CME has launched a new online tool to gain further transparency in to the FX marketplace and to highlight potential investment opportunities that are available via CME Listed FX products. The FX Swap Rate Monitor provides current and historic FX Link pricing and bid/offer spreads as well as interest rate differentials for eight currency pairs as implied by CME FX Futures and FX Link markets.

FX swaps, which are essentially funding transactions, are the largest segment of the OTC FX market. According to the latest BIS Triennial Central Bank Survey, FX swaps trading accounts for nearly 50% of the global FX market – with a value of $3.2 trillion traded every day. Despite this size, FX swaps do not have a primary market venue where firm executable prices are publicly viewed. Instead quotes are typically provided on a private bilateral basis or if public on an indicative basis.

The short-term funding rate generated by an FX swap can often differ from the combined nominal interest rates quoted for each currency, which in turn creates an advantage for entering the market to obtain improved investment returns.

CME FX Link provides an alternative to bilateral FX swaps that is available in a central limit order book on a credit agnostic, all-to-all basis with truly firm pricing. It combines an OTC spot transaction on the near leg with a centrally cleared and capital efficient FX Future on the far leg. FX Link currently supports eight currency pairs, which combined account for 69% of the FX swaps market according to the latest BIS survey*.

*Source: BIS 2019 Triennial Central Bank Survey of Foreign Exchange and Over-the-counter (OTC) Derivatives Markets.

| Example: USD/JPY | |

|---|---|

| CME JPY/USD Jun20 futures | |

| Futures Mid: FX Link Mid: Implied Rate Differential: |

0.009335 -0.038 0.43% |

| 1-month USD ICE LIBOR: 1-month JPY ICE LIBOR: Short term rate differential: |

0.18% -0.06% 0.18% - -0.06% = 0.24% |

| Effective FX Link USD Return | 0.43% + -0.06% = 0.37% |

| FX Link USD Yield Enhancement | 0.37% - 0.18% = 0.19% |

Worked Example – looking at USD/JPY: On May 14 2020, the FX Swap Rate Monitor quoted a rate of 43 basis points for the JPY/USD market referencing the June 2020 futures expiry. This indicates that, were covered interest parity to hold, rates of return in US dollars ought to be 43 basis points higher than rates of return in Japanese yen which isn’t unreasonable with yen interest rates in negative territory. We can compare this differential with cash market returns, using 1-month ICE LIBOR1 as a proxy. The differential between 1-month USD ICE LIBOR and 1-month JPY ICE LIBOR, when expressed in the same terms, was 24 basis points. This spread of 19 basis points (i.e. 43 minus 24) is therefore the potential enhanced return made available by transacting an FX swap using the FX Link trading mechanism, although it should be noted that other costs such as the bid-ask spread also need to be considered.

To take advantage of the 19 basis point yield improvement, a US dollar based investor can use FX Link to buy yen and simultaneously buy JPY/USD futures to lock in the FX swap rate of 43 basis points. Yen can then be invested in the local market, where the return (as indicated by 1-month JPY ICE LIBOR) is minus 6 basis points. After one month, this position can be reversed via FX Link – closing the futures position whilst simultaneously switching yen back into dollars on the spot leg. This results in a net return of 37 basis points, before costs, which is greater than the 18 basis points quoted as the prevailing 1‑month USD ICE LIBOR rate.

| Example: AUD/USD | |

|---|---|

| CME AUD/USD Jun20 futures | |

| Futures Mid: FX Link Mid: Implied Rate Differential: |

0.6312 -0.0001 -0.10% |

| 1-month USD ICE LIBOR: 1-month AUD BBSW: Short term rate differential: |

0.72% 0.09% 0.72% - 0.09% = 0.63% |

| Effective FX Link AUD Return | 0.72% - -0.10% = 0.82% |

| FX Link AUD Yield Enhancement | 0.82% - 0.09% = 0.73% |

Worked Example – looking at AUD/USD: On April 16 2020, the FX Swap Rate Monitor quoted a rate of -10 basis points for AUD/USD market referencing the June 2020 futures expiry. This indicates that, were covered interest parity to hold, rates of return in US dollars ought to be 10 basis points lower than rates of return in Australian dollars. We can again compare this differential with cash market returns, using 1-month USD ICE LIBOR and 1-month BBSW as a proxy. The differential between 1-month USD ICE LIBOR and 1-month BBSW, was 63 basis points. This spread of 73 basis points (i.e. 63 minus -10) is therefore another example of an enhanced return made available by the FX Link trading mechanism.

In this scenario, to take advantage of the yield improvement, an investor can use FX Link to switch borrowed Australian dollars into US dollars and simultaneously buy AUD/USD futures to lock in the FX swap rate of -10 basis points. The US dollars are then invested with a return of 72 basis points (as indicated in by 1-month USD ICE LIBOR). After one month, the position can be unwound - using FX Link to close the futures position and simultaneously purchasing Australian dollars in exchange for US dollars. The borrowing costs of 9 basis points (as indicated by 1-month BBSW) are more than covered by the result.

The position held in FX futures hedges the exposure to outright moves in the FX market, but as the investor has an exposure to the FX basis, this needs to be monitored.

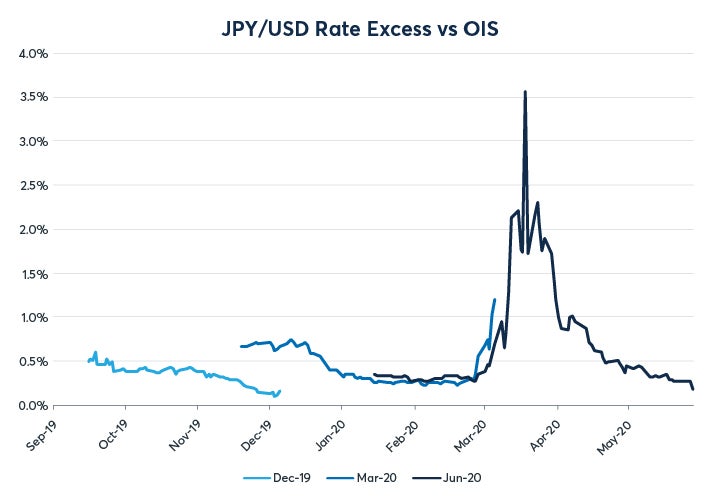

Further Analysis – Impacts of COVID-19 on JPY/USD: As the implications of the pandemic hit the markets in March 2020, FX swaps and FX futures prices became heavily affected by funding requirements and currency repositioning strategies. Demand for dollars in the spot market resulted in a spike in FX swaps rates, and the FX swap returns implied by FX Link can again be compared to the differences in 1-month ICE LIBOR.

Focussing on the spread between these two markets highlights that at a point during the crisis there was an excess yield of approximately 2.6% available in the FX Link marketplace.

What has also been widely observed during this period is that USD ICE LIBOR itself had an increased spread to OIS rates. Comparing FX returns available in FX Link and the spread of 1-month OIS rates highlights an even greater dislocation in FX swaps rates to the short term rates markets, and covered interest parity.

Further Analysis – Impacts of COVID-19 on EUR/USD: A similar analysis can be made of EUR/USD, and the following chart describes the excess of the FX swap rate over the interest rate differential between 1-month USD ICE LIBOR and 1-month EURIBOR. As can be seen, by early April the increase in USD ICE LIBOR in comparison to other rates, had moved the excess FX swap returns into negative territory. As with the Australian dollar example earlier in this paper, moving funds from euros into US dollars – managed and hedged via FX Link – could have enabled an investor to help manage their risk better.

In Summary: The FX Swap Rate Monitor brings greater transparency to the FX swap market and helps to inform potential cross currency investment choices. The tool provides both current as well as historic data for eight currency pairs, and the examples in this paper help illustrate how this data can be used to better understand each market.

By July 2020, market volatility has decreased relative to the levels seen in March and April, and the excess returns highlighted by the FX Swap Rate Monitor were returning to pre-crisis norms. Whilst it should not be expected (or maybe indeed, hoped for) to see excess returns as substantial as those identified in the charts above, the FX Swap Rate Monitor will continue to provide valuable analysis and transparency into CME’s FX markets.

To learn more about futures and options, go to Benzinga’s futures and options education resource.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.