The Past Week, In A Nutshell

What Happened: Last week ended negative on relative weakness in the technology sector.

Remember This: “While valuations have hinted to overstretched markets in the past, it’s tough to say where stocks should be trading right now. We just witnessed the fastest bear market and one of the fastest recoveries on record. The Federal Reserve is more engaged in the markets than it has ever been, which has distorted reality with record-low Treasury yields.” said Callie Cox, senior investment strategist for Ally Financial Inc-owned ALLY Ally Invest.

“One thing is for sure: when investors’ expectations for the future rise, stocks tend to rise as well. High expectations can leave a lot of room for disappointment, and investors’ fortunes can turn quickly when markets stray too far from the economy and earnings. That’s still a major risk here, but valuations alone aren’t enough reason to expect another historic slide.”

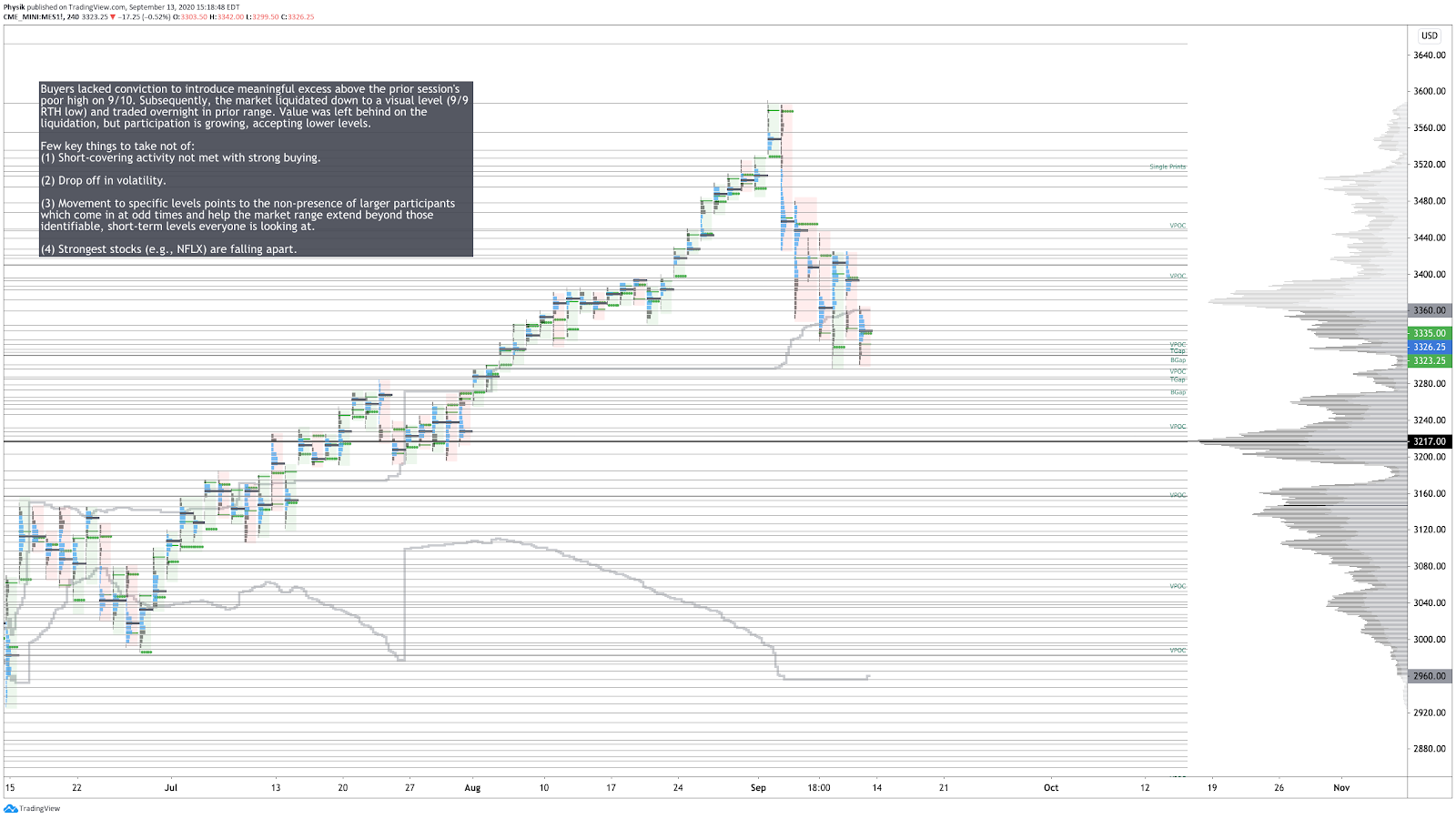

Pictured: Profile chart of the Micro E-mini S&P 500 Futures

Technical: Broad-market equity indices ended the week lower with the S&P 500 correcting to 3,300.

Recapping Last Week’s Action: On Tuesday, alongside Brexit news, on a second attempt, the S&P 500 broke through the 3,400 low-volume area, suggesting directional conviction changed. After spending much of the day trading neutral, the S&P extended lower, in-line with delta and away from value.

On news of AstraZeneca plc's AZN suspended COVID-19 trial, selling continued overnight into a base of liquidity in the 3,290 region before buyers regained control and one-time framed the market higher, to and through prior value and the low-volume area broken the day prior.

On Thursday’s economic data, the S&P 500 liquidated after non-convicted buyers failed to take out the prior day's low-excess high. Selling intensified as the market ate into prior low-volume, before closing off on a weak low, in-line with the prior day's cash-session low. After tech shares led an overnight rally up to some low-volume areas from the prior day's session, machine-like selling appeared and pushed the market through the weak low’s, before buyer's regained strength to finish Friday off in-range.

Overall, the recent mechanical activity to and from key technical levels denotes the non-presence of larger other time frame (OTF) participants and conviction. Heavily weighted index constituents are breaking trend while the broad market’s failure to extend much lower into the poor structure below it, coupled with reduced volatility pressures, suggests immediate downside may be limited. As a result, it’s time to temper expectations and look to reposition in line with emerging macro-economic and geopolitical themes.

Scroll to the bottom for non-profile charts.

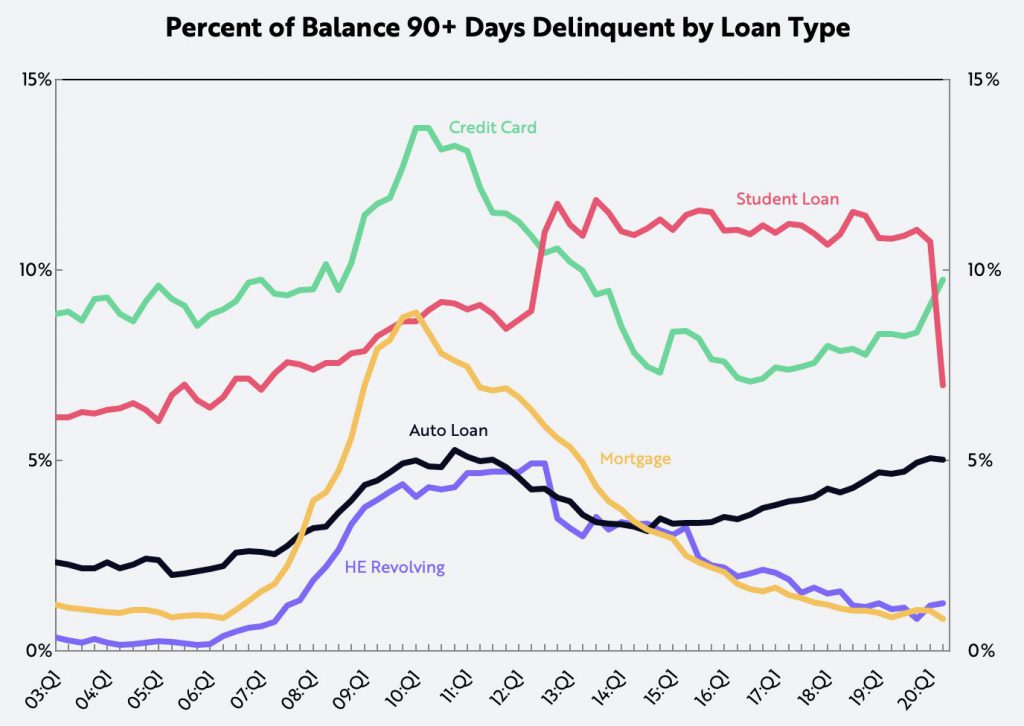

Fundamental: ARK Invest analyst Sam Korus suggested that the risks to auto loans, the securities supporting them, and underlying collateral may threaten the entire auto ecosystem.

“The percent of auto loans delinquent by 90 days or more has been rising for almost four years and is approaching levels last seen during the Global Financial Crisis (GFC) in 2009, as shown below. During the GFC, most consumers and businesses prioritized the servicing of auto loans over their mortgages because, in the absence of ride-hailing, they relied on vehicles to keep their jobs and businesses going. Now working from home, they seem to be prioritizing mortgages and home equity (HE) loans over auto and credit card debt.”

Korus also noted delinquencies may double while the underlying collateral will likely see a depression in residual value due to the mobility revolution. As a result, consumers, lenders, dealerships, and auto manufacturers may suffer financial damage as secular risks rebound in the tail-end of the COVID-19 recovery.

Source: ARK Investment Management

Key Events:

- Tuesday: Industrial Production.

- Wednesday: MBA Mortgage Applications; Retail Sales; Business Inventories; NAHB Housing Market Index; EIA Stocks Change; FOMC Economic Projections; Fed Interest Rate Decision; Fed Press Conference; Foreign Bond Investment; Overall Net Capital Flows.

- Thursday: Building Permits; Jobless Claims; Housing Starts; Philadelphia Fed Manufacturing Index.

- Friday: Michigan Consumer Sentiment; CB Leading Index; Michigan Inflation Expectations.

Recent News: White House eyes executive actions as virus-relief talks appear finished.

- Weekly jobless claims flatten as the labor market shows signs of fatigue.

- Bank of Canada head says too soon for exit from stimulus, will adjust QE.

- Forecasters see a 69% chance of an accessible vaccine by March 2021.

- New York office glut signals market downturn amid coronavirus recovery.

- Used cars drive U.S. consumer prices higher; inflation pressures firming.

- NYSE indicates that it will exit New Jersey if the state taxes stock trades.

- Equity market turmoil seen unlikely to provoke Federal Reserve response.

- U.S. proposes to waive minimum flight requirements for airlines until 2021.

- Tesla Inc TSLA launches fast electric car charging in Berlin.

- Pandemic e-commerce surge spurs race for Tesla-like electric delivery vans.

- Return of rush hour traffic in Europe and Asia adds to mixed outlook for oil.

- West Coast freight networks ‘bursting at the seams’ with surging imports.

- Equity funds have seen net outflows every week for every month of 2020.

- Purchasing managers’ indexes from ISM and IHS Markit show recovery.

- Production problems spur FAA review of Boeing Co BA 787.

- Copper on the cusp of a historic supply squeeze as China ups demand.

- New set of digitally influenced norms and behaviors born among consumers.

- Second wave of COVID-19 confronts Western Europe, following a sharp fall.

- Small businesses exhausted federal funding and started to lay off workers.

- Equity market volatility stemmed from risk of new, different tax frameworks.

- August jobs stronger than anticipated but did not meaningfully change outlook.

- European recovery is losing momentum as demand is soft, uncertainty remains.

- Japan’s economy to mark sharp contraction as a second wave materializes.

- Downtrend in credit quality slowed with upgrades outnumbering downgrades.

- Simon Property, Brookfield Property to buy JCPenney Company Inc JCPNQ.

- Economic model reform hopes rise as China focuses on inward economic shifts.

- Rise in remote, distributed workforces may drive new wave of venture deals.

- World Agricultural Supply and Demand Estimates as of September 11, 2020.

- The global energy transition is well under way and is accelerating rapidly.

- Walmart Inc WMT to test drone delivery of grocery household items.

- U.S. airlines warn on travel recovery while awaiting fresh recovery aid.

- U.S. utilities say Biden plan to cut C02 hinges on breakthroughs in clean tech.

Key Metrics

- Sentiment: 23.7% Bullish, 27.8% Neutral, 48.5% Bearish as of 9/9/2020.

- Gamma Exposure: (Trending Lower) 1,970,983,599 as of 9/11/2020.

- Dark Pool Index: (Trending Lower) 42.1% as of 9/11/2020.

Product Snapshot

S&P 500 E-mini Futures (ES) | SPDR S&P 500 ETF Trust SPY

Nasdaq-100 E-mini Futures (NQ) | PowerShares QQQ Trust QQQ

Russell 2000 E-mini Futures (RTY) | iShares Russell 2000 Index IWM

Gold Futures (GC) | SPDR Gold Trust GLD

Crude Oil (CL) | United States Oil Fund LP USO | Invesco DB Oil Fund DBO | United States 12 Month Oil Fund USL

Treasury Bonds (ZB) | iShares 20+ Year Treasury Bond TLT

Photo by Karolina Grabowska from Pexels.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.