(Wednesday Market Open) Investors seem ready to pause buying to start a new month, quarter, and last half of the year after two days of solid gains helped make for the best quarter in more than 20 years.

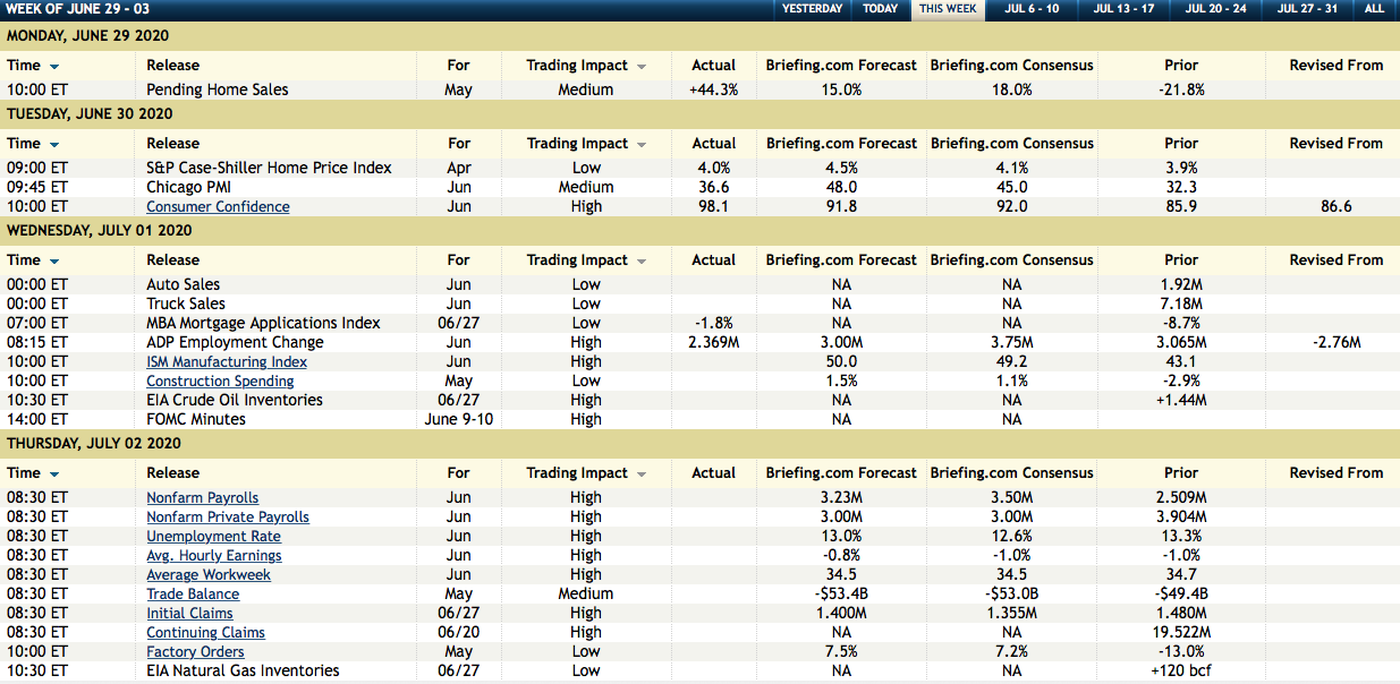

In economic news, an employment report from ADP and Moody’s Analytics showed fewer job additions than had been expected as its private payrolls figure rose by 2.369 million in June, missing a Briefing.com consensus forecast of 3.75 million. At the same time, the report showed a massive revision to the prior month’s figure, saying that 3.065 million jobs had been added in May when the original print had shown a loss of 2.76 million.

Considering last month’s payrolls report, which turned in solid gains against an expected loss, today’s ADP data is a reminder that, in the COVID economy, the collection of robust employment data has been a challenge. Keep that in mind for tomorrow’s jobs report, and remember that one data point is not a trend.

Although Wall Street’s main fear gauge was up a little and gold has hit a new multi-year high, this morning’s dip in stocks might not be too much to worry about considering that we’ve had two solid up days in a row. The jitters may be coming from worry as U.S. coronavirus cases continue to climb. Against a backdrop of lowered demand, the U.S. benchmark oil contract continues to struggle around the $40 mark. It may be worth watching whether the S&P 500 Index (SPX) can hold Monday’s close of 3054—a level seen as support on the downside.

In corporate news, shares of FedEx Corporation FDX were up about 11% in pre-market trading after the shipping giant opened its books following the closing bell yesterday. FDX handily beat earnings expectations, saying it earned more than a dollar above what analysts had been forecasting. Its revenues also beat expectations.

Analyst expectations were set on the low side. FDX’s revenue and net income were both below what they were a year ago, and operating costs were higher because of the coronavirus, the company said. But home deliveries have surged amid a spike in e-commerce deliveries in the United States. Plus, the business-to-business volume is coming back, according to the company. United Parcel Service, Inc UPS shares are also up this morning—4.5% since yesterday’s close—in an apparent sympathy rally. UPS is set to report its earnings in a few weeks.

Wednesday in Review

There was a lot for investors and traders to unpack on the last day of trading for the month, quarter, and half-year—with a mix of encouraging and sobering news on the table.

In closely watched congressional testimony, Fed Chairman Jerome Powell and Treasury Secretary Steven Mnuchin discussed the Fed’s and Treasury’s economic response to the pandemic in front of the House Financial Services Committee.

While Powell said that the economic recovery is “extraordinarily uncertain” and that the second wave of coronavirus cases could hit consumer confidence, he also said the recent bounce in economic activity is welcome. For his part, Mnuchin said the Treasury and Fed could add asset-based lending markets to the central bank’s already established emergency lending facilities.

Economic data for the day was mixed. June's consumer confidence rose more than expected. But data on manufacturing activity in the Chicago area was worse than forecast, and a home price index also came in below expectations, although both measures did show improvement over the prior month.

News from the semiconductor sector was pretty good, with Micron Technology, Inc MU, and Xilinx, Inc XLNX offering encouraging guidance. In quarterly results, MU beat expectations on its top and bottom lines. In general, we are seeing an uptrend in the chip makers, which could be because of expansion in 5G, electric vehicles, cloud storage, data centers, and artificial intelligence.

Meanwhile, Dr. Anthony Fauci said the U.S. could face 100,000 new cases a day unless people improve social distancing and mask compliance and states do better in heeding reopening guidelines. When you look at how far and fast the market has recovered from the initial virus-related economic scare, it’s tempting to think the corner has been turned. But it seems unlikely that the market can resume that upward trajectory if lockdowns return in force.

A Banner Quarter

With all that in the mix, the SPX rose more than 1.5%. It’s possible that some of the gains came from participants adjusting their positions to close out the month, quarter, and half year.

It may be a bullish sign that they wanted to add risk when adjusting their positions instead of reducing risk. That perhaps shows sentiment among investors and traders is still tilted toward optimism about economic recovery.

Despite modest gains for the month of June, the SPX still managed its best quarter in more than two decades on a percentage basis amid optimism about the economic reopening, massive fiscal and monetary stimulus, and hopes for a vaccine.

But it remains a big question as to whether that momentum can continue through the third quarter given the coronavirus resurgence in many states. Indeed, the stock market has already seen a pullback in its recovery as cases have rebounded in many states.

On the other hand, if a vaccine or treatment emerges, or if following social distancing, mask, and reopening protocols meaningfully halt the increase in cases, the stimulus could help send the market sharply higher. At this point, though, that seems like a big “if.”

CHART OF THE DAY: CHIPS SHOWING SOME MOMENTUM. After reaching a high in early June, the PHLX Semiconductor Sector Index (SOX—candlestick) has been trading in a range close to its all-time high (yellow line). It’ll be interesting to see if the index can break out above the high or if the level remains a point of resistance. Data source: Nasdaq. Chart source: The thinkorswim® platform from TD Ameritrade. For illustrative purposes only. Past performance does not guarantee future results.

Consumer Confidence Rises: It was encouraging to see an uptick in consumer confidence levels in June. After all, consumer spending makes up the single largest contributor to gross domestic product, accounting for around 70 percent of that important economic measure. The Conference Board’s Consumer Confidence Index increased to 98.1—beating a Briefing.com consensus expectation of a 92 print—from a downwardly revised 85.9 the previous month. But it seems that we’re hardly out of the woods. “Consumer confidence partially rebounded in June but remains well below pre-pandemic levels,” Lynn Franco, senior director of economic indicators at The Conference Board, said in a press release accompanying the numbers. “Faced with an uncertain and uneven path to recovery, and a potential COVID-19 resurgence, it’s too soon to say that consumers have turned the corner and are ready to begin spending at pre-pandemic levels.”

Stay-At-Home Trade Alive And Well: As the economic reopening takes some steps back in certain parts of the country, it appears that investors are still interested in getting exposure to companies that can benefit if businesses remain closed, or under capacity, and people spend more time at home than previously hoped for. Lululemon Athletica’s LULU shares rose 6% Tuesday after the athletic apparel maker said it plans to buy a home fitness company for $500 million. It’s interesting that the acquirer’s shares went up on the news. Often, when an acquisition is announced the buyer’s share price decreases initially. But in this case, it looks like investors are cheering the move at a time when many people might still want to work out at home instead of going to the gym. In the same vein, Uber Technologies, Inc UBER—already one of those companies that make staying at home easier with its Uber Eats food delivery unit—is reportedly talking to Postmates about buying the food delivery service for $2.6 billion. All of that is on top of Micron’s encouraging outlook, as its chips have been in demand as stay-at-home employees and students use the internet to work and learn.

Looking for Clues on Yield Curve Control: Later today, the Fed is scheduled to release the minutes from the latest meeting of its monetary policymaking body. It could be interesting to see if the minutes reveal more detail on the Fed’s thinking about yield curve control as a tool to try to stimulate the economy. The measure would involve the Fed buying certain maturities to cap those interest rates at set targets. According to a Bloomberg article, more than half of economists surveyed by the news agency in June expect yield curve control, and a record low in five-year notes and surging open interest in five and 10-year futures point to expectations that the Fed will embark on the measure.

This week’s economic calendar. Source: Briefing.com

TD Ameritrade® commentary for educational purposes only. Member SIPC.

Photo by Getty Images.

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.