The Past Week, In A Nutshell

What Happened: Last week ended negative on weakness concentrated in heavily-weighted index constituents.

Remember This: “The Fed essentially acknowledged they were a bit behind the curve with their forecast on the economy, as projections needed tweaking to reflect the current path of the recovery,” noted Charlie Ripley, Senior Investment Strategist for Allianz Investment Management.

“However, with near-term risks to the outlook still intact, the Fed continues to reiterate that it is too early for victory laps on the economic recovery. On the horizon, the path of the virus, the upcoming election, and the motivation for additional fiscal stimulus are all hurdles the economy needs to overcome.”

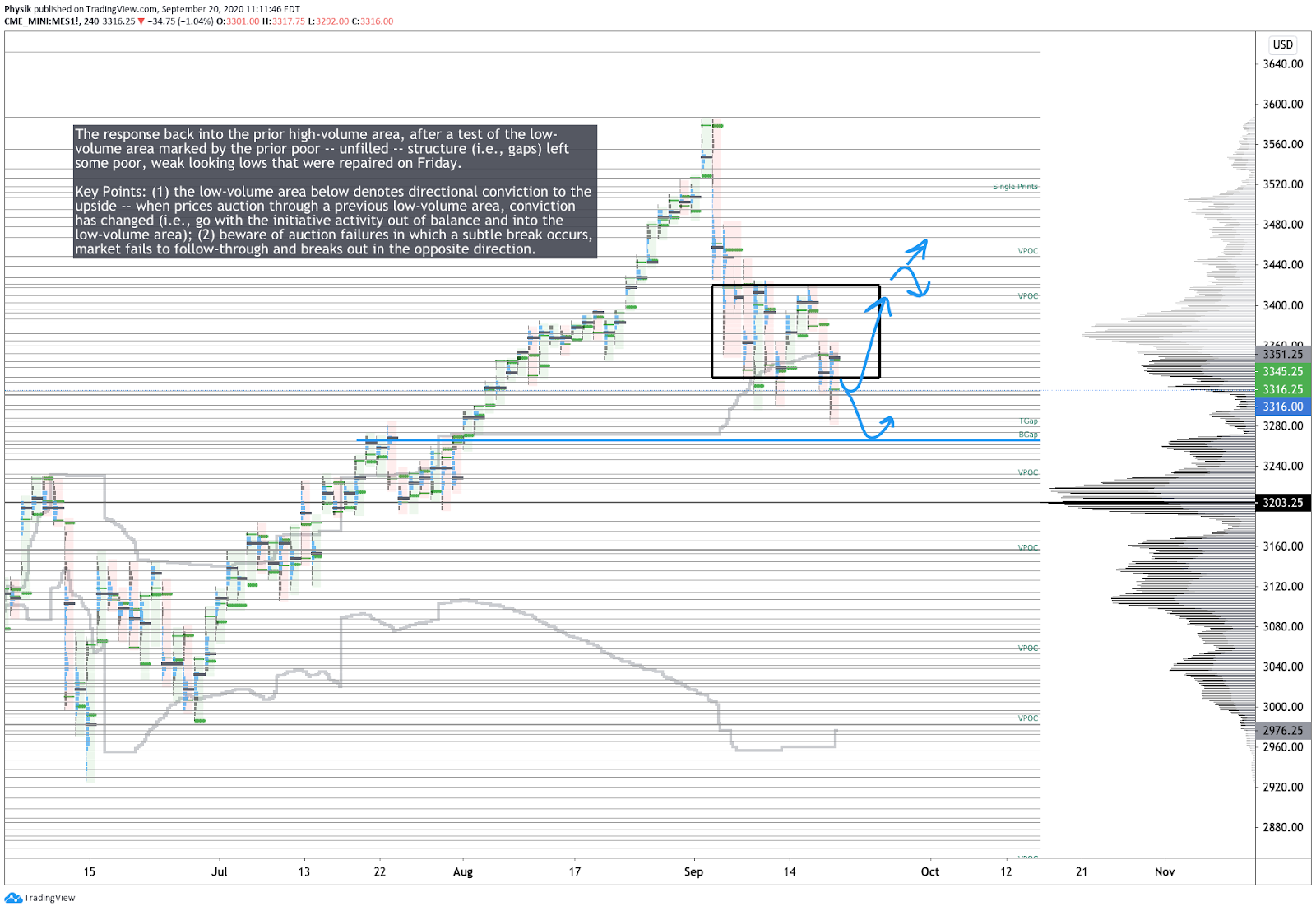

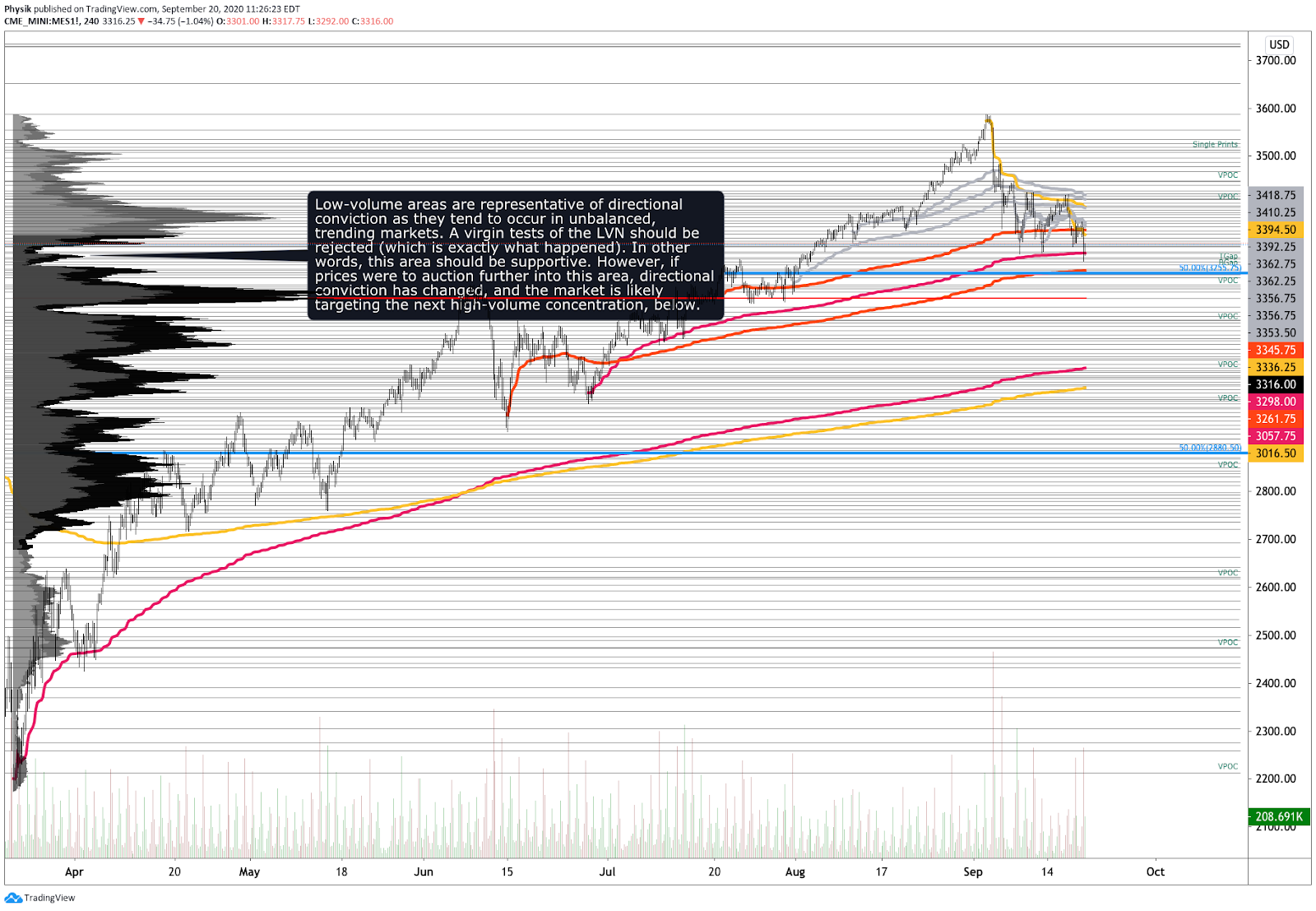

Pictured: Profile chart of the Micro E-mini S&P 500 Futures

Technical

Broad-market equity indices ended the week lower with the S&P 500 correcting to $3,280.

Recapping Last Week’s Action: Alongside progress in COVID-19 vaccine development, on Monday, participants rejected the prior week's low, establishing value higher on a gap. Ahead of the Federal Reserve's two-day meeting, Tuesday’s session confirmed the upside directional conviction, trading up to a multi-day ledge formed by mechanical sellers. In light of Fed statements, after the ledge proved resistive for two days straight, the market liquidated through Friday’s session, testing and accepting value near a low-volume area that formerly denoted directional conviction to the upside.

Overall, the market’s weakness on economic concerns and acceptance of value below a composite high-volume area, confirms the near-term change in conviction. That said, indices keep testing the low-volume area below $3,320. Acceptance within the low-volume area may foreshadow a test of $3,270, the next-closest high-volume concentration which could slow prices enough to allow responsive longs entry at more favorable prices.

Scroll to bottom of document for non-profile charts.

Fundamental

Albert Edwards, chief investment strategist at Societe Generale SA SCGLY, suggested rapid money supply growth will worsen the deflationary bust.

“Why? The flipside to looking at money supply growth is to look at its counter-parties on the asset side of the banks’ balance sheets. It is clear that the main driver for the recent explosive 25% monetary growth has been bank lending to industrial and commercial companies, which despite only comprising a quarter of total bank lending has contributed some 70% of the total rise in lending over the past year, surging 30% yoy. One thing we now know for sure after Japan’s lost decade: keeping zombie companies alive with “extend and pretend” bank loans creates deflation, not higher inflation.”

Simply put, indebtedness and malinvestment in unproductive activities will lower the economy's growth prospects.

Key Events

- Monday: Chicago Fed National Activity Index, Fed Brainard Speech, Fed Kaplan Speech, Fed Williams Speech.

- Tuesday: Existing Home Sales, Fed Evans Speech, Fed Chair Powell Testimony.

- Wednesday: MBA Mortgage Applications, Fed Mester Speech, House Price Index, Markit Manufacturing PMI Flash, Fed Chair Powell Testimony, EIA Cushing Crude Oil Stocks Change, EIA Distillate Stocks Change, Fed Evans Speech, Fed Quarles Speech.

- Thursday: Initial Jobless Claims, Continuing Jobless Claims, Jobless Claims 4-Week Average, Fed Chair Powell Testimony, New Home Sales, Treasury Secretary Mnuchin Testimony, Fed Evans Speech, Fed Williams Speech.

- Friday: Durable Goods Orders, Fed Williams Speech.

Recent News

- Broad macro backdrop improves; pro-risk and credit are preferred.

- Markets, bankers, and analysts are differing on 2021s default rate.

- Philip Morris International Inc. PM cuts into its leverage.

- Analyzing COVID vaccine pipeline and immunization scenarios.

- Labor market recovery stalls as housing market presses ahead.

- Promise to revive coal thwarted by falling demand, alternatives.

- Gilead Sciences Inc. GILD Immunomedics deal risky.

- Apple Inc. AAPL rolls out virtual fitness service.

- Alphabet Inc. GOOGL faces grilling on ad business.

- Fed will keep rates zero until inflation is on track to exceed target.

- General Motors Co. GM to manufacture EV drive systems.

- Hurricane cuts into quarter of U.S. Gulf of Mexico energy output.

- Fading fiscal stimulus is restraining U.S. consumer spending.

- Nasdaq Inc. NDAQ is launching AI-driven AML tech.

- Morgan Stanley MS believes the trading boom won’t continue.

- Trump announces nearly $13 billion in farm aid at Wisconsin rally.

- Saudi energy minister gives warning to oil market short sellers.

- Moderna Inc. MRNA to produce 20 million vaccines.

- Economics and the damage of Financial Transaction Taxes (FTT).

- Kashkari urges big investors to demand banks hold more capital.

- Trump blesses Oracle Corp.’s ORCL TikTok deal.

- Boeing Co. BA 737 MAX returns and backlog risks remain.

- Trump to emphasize energy infrastructure buildout in the second term.

- Nikola Corp. NKLA examined by SEC regarding Fraud.

- UBS Group UBS, Credit Suisse Group CS to merge.

- Sentiment weakens as outlook for the oil market looks more fragile.

Key Metrics

- Sentiment: 32.0% Bullish, 27.6% Neutral, 40.4% Bearish as of 9/16/2020.

- Gamma Exposure: (Trending Lower) 189,695,161 as of 9/18/2020.

- Dark Pool Index: (Trending Higher) 44.2% as of 9/18/2020.

Product Snapshot

S&P 500 E-mini Futures (ES) | SPDR S&P 500 ETF Trust SPY

Photo by Pixabay from Pexels.

Edge Rankings

Price Trend

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.