Monetary Policy Report To Congress

It is crunch time for our ‘Quadrilemma’ thesis, which is our view that in order for the Fed to cut to 4% in ‘24, the level required to painlessly disinvert the 3m10y yield curve with a 10-year Treasury near 4% that will reopen regional bank credit channel, the unemployment rate needs to exceed 4% and wage growth cool below 4%. The Treasury market absorbed massive supply in the soft underbelly of the curve (2s, 5s and 7s) partially on hopes that the hot January inflation and employment data was distorted by seasonal adjustment factors corrupted by the pandemic and the data will cool in coming months. We are sympathetic to that view, however, as we will discuss we are less sanguine than FOMC participants or most street forecasters about the longer-run inflation and natural (r*) rates.

Expect the financial news and street research to focus on rate policy ahead of Chairman Powell’s Semi-Annual Monetary Policy Report to Congress on Wednesday and Thursday. However, the more important theme could be Republican Senators airing grievances over the Administration and the regulatory proposals of their appointees, including Fed Chair for Bank Supervision Barr, FDIC Chair Gruenberg, and acting Comptroller of the Currency Hsu.

Fed Governor Bowman provided a preview this week with a warning of the macro implications of these proposals, that include an increase in the GSIB (largest banks) surcharge, Basel III endgame rules, long-term unsecured debt requirements for banks with more than $100 billion of assets, CRA rules, restrictive mergers & acquisition reviews, climate change, interchange fees and liquidity requirements. These policies threaten to return banks to the 2014-2018 and 1950’s excessive regulatory regime that capped return on equity at 10%, thereby impairing the flow of credit leading to uneven economic activity and weak capital investment, not to mention poor stock price performance. Of course, even if Chair Powell comes down on Barr’s side in the dispute with community banker board member Bowman and pushes through these excessive and poorly constructed proposals, a Republican controlled White House will reverse these rules in short order.

The first two months of 2024 are in the books. Hotter than expected inflation and employment data led to a convergence of market expectations for a year-end monetary policy rate of 4% and the December FOMC Summary of Economic Projections forecast for a 4.75% rate. We frequently hear the markets looked right through what was expected to be a wrenching process. We view that take as simplistic, in fact the Treasury curve is 40bp higher, the S&P Regional Bank ETF fell 8.2%, the Russell 2000 is underperforming the S&P by 5.5%, while the S&P 500 Information Technology and Communication Services sectors both rallied more than 10%. In other words, the unstable equilibrium between the rate insensitive household and large nonfinancial corporate sectors on the one hand, and inverted yield curve sensitive regional banks and their real estate and small business customers on the other, has persisted for nearly a year. For our part, we continue to lean into the unstable equilibrium: we are underweight duration, financials, small caps, rate sensitives and defensives sectors and long technology and related sectors along with industrials, energy and materials. This week we got our first acknowledgement from an FOMC participant (see below) that the Fed’s reckless accommodation in ‘21 and clumsy tightening in ‘22 and ‘23 that caused the deepest yield curve inversion since Volcker’s policy did irreparable damage to the Savings & Loan industry.

In this week’s note we update our bills only Fed balance sheet outlook, ‘Quadrilemma’ thesis ahead of the February employment report, update our inflation outlook, and look at the strength of the recovery in earnings from the 4Q22-2Q23 earnings recession. Our director of research, at Barclays, Stu Linde (RIP), would scold us for covering this much ground in a weekly note, but we had a lot to say.

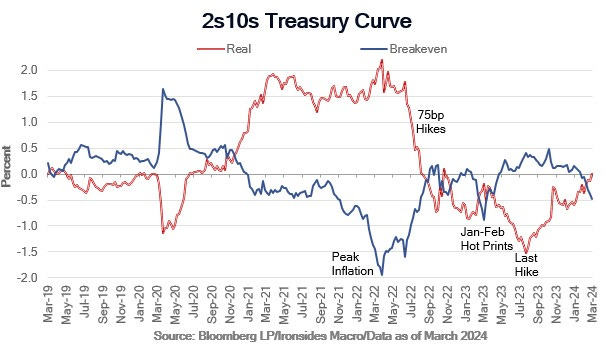

Figure 1: Although the level of breakeven inflation (nominal Treasuries less inflation protected yields) is lower than it would be otherwise if the Fed did not hold ~25% of the Treasury market, the breakeven curve accurately forecasted peak CPI and the early ‘23 scare. The curve is giving a similar forecast currently. While we agree the hot January reports are unlikely to persist through spring, we expect the Fed’s 2% target to prove elusive.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.