CPI inflation for May comes out at 830am. Here are Wall Street estimates:

-

GOLDMAN SACHS: 4.2%

-

UBS: 4.1%

-

MORGAN STANLEY: 4%

-

JP MORGAN: 4.2%

-

BARCLAYS: 4%

-

VISA: 4%

-

BLOOMBERG: 4%

-

ME: Still too damn high

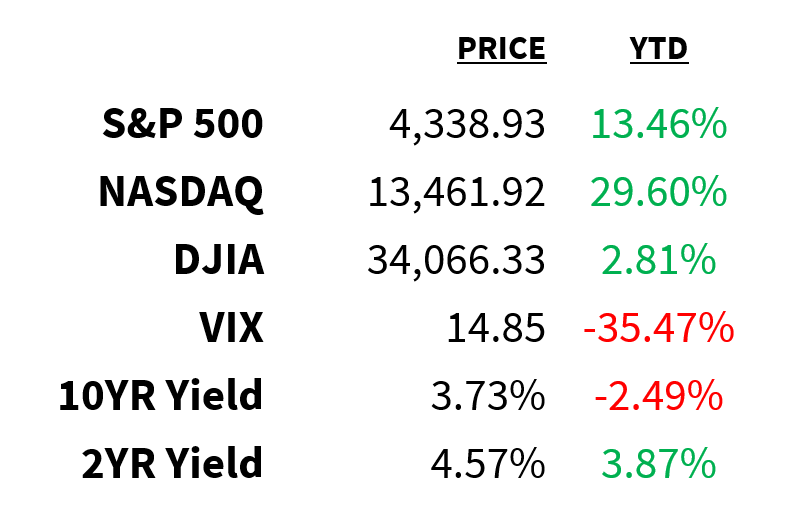

Market

Prices as of 4 pm EST, 6/12/23

Macro

The US government spent more than it earned in May…by a lot.

-

Revenues fell 21% YoY to $307 billion while outlays–led by Medicare spending–rose 20% to $548 billion.

-

The resulting $240 billion budget deficit for the month was more than double the deficit in May 2022.

-

For the fiscal year, the gap has widened to $1.16 trillion, a 191% jump from a year ago.

This year has already seen more debt defaults in the US junk loan market (in number and total value) than all of 2021 and 2022…combined.

-

A rapid rise in interest rates over the past year has left junk-rated companies–many of which had loaded up on leveraged loans at floating rates–facing higher interest payments as slowing economic growth caps earnings.

-

Last month alone saw $7.8 billion in defaults, the highest since the pandemic.

-

Looking ahead, more defaults are expected as the Fed keeps interest rates higher for longer.

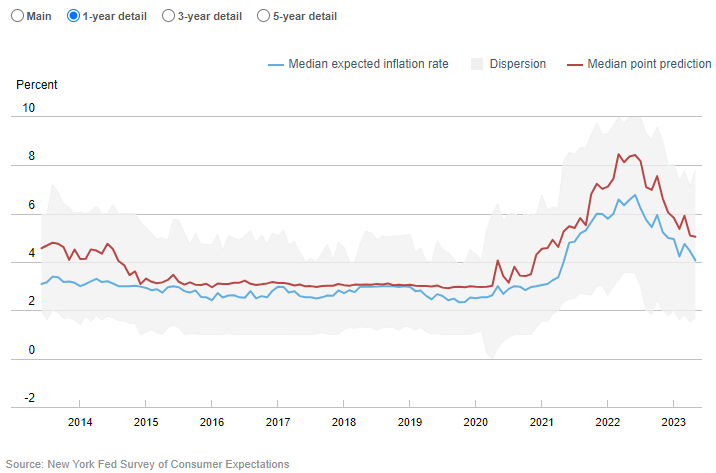

Consumers are becoming more optimistic about inflation.

-

The NY Fed’s Survey of Consumer Expectations for May revealed short-term (1-year ahead) inflation expectations dropped to the lowest since May 2021 at 4.1%.

-

Medium- (3-year) and long-term (5-year) expectations, on the other hand, ticked up by 0.1% each to 3% and 2.7%, respectively.

-

The survey also showed consumers are less optimistic about wages with one-year expected earnings falling to 2.8% from 3%.

-

Meanwhile, their expected odds of being laid off dropped by 1.3% to the lowest since April 2022.

Stocks

Shares of Tesla advanced for the 12th straight day yesterday, marking the stock’s longest daily winning streak ever.

-

Driving the gains were announcements from three charge makers–ChargePoint, EVgo, and Blink Charging–who say they will adopt the EV maker’s charging technology.

-

This comes after GM and Ford recently agreed to embrace Tesla’s North American Charging Standard (NACS).

-

However, according to industry body CharIN–which promotes the Combined Charging System (CCS) standard–Tesla’s charging model is not yet a standard because it doesn’t provide an open charging ecosystem for the industry.

A pair of index-outperforming sectors are poised for continued gains, according to analysts.

-

Still well below their pre-pandemic highs, cruise line stocks are gaining momentum.

-

Analysts from BofA and JPMorgan point to pent-up demand and strong bookings across the cruise industry coupled with low cancellations as reasons for continued outperformance among cruise operators.

-

-

Among the year’s leaders, homebuilder stocks are also expected to build on their strong YTD performance.

-

Analysts at Citigroup cite strong buyer demand, stable home prices, tight inventories, and a potential pause in rate hikes as catalysts for the group.

-

The S&P 500 and Nasdaq closed at their highest levels since April 2022 yesterday.

-

The rally is forcing investors off the sidelines, lest they miss out (aka FOMO is kicking in).

-

According to Deutsche Bank, positioning among discretionary investors has emerged into overweight territory for the first time in more than 16 months.

-

The same can be said for consolidated equity positioning which is now in the 54th percentile.

-

Pair that with increasingly bullish investor sentiment and “risk-on” has been activated across many corners of the market.

Goldman Sachs

Energy

Oil traders are still ignoring Saudi Arabia’s production cuts.

-

Front-month Brent futures fell yesterday to their lowest since December 2021 as better-than-expected production and weak demand weigh on prices.

-

Prices for WTI crude are down ~11% since the end of March (just before OPEC’s surprise production cut).

-

Meanwhile, the EIA predicts US oil output will reach a new record in July, rising to 9.38 million barrels per day.

John Kemp

Earnings

Yesterday’s highlights:

Oracle ORCL: $1.67 EPS (vs. $1.58 expected), $13.84 billion in sales (vs. $13.74B expected).

-

The company offered quarterly revenue guidance above analysts’ expectations but fell short of their consensus for earnings.

-

Board chairman and CTO Larry Ellison said Oracle would introduce a generative AI cloud service–similar to Microsoft’s Azure OpenAI Service–in partnership with startup Cohere.

What we’re watching today:

-

Burford Capital BUR

-

Top Headlines

-

Survey says: BofA’s latest Global Fund Manager Survey reveals long Big Tech is by far the most crowded trade.

-

Next-gen: Shares of Toyota popped after the company announced plans to introduce a full lineup of EVs with next-generation batteries.

-

Google ads: EU antitrust regulators are exploring a breakup of Google’s ad-tech business as part of a new antitrust complaint.

-

ESG talk: The number of SPX companies mentioning “ESG” on earnings calls has reached its lowest point since Q2 2020.

-

Cardboard indicator: Shipments of empty boxes fell 11% YoY in March, pointing to a slowdown in consumer spending.

-

JPM settles: JPMorgan agreed to a $290 million settlement with Jeffrey Epstein victims.

-

Growth concerns: China’s central bank surprised markets by cutting a short-term policy interest rate.

-

BoE pressure: A surprise jump in UK wage growth and employment puts pressure on the Bank of England to raise interest rates to battle inflation.

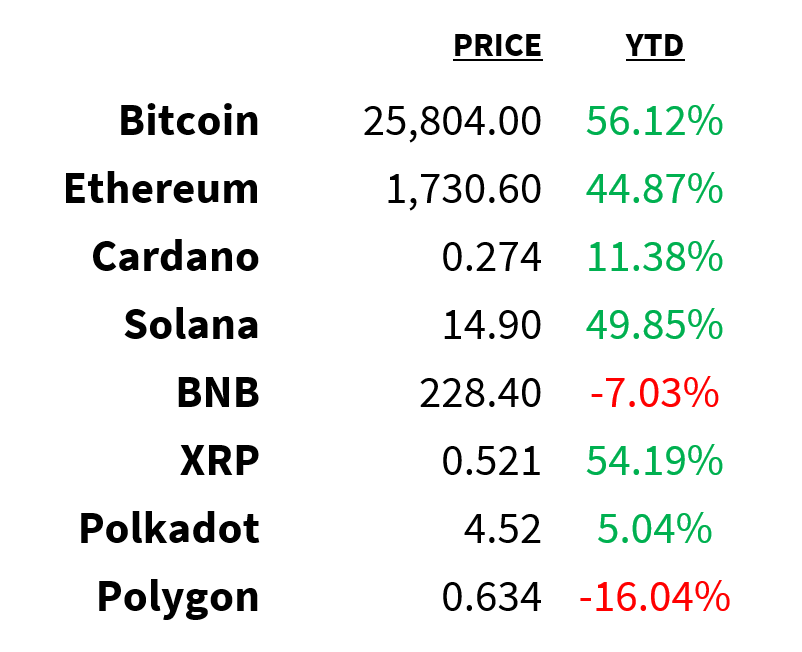

Crypto

Prices as of 4 pm EST, 6/12/23

-

Dwindling: Binance.US’ market share has plummeted to 5% from 20% in April.

-

Delisting: Investing platform eToro will delist 4 major cryptocurrencies for US users next month in response to recent SEC actions against Coinbase and Binance.

-

Client distributions: BlockFi is planning to enable customer withdrawals this summer.

-

Volumes: Crypto trading volumes on Robinhood were down 43% MoM and 68% YoY in May.

-

Tokenized T-bills: Finblox is partnering with OpenEden to bring tokenized US Treasury bills to emerging markets in Southeast Asia.

Deals

-

Biotech: Novartis has agreed to acquire US biotech firm Chinook Therapeutics for up to $3.5 billion.

-

MSFT x ATVI: The FTC will seek to block Microsoft’s $68.7 billion acquisition of Activision Blizzard.

-

O&G M&A: NextTier Oilfield Solutions and Patterson-UTI Energy are in talks for a potential merger.

-

Anchor investor: SoftBank is in talks with Intel and others to anchor its upcoming $10 billion Arm IPO.

-

Agriculture: Bunge and Viterra closed their $18 billion merger, creating one of the world’s biggest agriculture trading firms.

Meme Of The Day

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.