Exacerbating Excess Treasury Supply

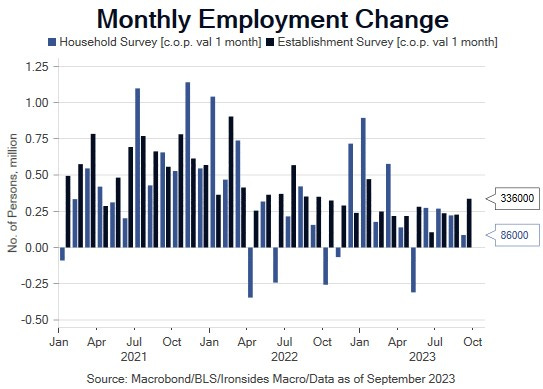

There was a lot riding on the September employment report and the headline was shockingly strong. That said, the broadest measure of labor market demand, the aggregate hours index, increased 0.2% from August and for 3Q it increased at a 1.7% annualized rate. Thes is a pace that implies — given GDP tracking estimates — a second robust increase in productivity, a topic we will discuss in our earnings preview later in the note. In our payroll preview note, we had a strong conviction that soft wage growth would be soft, and that there would not be a retracement of the 0.3% increase in the August 3.8% U3 unemployment rate. The soft wage data and higher than consensus unemployment rate is a something of a pyrrhic victory, given the shockingly strong headline increase in nonfarm payrolls. We had lower confidence in our expectation for a soft net change in payrolls; eight consecutive months of net revisions was a key element of the softening trend. At first glance, the 336,000 increase in nonfarm payrolls and a 119,000 positive revision to the last two months appeared to reverse a trend that persisted for all of 2023. Turns out, all the revisions were in government jobs and for the quarter, full time jobs contracted 692,000 (-585,000 in July, -85,000 in August and -22,000 in September) and part-time jobs increased 1,155,000 (similar pattern). We will dig deeper into this later in this note, however, the more you look at the report, the more the headline looks misleading. Indeed, as the morning progressed, and investors dug into details, equities rallied, and Treasuries stabilized. That said, the September FOMC meeting put the Committee on a path for a November rate hike unless the growth and employment outlook deteriorated and the two big numbers of the week, JOLTS and Employment, had very strong headlines for job openings and nonfarm net payrolls. The price action implied markets expect the FOMC to pivot back to the disinflationary path to curve disinversion, however we remain concerned that they can wiggle out of the forward guidance straitjacket so easily.

Figure 1: The strength in nonfarm payrolls was mostly government jobs, the headline was almost as misleading as January’s. That report, and some similarly misleading inflation reports almost convinced the Fed to reaccelerate the hiking pace until the bank failures.

By early Friday morning, following the employment report the 30-year real rate (TIPS yield) was 100bp above the late July, pre-Treasury financing announcement, level. We were asked to decompose the move in rates this week. Using the part of the curve least impacted by the Fed’s balance sheet or rate policy, 30-year real rates, the first 60bp occurred in August in response to $500 billion of unexpected supply. To be sure other factors (including Bank of Japan yield curve control loosening) contributed to the move. The next 40bp followed the September FOMC ‘hawkish hold’; in our view the Fed’s forward guidance straitjacket exacerbated the fiscal imbalance. On the current path, a 5+% policy rate for 15 months, in addition to the damage to all but the largest banks in the system, implies Treasury forced to finance interest expense. At the expense of redundancy, let’s consider the potential paths to curve disinversion. The benign best-case outcome is a disinflationary bull steepening driven by Fed 2024 rate cuts. Disinflation was the dominant macro theme in 1H23, unfortunately the September FOMC Summary of Economic Projection policy rate and inflation forecasts inferred the Committee assigned a low probability to this outcome. The worst-case scenario is the insidious bear steepener. We are now two months into this outcome, it is a risk-off, stocks down, bonds down outcome. We suspect there are losses that have not yet surfaced, and both the banking system and nonbank finance are obvious areas of vulnerability. Earnings season, beginning on Friday the 13th, could uncover some of the losses. The final path is a bull flattening where the Fed cuts rates in ‘24 due to deterioration in their full employment mandate. This is a stocks down, bonds up outcome that the September FOMC forecasts, press conference and subsequent speeches imply the Fed believes is necessary to avoid the Ghost of Arthur Burns Second Great Inflation.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.