as a partial hedge against a continuation of the disorderly bear steepening. Building on this idea, the partial pivot is a necessary, but not sufficient, condition for favorable seasonality and the end of the earnings recession to trigger a rally back to the July 4600 S&P 500 high, or our original 4800 year-end target. A more definitive end to the hiking cycle, regional banks muddling through earnings season and indications from corporate results that productivity is accelerating, would all help. Chronically optimistic equity investors, who — unlike bond investors — can get better than par, are often guilty of looking for silver linings behind every dark cloud. The silver linings — end of the earnings recession, seasonality, capital spending and productivity booms — are out there, but fiscal and monetary policy drags are intensifying despite the FOMC’s partial pivot this week.

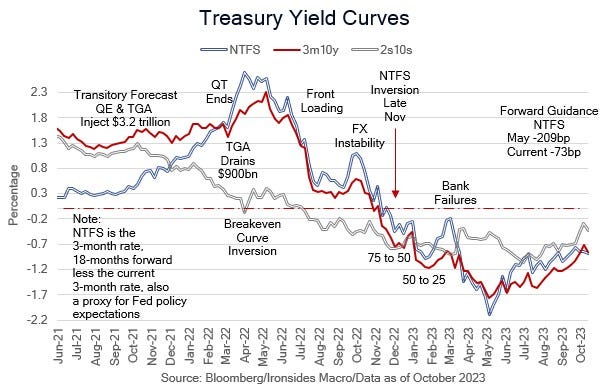

Figure 1: Curves have steepened but remain deeply inverted. If the bear steepening extends with 10s and 30s exceeding 5%, losses in the banking system will deepen.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.